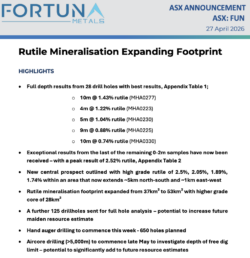

Three weeks ago, Fortuna Metals (ASX: FUN) put a maiden exploration target of 180 to 240 million tonnes on its Mkanda rutile project.

We said then it was a fraction of what was actually there. Today’s results are the first evidence backing that up.

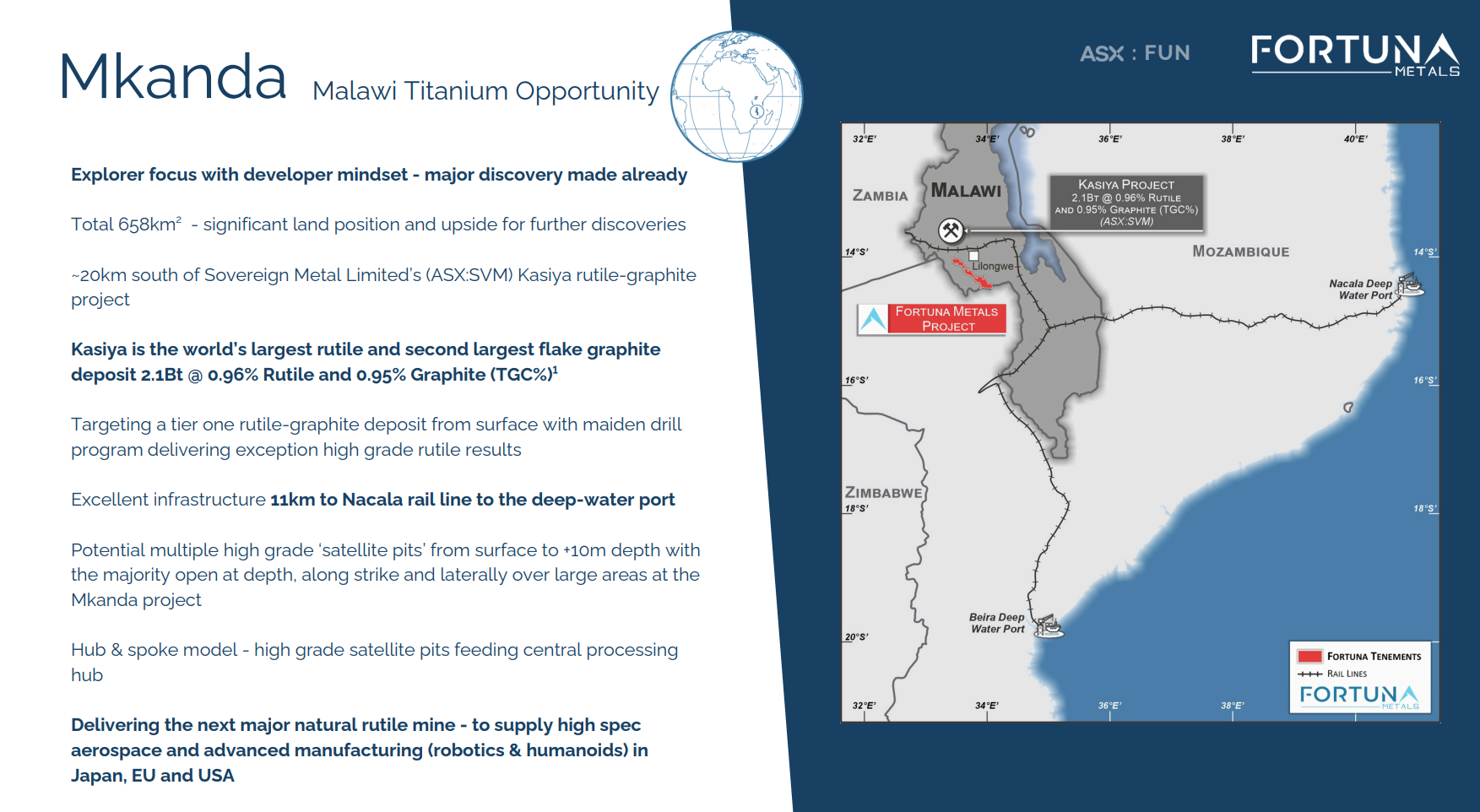

