Fortuna Metals (ASX: FUN) is back with its second update of the week, and this one reframes the economics picture for the Mkanda project in Malawi.

Since acquiring Mkanda in September, FUN has been progressing work to define the rutile system across the project.

Rutile is the highest-grade feedstock for titanium, a metal expected to see strong demand growth as lightweight titanium alloys become increasingly important in humanoid robotics.

Today’s announcement adds heavy rare earths and graphite to the Mkanda story, and the project is reading more and more like the world-class Kasiya deposit immediately to the north.

Kasiya is owned by Sovereign Metals (ASX: SVM), which is valued at $460 million and has none other than Rio Tinto as shareholders. SVM released a study two weeks ago valuing the Kasiya asset at USD$2.2 billion before tax.

Rutile is still the main game at Mkanda. But these results add two more revenue streams alongside it, and the closer FUN’s chemistry tracks Kasiya’s, the harder that $430 million market cap gap gets to justify.

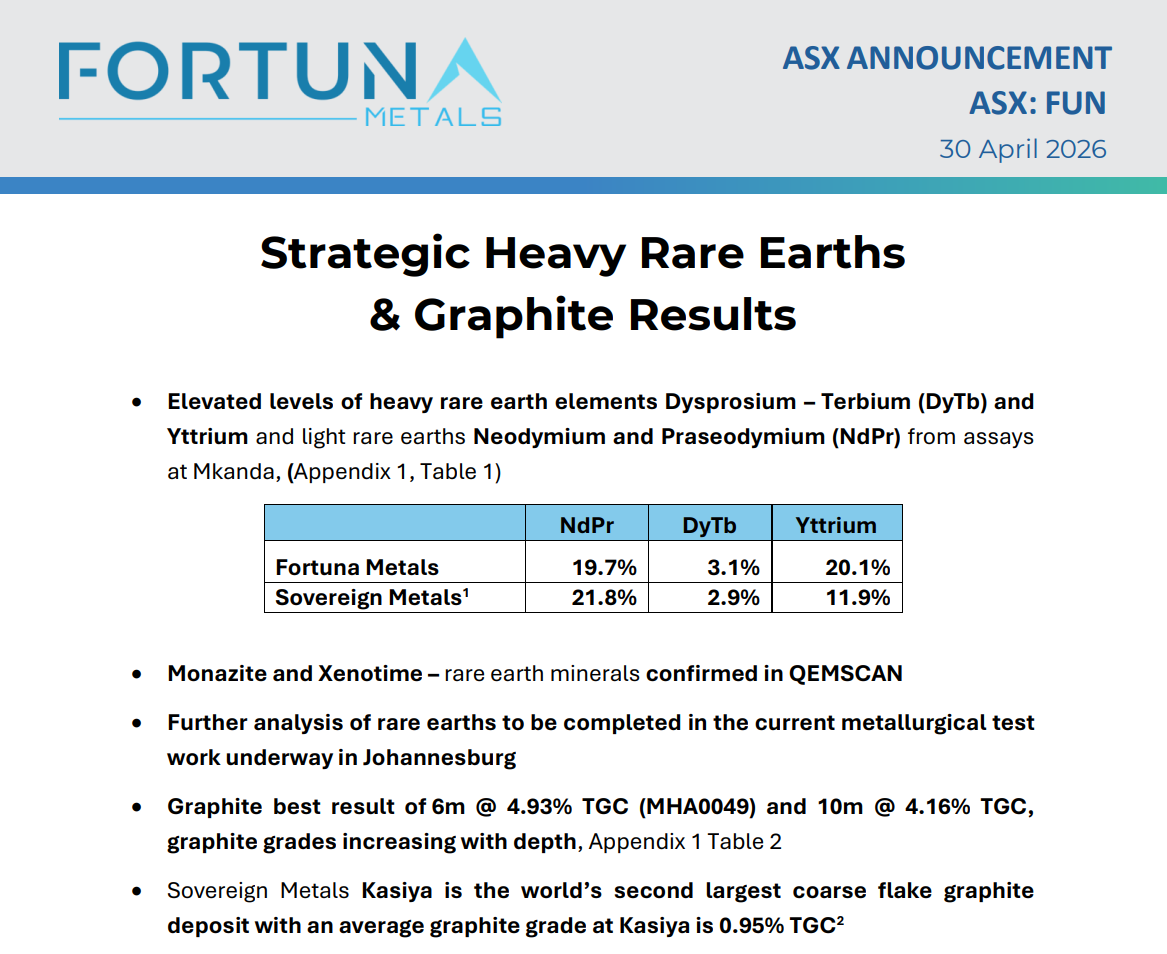

FUN’s first heavy rare earth assays at Mkanda came back with a basket that looks like Kasiya’s.

The chemistry alone doesn’t close a $430 million gap, but every step that confirms the geology runs further south makes it harder to argue Mkanda is a different beast.

