With everything going on in the Gulf, good stock stories are getting lost in the noise right now.

One that shouldn’t be is Fortuna Metals (ASX: FUN).

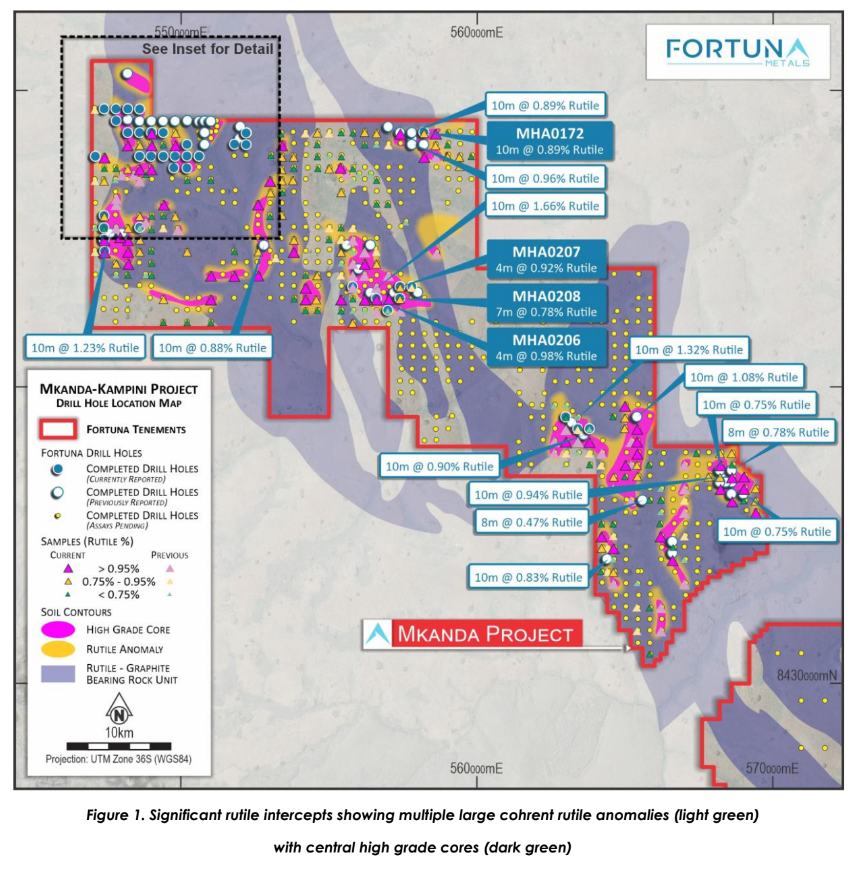

FUN put out another batch of drill results this morning from its Mkanda rutile project in Malawi, and they’re good. High-grade rutile across 40 holes, mineralisation starting at surface, and most holes still going when the drill stopped.

