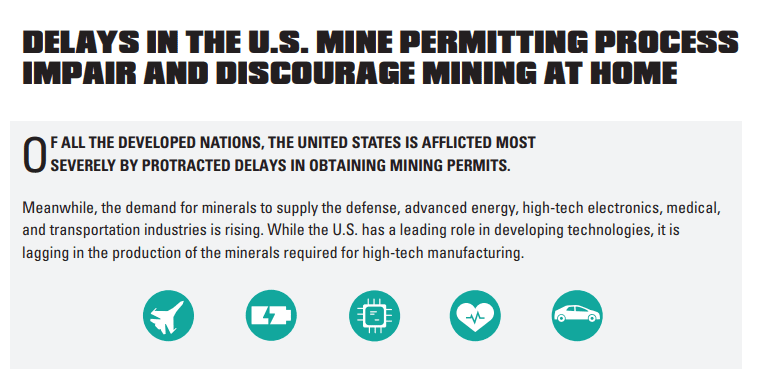

What is the current landscape of the mining industry in the US?

America’s got the rocks, but it comes with a lot of red tape.

The US mining sector is a study in contradictions – it’s one of the largest global producers of mined materials, such as copper, gold, and coal but it’s slow and continually strangled by permitting delays.

Put simply, America can dig. It just can’t get permission to start digging.

Cortez gold mine in Nevada

Most industry activity still centres on the usual suspects – copper, gold, and coal. But there’s been a real shift towards critical minerals in recent years. Lithium, rare earths, graphite, nickel, and cobalt. Not because the rocks are new, but because the urgency is. Clean energy policies and growing tension with China have quickly changed the tone.

So the problem isn’t geology. It’s paperwork. There’s a bureaucratic maze standing between a deposit and actual production in the US. Policy makers want secure mineral supply, but the internal production pipeline is far from quick.

As Mick Malthouse once said – the ox is slow, but the earth is patient.

Nevada dominates gold production and exploration activity. Arizona and Utah still shoulder most of the copper load, while Alaska offers a mixed bag of base and precious metals.

But interest is now creeping east into Arkansas, Idaho, and the Carolinas (North and South), where new rare earths and lithium clay targets are starting to gain traction.

Bingham copper mine in Utah

The US has more than 400 active mines and 700 junior exploration projects. In 2024 the exploration spend in the US was approximately US$1.65 billion. Only Australia and Canada spent more.

All the mining majors are in the US – Freeport, Rio Tinto, BHP, Ivanhoe, Barrick, Glencore and many others, showing the country can attract both junior explorers and virtually every tier-one miner globally.

America’s made its intentions clear. Reduce dependence on China and Russia by developing domestic mines.

It’s the approvals and timelines that are keeping things stuck in second gear.

What are the US’ key sectors?

The stalwarts of American mining (copper, gold, coal, sand, gravel) haven’t changed much. These still account for the bulk of the country’s production value, with majors like Freeport-McMoRan and Newmont running the show.

But the real shift is happening in minerals tied to the energy transition and defence.

Lithium and rare earths are now being prioritised at the federal level under the Defence Production Act. The US has watched Australia ship raw materials offshore for decades, only to buy back the processed products at a premium. They’re determined not to repeat that mistake.

Instead, the US wants the whole value chain on home soil. Mining, processing, refining, end use. All of it.