Aircore drilling kicks off in the coming weeks. It goes much deeper than previous drilling, and graphite grades are known to climb at depth.

That’s where the graphite credits start to count.

With heavy rare earths on the board and graphite still to come, that valuation gap is starting to look stretched.

FUN vs SVM: How the Numbers Stack Up

Lining the assays up against Kasiya, FUN comes out in front on two of the three measures.

- Dysprosium-terbium came back at 3.1% versus SVM’s 2.9%.

- NdPr was a touch lower at 19.7% versus 21.8%.

- Yttrium nearly doubled SVM at 20.1% versus 11.9%.

The samples FUN sent off were originally being processed for rutile, the project’s main game. Heavy rare earths were tested as a side analysis from material that had already been through the rutile workflow.

That workflow uses a magnetic separator to pull out the different minerals.

Dial up the current and you grab more magnetic material. FUN ran theirs at 2.4 amps, the right setting for clean rutile. SVM used 2.9 amps when targeting rare earths at Kasiya.

In plain English, FUN picked up these grades while running a process tuned for a different metal. Push the current to where SVM had it and the grades likely go higher from here.

The lab work also picked up monazite and xenotime, the minerals that hold the rare earths in the rock and the same ones SVM found at Kasiya. The geology is reading the same.

When SVM confirmed its own heavy rare earth credits in January, the stock moved sharply, up nearly 30% on the previous days close.

FUN’s now sitting on its own version of that catalyst.

What These Rare Earths Are Worth

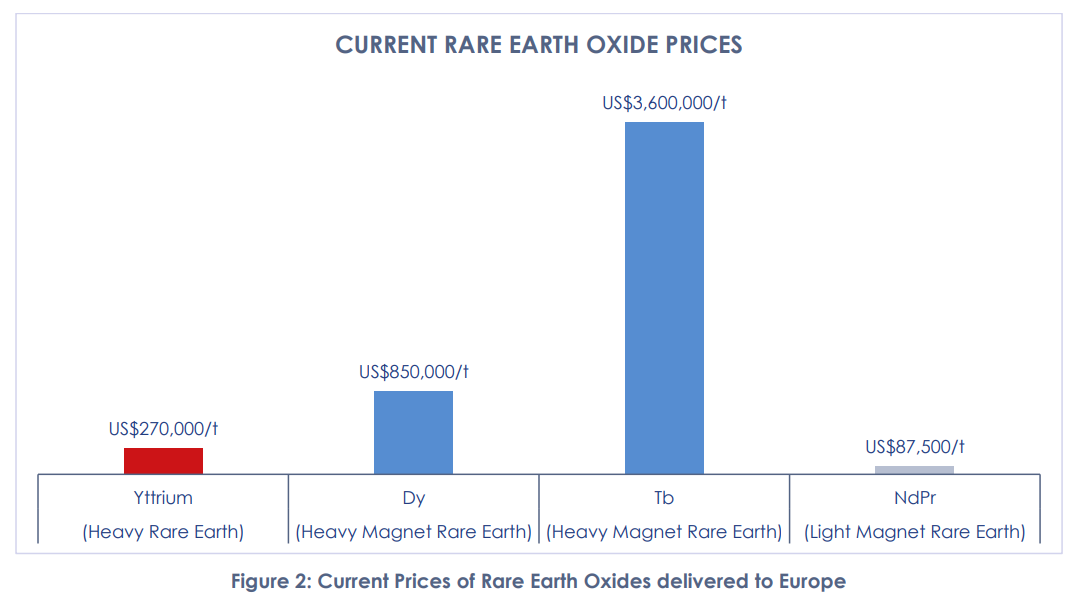

Dysprosium and terbium are heavy magnet rare earths, used in the high-temperature magnets that go into defence systems and precision weapons.

Q4 2025 prices in Europe sit at US$850,000 a tonne for dysprosium and US$3.6 million a tonne for terbium.

Yttrium goes into aerospace coatings and semiconductor manufacturing. The Q4 2025 price is US$270,000 a tonne, up roughly 4,000% on a year before.

The US imports 100% of its yttrium from China, and China has been tightening exports, so the US is looking for supply from another source.

There’s also a monazite by-product alongside the rare earths. Concentrate sells for over US$8,500 a tonne delivered to China and pulls out of the same processing flow at near-zero incremental cost.

That’s a third revenue line alongside rutile and graphite, with no extra capital required.