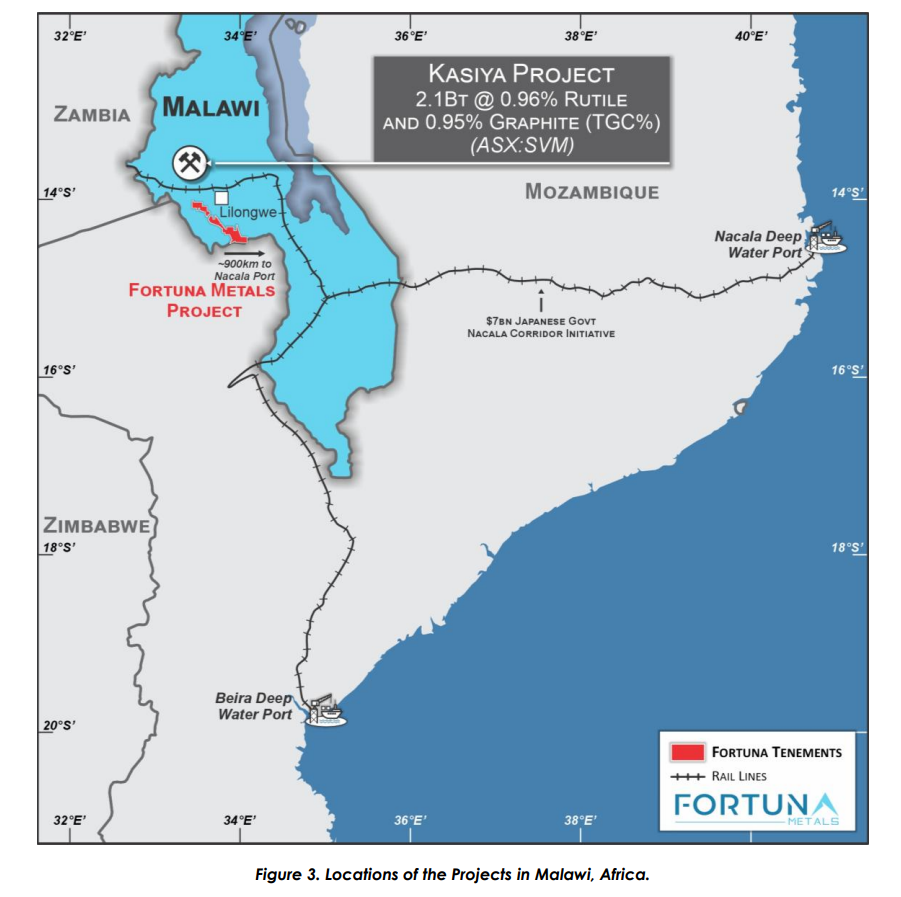

For new readers, FUN is the small-cap rutile explorer we added to the portfolio at 4c. Their ground in Malawi sits 20km south of Sovereign Metals’ (ASX: SVM) Kasiya deposit, the largest rutile deposit on the planet.

Same belt, much earlier in the story.