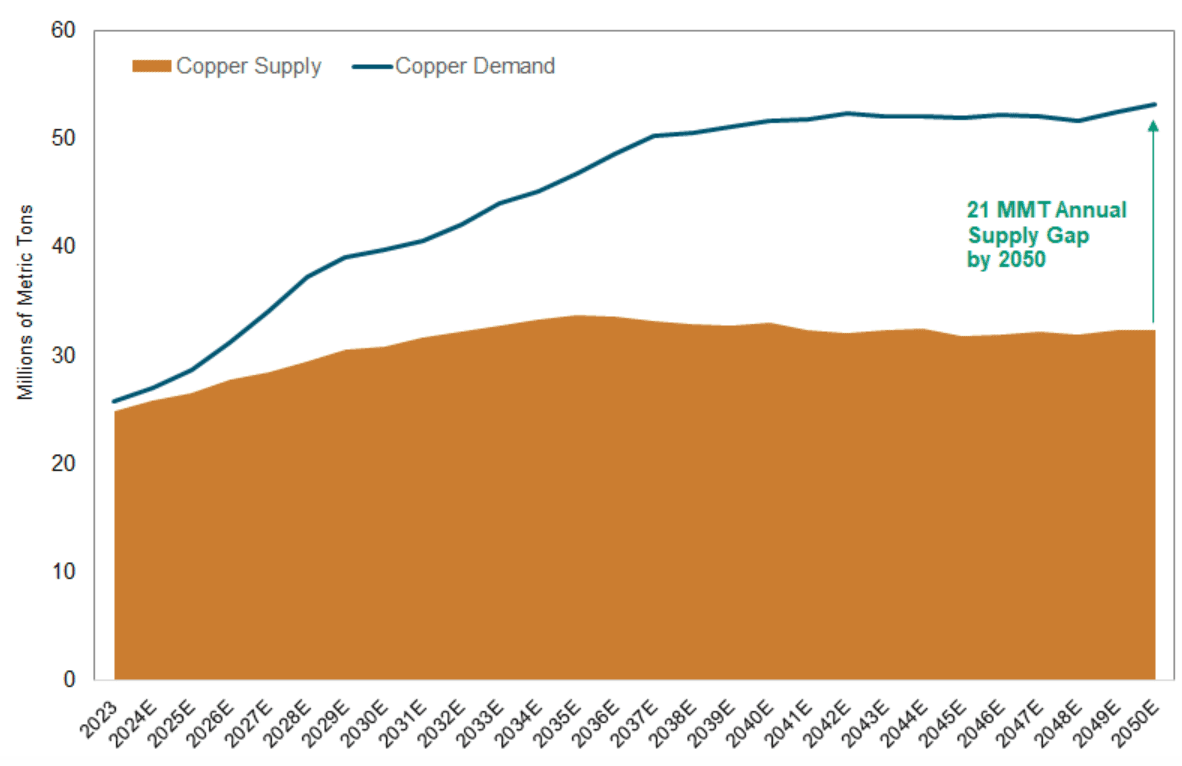

Copper

But turning talk into action isn’t always straightforward. Case in point: the Resolution project in Arizona.

Owned by BHP and Rio Tinto, it’s one of the world’s largest undeveloped copper deposits – enough to supply a quarter of US demand for decades. Yet despite its scale and backing, it remains stuck in permitting limbo.

Resolution copper project

Resolution copper project

The US recognises this and realises that copper is needed for the electrification of the global economy. Used in electric vehicles, power lines, and all kinds of infrastructure, copper sits at the top of the list of commodities the USA would like to mine and process (and the top of a couple of our ASX watch lists too).

Coal

Coal presents a split story. Thermal coal’s long-term trajectory is downward, but regions like Appalachia and the Powder River Basin were built around coal mining and continue producing today. Metallurgical coal sits in a different category – it’s essential for steelmaking and remains crucial for defence and infrastructure.

Other Sectors

These are the key sectors. But in recent years, the US government has also directed funding into lithium projects and flagged support for rare earths, once again in an effort to diversify away from China.

Thacker pass lithium project in Nevada

Over half of the US$1.65 billion spent on exploration in the USA goes towards gold, with copper making up approximately US$450 million. It shows that companies see value in US-based assets and are willing to spend to find more.

Of that US$1.65 billion, over half is being spent on late-stage exploration projects heading into feasibility. The challenge emerges once projects reach feasibility. Early-stage exploration moves relatively smoothly, but the permitting process creates a bottleneck that can stall projects for years.

The US is resource-rich; it now needs to take steps to keep on improving the process and encourage investment.