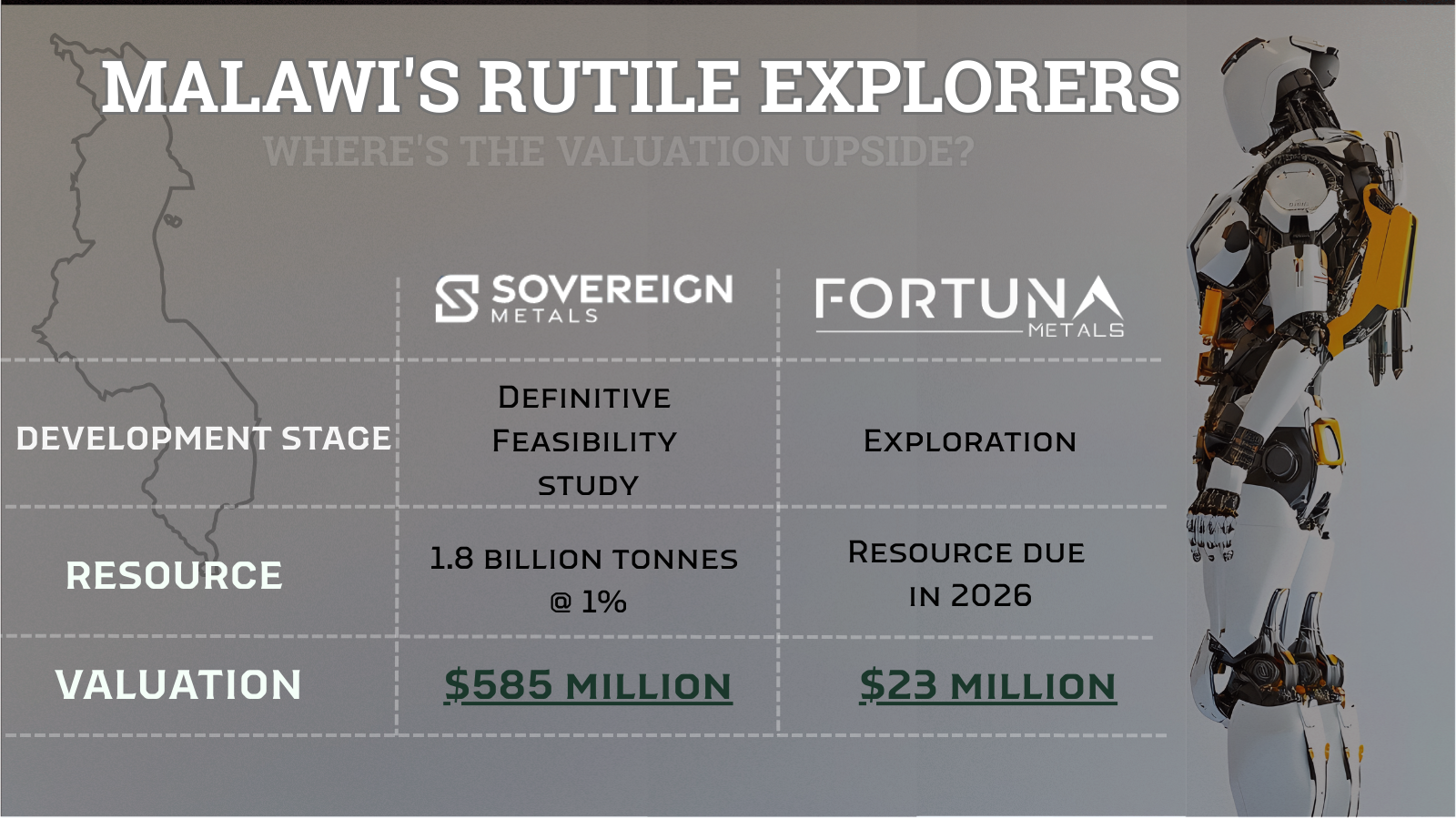

For anyone new to the story: FUN’s ground sits immediately south of Sovereign Metals’ (ASX: SVM) Kasiya deposit, the largest rutile deposit in the world and the second largest flake graphite deposit globally.

SVM is worth around A$585 million. FUN trades at roughly A$22 million with the same geological belt, and same style of mineralisation. And FUN’s early grades are comparing well.

FUN has already proved the same geological system extends onto its ground, now it’s about understanding how big it is. With such a valuation differential in play, we think FUN is one of the most overlooked stories on the ASX right now.

Since we last wrote about FUN in February, the Malawi export ban scare has been officially cleared by the government, and there’s now a third round of high-grade results on the table. The share price hasn’t caught up with either.

Why Rutile Demand Is About to Get Loud

We wrote about the humanoid robot thesis back in November and said it was moving quicker than most people expected. Four months on, we now see we undercooked it.

Last weekend, Xiaomi put two humanoid robots on its EV assembly line in Beijing. They ran autonomously for three hours, completing 90% of tasks on a 76-second production cycle. That’s the same pace as the human workers around them.

Two days later, BMW announced it’s deploying a second wave of humanoid robots at its Leipzig plant in Germany, after a pilot at its Spartanburg factory where the machines handled more than 90,000 components across 1,250 operating hours.

And Tesla has gone further than both. In January it announced it was shutting down Model S and Model X production at Fremont to convert the factory for Optimus robot manufacturing, with a target of up to 100,000 units by the end of 2026.

You can’t build a humanoid robot without titanium. The frames, joints and structural components all rely on titanium alloys because nothing else gives you the same strength at the weight. And you can’t make titanium without rutile. It’s the starting point for the entire supply chain, the cleanest, highest-grade feedstock there is.

Each humanoid robot is estimated to contain around 10.4 kilograms of rutile. You can probably see what we’re getting at here now.

Natural rutile is currently selling for roughly US$1,900-2,000 per tonne, and the titanium market is forecast to grow from US$30 billion in 2025 to US$54 billion by 2034.

Legacy rutile producers are in decline and new deposits of any real scale are rare, which means the supply picture is tightening from both ends.

When there’s projection of scaling from 16,000 robots to potentially millions by the end of the decade, the feedstock question stops being theoretical pretty quickly. And right now, there aren’t many companies on the ASX sitting on large-scale rutile deposits that could help answer it.