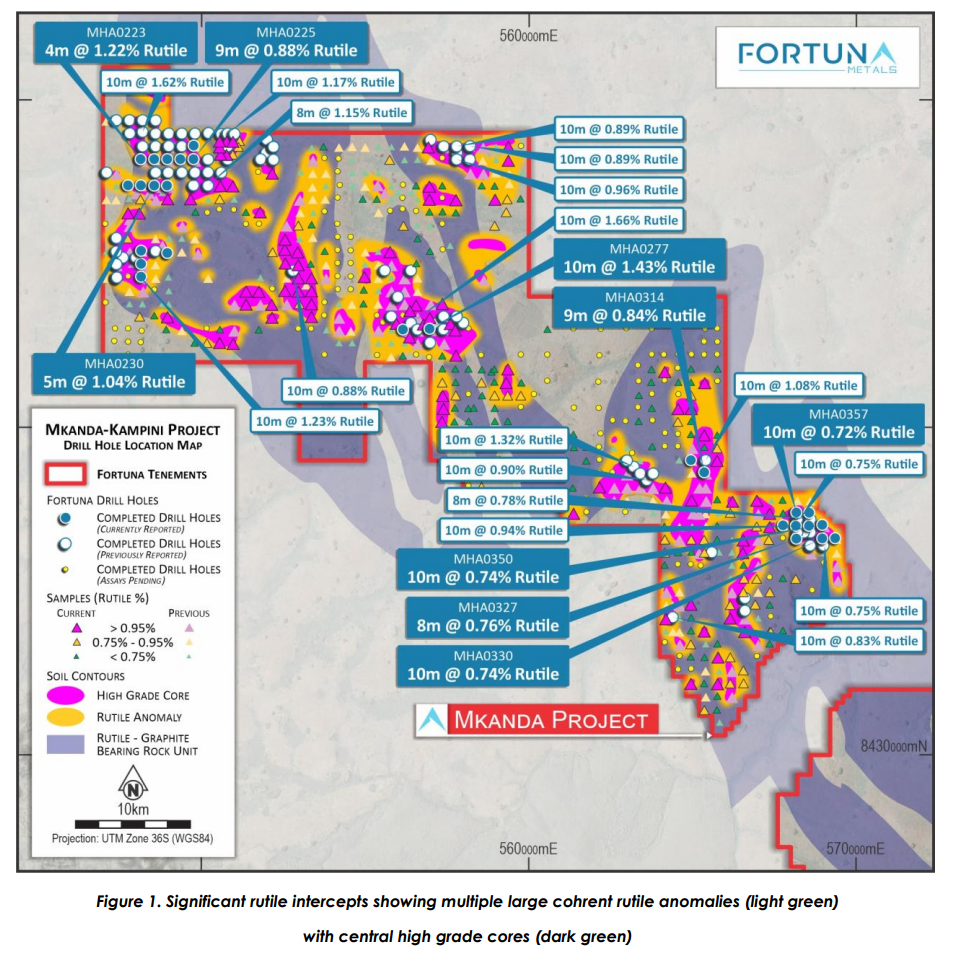

Mkanda’s mapped rutile footprint has pushed out from 37km² to 53km², a 40% expansion in a single batch of results. A 28km² high-grade core is taking shape inside it.

A brand new prospect has appeared in the centre of the project, with surface grades up to 2.5%. 73% of the latest 0-2m samples came back above the cut-off, averaging 0.9% rutile.

Best drill intercepts came in at 10m at 1.43% rutile, 4m at 1.22% and 5m at 1.04%, with surface samples peaking at 2.52%. Most of the 28 full-depth drill holes ended in mineralisation, meaning more rutile sits below where the auger stopped.

At 8.9c and a $25 million market cap, FUN still trades like an early-stage explorer despite an exploration target of 180-240Mt and 53km² of mapped rutile already on the board.

SVM is worth $460 million for the same belt of rocks.

Mkanda Rutile Grades Match Kasiya at Surface

Rutile is the cleanest natural feedstock for titanium, and the titanium market is tightening as defence, aerospace and robotics demand keeps climbing.

FUN’s ground sits 11km from a major rail line connecting to a deep-water port in Mozambique, so the export route is already there.

Today’s results pushed the system out further on both ends.

Fortuna’s new central prospect sits in the middle of the project, stretching about 5km north-south by 1km east-west. Standout surface grades came in at 2.5%, 2.05%, 1.89% and 1.74% rutile.

Up north, the Mbale prospect has stretched another 1.6km this batch, with shallow samples across the extension running at 1.5%, 1.07%, 1.01% and 0.94% rutile.

Twenty-eight full-depth drill holes also delivered, most of them ending in mineralisation.

That gives FUN two prospects expanding at once on opposite ends of the same project. Pair that with a 53km² footprint and the picture looks familiar, the same enrichment story that built SVM’s Kasiya into a 2.1 billion tonne deposit 20km north.

The first pass was a wide net by design. FUN punched out 675 holes on a 400m grid across 180km² to find where the rutile actually sits. With the hot zones mapped, the next round tightens to a 200m x 200m infill grid over the high-grade cores.

Rutile is showing up almost everywhere FUN puts a hole in the ground.

It’s the same playbook SVM ran at Kasiya, just earlier in the cycle and at a fraction of the share price.