What the US produces (and could produce more of):

- Precious metals: gold, silver, platinum group metals

- Base metals: copper, zinc, lead, molybdenum

- Battery minerals: lithium, nickel, cobalt, manganese, graphite

- Rare earth elements: neodymium, praseodymium, dysprosium, terbium

- Industrial minerals: phosphate, potash, barite, fluorspar, silica

- Energy minerals: thermal and metallurgical coal, uranium

What could a mining policy look like under Trump?

Six months into his second term, Trump’s mining agenda is becoming clearer. The administration is prioritising mining, not just as an economic tool but as a pillar of national security. Trump’s “drill baby, drill” mantra isn’t just campaign rhetoric anymore – it’s policy.

The early signals suggest Trump’s intent is fast-tracking mine approvals and slashing regulatory red tape. The message is crystal clear: domestic production over imports, especially for anything China currently dominates.

The first time around, the Trump administration labelled certain materials as “critical minerals” and signed executive orders to encourage exploration. But on the ground, not much changed. The permitting web was too tangled to cut through.

This time, the federal approach looks more aggressive. There’s talk of simplifying overlapping state and federal approvals and using executive orders to accelerate key projects.

Support for battery materials, such as lithium and rare earths, has stayed strong — even with prices dipping. Uranium’s also back on the radar. The US is pushing nuclear again, both for energy independence and supply security. Trump has signed orders to ease approvals for new reactors and shore up fuel chains.

Expect funding for processing plants and incentives for companies building downstream capacity domestically.

Coal will re-enter the energy debate under Trump as well. While much of the West continues to phase it out, Trump’s keen to bring it back for energy and for jobs (and let’s be honest, for votes).

That includes thermal coal and, importantly, metallurgical coal, which aligns with infrastructure and defence manufacturing. These two areas have been clearly identified as requiring more attention.

The tone has shifted. It’s no longer “Can we mine this?“, it’s “Why aren’t we mining this already?“

Projects like BHP and Rio Tinto’s Resolution Copper project are suddenly front of queue. Large-scale, economically viable projects that enhance US security get priority treatment.

Trump’s team is pushing hard, but like all mining ventures, the real benefits to US supply security won’t materialise until well after he’s left office.

What does this mean for investors?

The US policy shift under Trump could be a significant catalyst for small-cap mining investors.

It’s been decades since any administration managed to meaningfully reform mining regulations. With streamlined approvals and reduced bureaucracy on the horizon, small-cap opportunities could multiply quickly.

Permitting and funding are joined at the hip in mining – you can’t get the second without the first. And this opportunity isn’t limited to American companies.

Several ASX-listed juniors hold projects in the US or partner with North American players, and a friendlier regulatory landscape could shift sentiment sharply in their favour.

While permitting complexities increase globally, streamlined US approvals could trigger a capital rush into American projects.

Government co-investment is already happening. The Department of Energy has already backed projects like the Thacker Pass lithium project that align with strategic objectives. Expect more of this in the coming years.

Geopolitics adds another layer. Trump’s well-documented scepticism toward China means any trade tensions could place a premium on domestic supply chains. US-based projects suddenly become strategic assets as well as commercial ventures.

If Trump stays the course, we could see reratings of US-focused explorers before any policy even hits paper.

For investors, it’s about reading the room early and doing the homework now. When the narrative shifts, you want to already have your shortlist of quality projects ready to go.

Which ASX small caps could benefit?

When it comes to juniors, the sweet spot is finding a company that fits the political moment, and knows how to tell that story.

Trump 2.0 is all about critical minerals, domestic processing, and energy security. That puts certain ASX explorers in a much stronger position.

Several ASX small-caps already have ground in the US. If permitting gets easier and Washington throws its weight behind the right projects, some ASX small-caps could potentially move fast.

Here are a few small-caps on our radar:

Hawk Resources (ASX: HWK) – copper explorer

Uvre Limited (ASX: UVA) – uranium

Patriot Resources (ASX: PAT) – copper

Advance Metals (ASX: AVM) – gold

Sierra Nevada Gold (ASX: SNX) – gold

The beauty is that these companies don’t just have US projects – they have US projects in commodities that Trump actually cares about.

How can Aussie investors get involved?