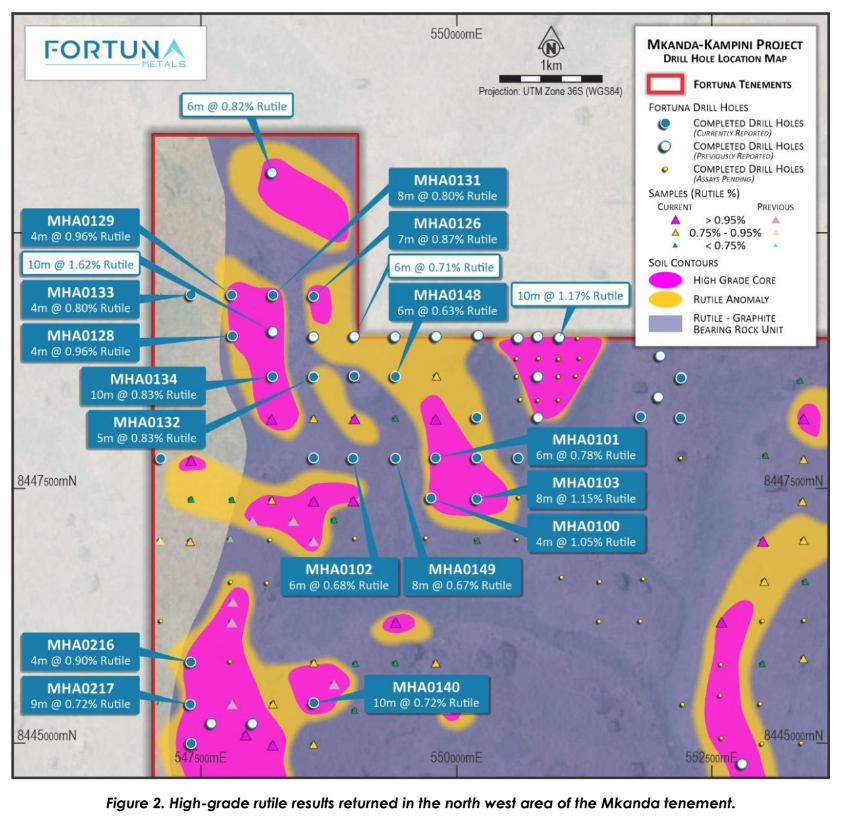

40 Holes of High-Grade Rutile at Mkanda

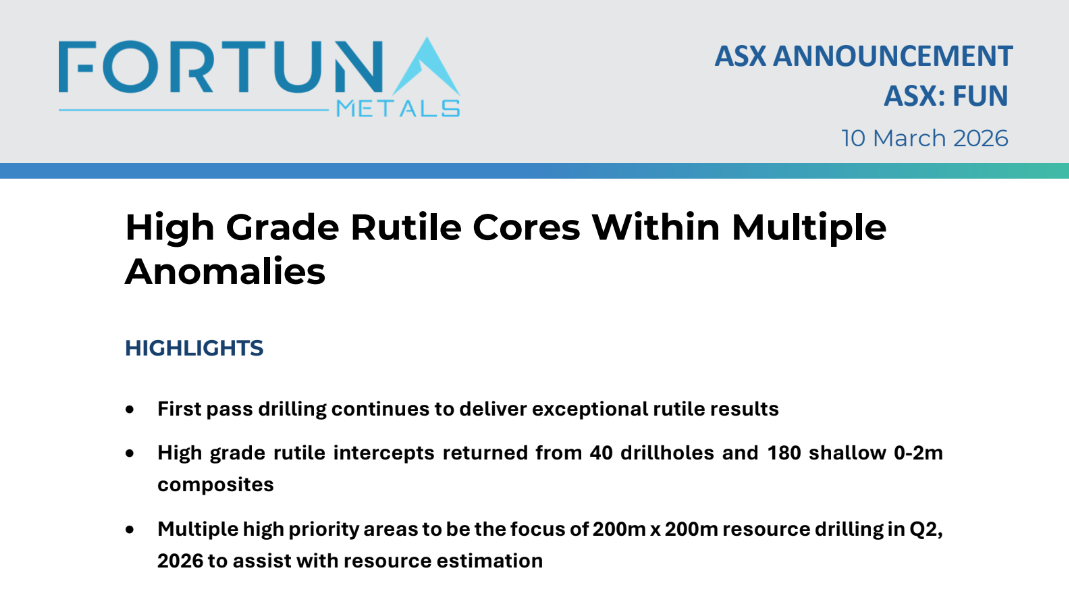

Today, Fortuna Metals reported results from 40 drill holes along with 180 shallow 0-2 metre composite samples, confirming rutile mineralisation across multiple zones at the Mkanda project.