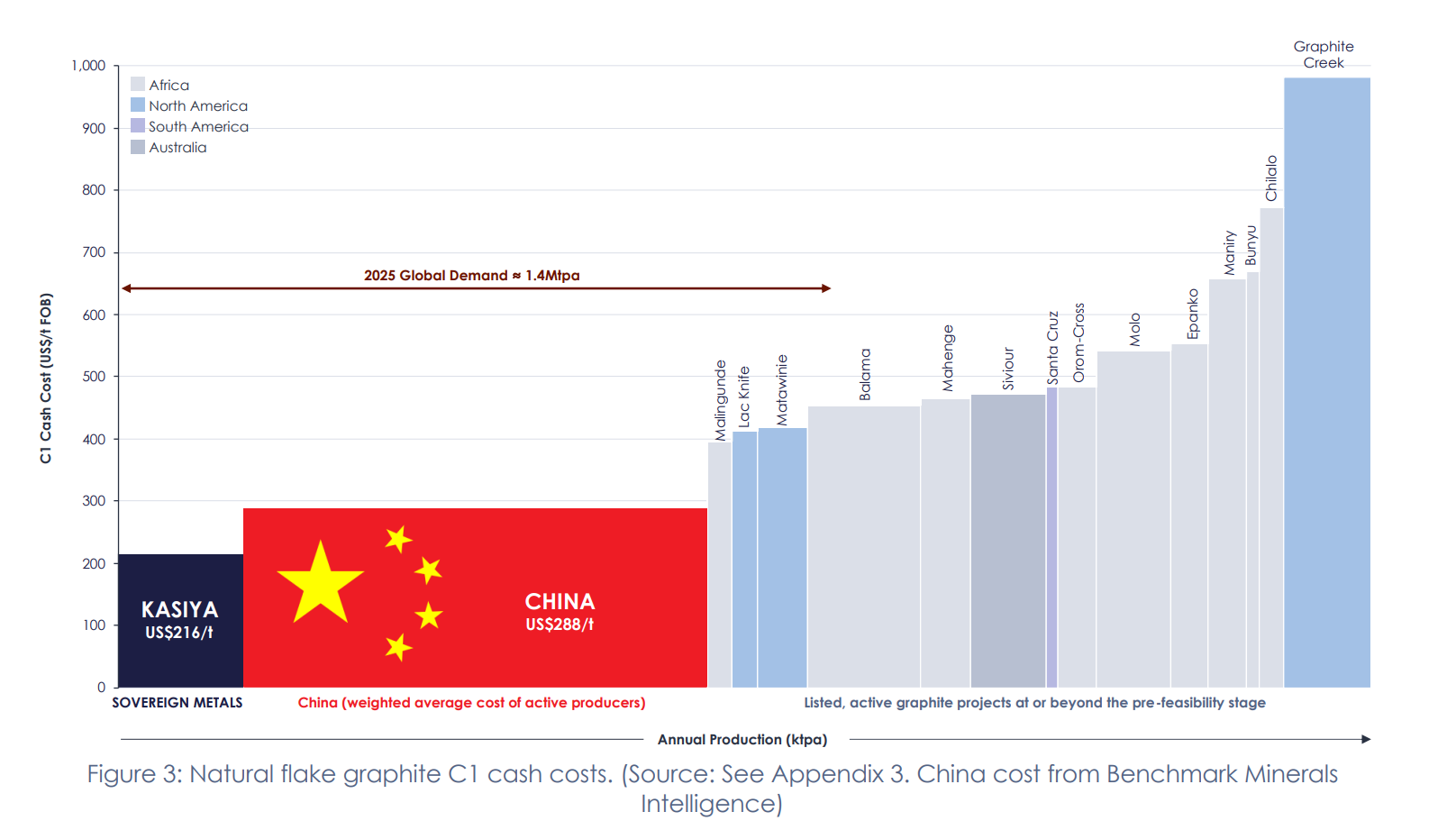

Graphite Builds With Depth

The graphite results came in alongside the rare earth work. The best hit was 6 metres at 4.93% Total Graphitic Carbon (TGC), the standard measure of graphite content in a rock.

Sovereign’s Kasiya is the world’s second-largest coarse flake graphite deposit. It averages 0.95% TGC.

Fortuna’s best Mkanda hits are running roughly five times that grade. A 10-metre intercept came in at 4.16% TGC, with plenty of other holes returning grades above 2%.

Another 115 hand auger holes are at Intertek in Zambia right now, with results flowing through 2026.

Grades have been climbing the deeper the drill goes, the same pattern Sovereign saw at Kasiya before aircore drilling confirmed the resource down at 20-30 metres.

Fortuna’s aircore rig kicks off in a matter of weeks and will tell us whether Mkanda’s graphite holds at depth.

Closing the Gap

SVM’s Kasiya ore reserve gets uplifted from 0.96% rutile to 1.51% rutile equivalent once graphite credits are added in. The graphite adds another 57% to the value of every tonne mined.

If Mkanda is Kasiya’s twin, similar arithmetic applies down here, and FUN’s graphite hits are running several times SVM’s grades.

FUN trades at 6-7% of SVM’s value on the same geology, with assays still to flow this year.

Aircore drilling and metallurgical results are next, and that valuation gap is looking out of step with what’s coming out of the ground.

General advice warning, disclosure and confidentiality notice

General advice warning

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consult your own investment advisor to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (“Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 1,554,000 FUN shares at the time of publishing this article. Equities Club has been engaged by FUN at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.