Getting exposure to the US mining story is easier than you might think. The ASX hosts several companies with projects across America.

Whether you like Trump or not shouldn’t matter. If there’s value the ASX market hasn’t priced in, the smart move is to be early.

The most direct path is through ASX companies with US assets. Historically, these stocks have traded at a discount (mostly thanks to the slow permitting we’ve been banging on about). But that could flip fast.

If the Trump administration follows through on faster approvals, those discounts turn into upside. That means sentiment-driven rerates and real project progress for investors already on the register.

ETFs and thematic funds are another option, they’re less direct, but easier for those who don’t want to pick individual stocks. They can give broader exposure to critical minerals or US resource plays without the volatility of a single junior.

More sophisticated investors can access private placements and early-stage capital raises. Many ASX juniors will tap markets for fresh capital to fast-track their US projects.

These rounds are high-risk plays though – there’s never a guarantee your investment will even make it to market.

The key is staying close to the signals. Policy can shift overnight. Trump might tweet about tariffs at breakfast and rerate a stock by lunch. The funding taps in Washington open and close just as fast.

Look at what happened with Dateline Resources (ASX: DTR), which saw a 1000% increase after Trump mentioned them as a potential Rare Earth mine.

Understanding where policy is heading, which commodities are at the centre of that story, and which companies can realistically benefit allows investors to trade with confidence.

The US might feel like the wild west sometimes, but right now, it’s also the land of opportunity for small-cap investors who are paying attention.

Opportunities

America’s been sitting on a geological treasure chest for decades, but the lock’s been jammed with bureaucratic red tape.

Trump’s second term could be the key that finally opens it. The real opportunity lies in backing projects that have been gathering dust in regulatory filing cabinets. Once permitting gets streamlined, today’s bureaucratic nightmares could become tomorrow’s production success stories.

Copper’s the obvious winner here. We’ve seen what happens when major copper projects get approval – valuations don’t just rise, they rocket. Companies holding US copper ground could be sitting pretty, especially if Washington starts throwing money at domestic processing facilities.

For investors with strong stomachs, early-stage placements in US-focused juniors can offer the chance for serious returns. Basically it’s betting on a regulatory transformation that could turn exploration lottery tickets into production realities faster than expected.

Risks

As always, the upside comes with a few sharp edges.

Trump might talk a big game about faster approvals and mining dominance, but turning that into reality isn’t guaranteed. We’ve seen promises before. They don’t always survive the political obstacle course that is the US.

Investors have been burned before by grand promises that fail to materialise once political battles start.

Federal support doesn’t mean everyone’s on board. Local communities still have voices, environmental groups still have lawyers, and state governments don’t always play nice with federal directives. Mining projects can still get tied up in court for years, regardless of what Washington wants.

Then there’s the small matter of commodity prices. Even if every US project gets fast-tracked approval, global market forces still call the shots on profitability.

For Aussie investors holding US-facing stocks on the ASX, the Aussie dollar is also a factor. If AUD runs, it can eat into your returns. You won’t notice it day-to-day, but over 12 to 18 months it adds up. Especially if you’re in something illiquid.

And Trump is a mixed bag as we know. One minute he’s pushing for nuclear funding, the next he’s threatening tariffs on half the periodic table. It can be hard to price that in.

That said, all investing is risk. It’s just about knowing which ones you’re comfortable wearing.

In summary

America’s mining sector has been napping for decades, but Trump’s second term might just be the alarm clock it needed.

If Trump delivers even half his promises, early positioning could pay handsomely. The time for talk is done. Or as Benjamin Franklin once put it, well done is better than well said.

For Aussie investors, ASX juniors with US projects offer a unique opportunity to ride this wave from the comfort of home.

As always, homework beats hope. Know which companies hold US ground, which management teams have navigated American bureaucracy before, and where the political winds are blowing. That knowledge edge makes all the difference.

The ASX small-cap space never lacks drama, but US-focused mining plays could steal the show over the next few years.

If Donald Trump can cut through the red tape as promised, there’s real money to be made.