Among the best intercepts reported were:

- 8m @ 1.15% rutile

- 10m @ 0.89% rutile

- 10m @ 0.83% rutile

- 10m @ 0.72% rutile

All of those holes (and plenty of others) ended in mineralisation, meaning the rutile continues beyond the end of drilling. The drill stopped before the rutile did.

The shallow 0-2 metre samples tell a similar story. Peak grades of 1.74%, 1.53%, and 1.40% rutile, with around 85% of samples above the cut-off grade.

The shallow sampling is Fortuna’s way of quickly mapping where mineralisation is thickest before committing to deeper drilling.

The high-grade core has now expanded to 17.8km², sitting within broader rutile anomalies covering roughly 37km² in total.

FUN has completed 675 holes across 180km² of the Mkanda tenement. There are still 485 full hole assays and more than 300 shallow samples to come through, so this story has months of news flow left in it before the company even starts the next drilling phase.

SVM, Rio Tinto, and the Valuation Gap

Rio Tinto just committed US$473 million to restart a titanium sands mine in South Africa because the deposit feeding its current operation is dying. That’s half a billion dollars just to keep existing rutile production alive.

Twenty kilometres north of Fortuna Metals sits Kasiya, the world’s largest rutile deposit, owned by Sovereign Metals (ASX: SVM). Rio is also SVM’s largest shareholder with a 19.9% stake.

Between the two, Rio has made it pretty clear where it thinks rutile supply is headed.

SVM is currently valued at around A$585 million and is progressing through its definitive feasibility study.

Fortuna Metals’ Mkanda project sits in the same Lilongwe Plain geological formation as Kasiya, the same weathered gneiss where tropical weathering has pushed rutile close to surface over millions of years.

The grade profile and geometry FUN is seeing in its early holes maps closely to what Kasiya looked like at the same stage of exploration.

Back in 2019, SVM was valued at around A$35 million and was just starting to show rutile continuity across its ground. Twelve months later it was A$160 million.

FUN, at A$22 million, is sitting below that starting line with three batches of drill results already in hand.

FUN is valued at roughly 5% of SVM. That gap reflects the difference in project maturity, and it tends to close fast when exploration starts converting into resources.

SVM’s ore reserve upgrades from 1.03% rutile to a 2.00% rutile equivalent once graphite credits are factored in, near-doubling of the headline grade. FUN’s graphite assays from Mkanda are due in Q2-Q3.

If the graphite numbers reflect the same geological setting, the project economics could look very different to what the rutile-only story suggests today.

SVM recently signed an offtake MOU with Traxys North America, a major global commodity trader, covering up to 80,000 tonnes per annum of Kasiya graphite.

FUN’s graphite assays could open up a similar conversation if the results come in strong.

Aircore Drilling, Graphite Assays, and a Maiden Resource

Fortuna Metals has only sampled the top eight metres at Mkanda. At Kasiya, the mineralised zone runs to 20-30 metres depth. Everything reported so far could be less than half the picture.

The hand auger rigs FUN has been using can’t push past the water table. Once the ground gets saturated, the samples turn to mush. At Mkanda, that’s been cutting holes off at around 8 metres.

Aircore drilling starts from May, and it can push through that saturated layer and keep going until it hits saprock, the hard, unweathered rock beneath the mineralised zone where rutile concentrates.

Ahead of that, resource drilling on a 200m x 200m grid is planned for Q2, aimed at supporting a maiden inferred resource estimate in the second half of 2026.

Metallurgical test work is underway targeting a rutile concentrate above 95% TiO₂, which is the quality level that attracts serious offtake interest from industrial buyers.

If FUN can get an offtake partner across the line, the story shifts from pure exploration to something with real commercial legs, and the market tends to reprice that transition quickly.

Our Take on Fortuna

We think FUN is one of the most mispriced small-caps on the ASX right now.

The company has 675 holes in the ground confirming a large, coherent rutile system in the same geological belt as the world’s biggest deposit. Hundreds more assays are still to come, and there’s a clear program through 2026 to convert what’s been found into a resource estimate.

The industrial demand case for rutile is playing out in real factories right now. At around A$20 million, you’re getting a lot of exploration progress for not much money.

The news flow runs through the rest of the year, the graphite results haven’t landed yet, and FUN is still trading at a fraction of the monster sitting 20 kilometres up the road.

The risk is that this is still early-stage exploration. Drilling can throw curveballs and resource estimates don’t always land where the early results suggest.

But the valuation gap to SVM, the assay pipeline, and the graphite results still to come give this stock more catalysts over the next twelve months than most small-caps we follow.

General advice warning, disclosure and confidentiality notice

General advice warning

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consulting your own investment advisor to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (“Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 1,554,000 FUN shares at the time of publishing this article. Equities Club has been engaged by FUN at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.