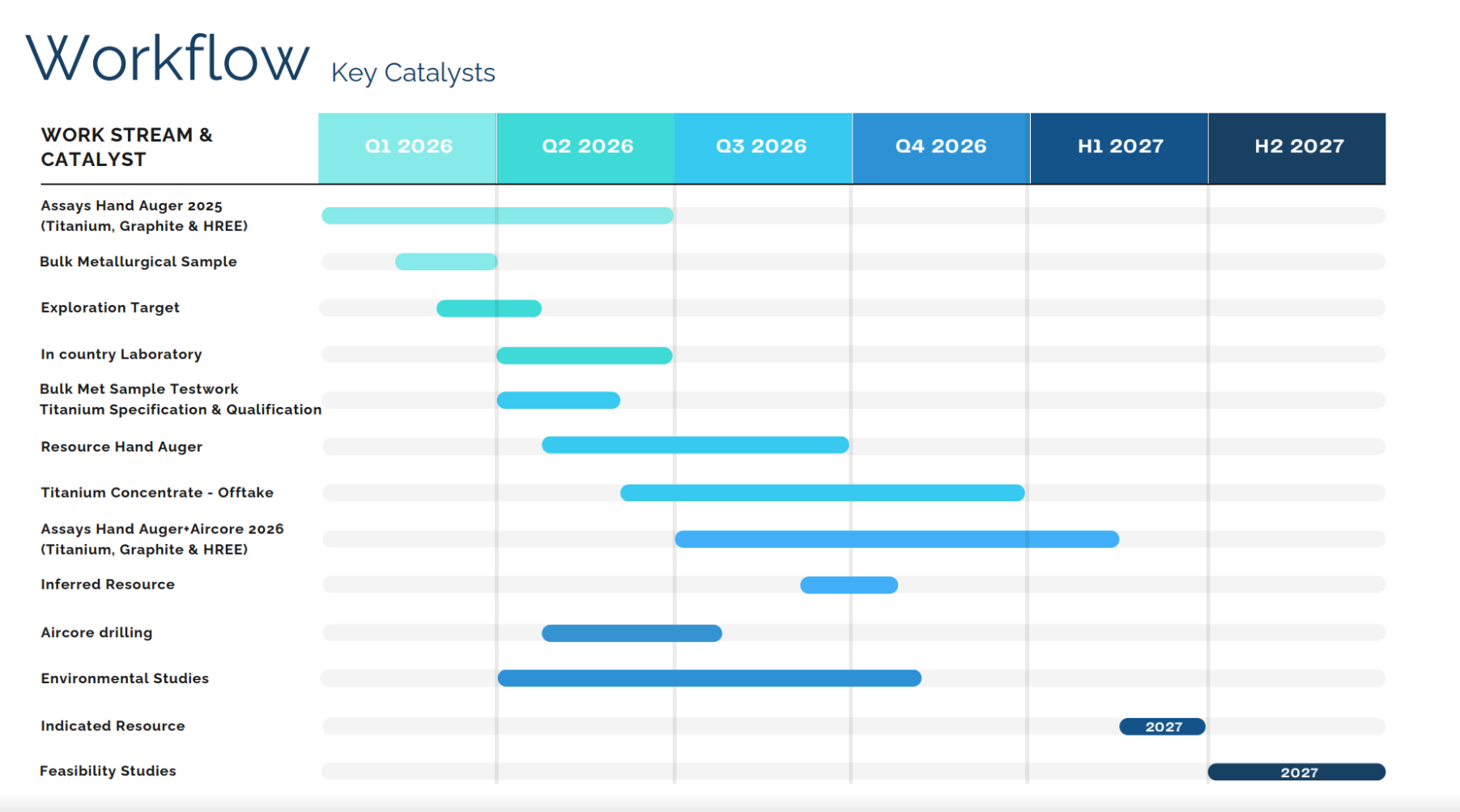

Aircore Drilling, Graphite Assays and Maiden Resource Timeline

Today’s update is one piece of evidence in a much bigger run. The numbers that can move FUN’s valuation are coming in the next two quarters.

The first is depth. Hand augers can only drill to about eight metres before the water table stops them. FUN’s current 180-240Mt exploration target is calculated on an average depth of just 4.1 metres.

At Kasiya, the rutile keeps going to 20-25 metres. SVM’s resource started at 644 million tonnes. After deeper drilling, it grew to 2.1 billion tonnes.

Aircore drilling starts at Mkanda in late May, with more than 5,000m planned. That’s the first proper look at whether FUN’s system holds at depth. If it does, the 180-240Mt target is the floor, not the ceiling.

The second is graphite. SVM’s ore reserve went from 1.03% rutile to 2.00% rutile equivalent once graphite credits were added. That’s the same rocks, with twice the payable mineral.

241 of FUN’s drillholes are already in the lab for graphite analysis, with results due Q2 to Q3.

There’s also a third commodity being tested from the same drilling, with rare earth results expected later this year.

On top of that, there’s a steady stream of rutile assays in the pipeline. 117 holes due mid-May, another 125 by end of June. All of it feeding into a maiden inferred resource estimate in the second half of 2026.

That’s a lot of catalysts for a $25 million company sitting on the same belt as a $460 million peer.

ASX:FUN’s Path From Explorer to Resource-Stage Rutile Play

Three weeks ago FUN had a maiden exploration target on the table. Today the footprint behind that target is 40% bigger, with a brand new high-grade prospect taking shape in the middle of the project.

The aircore rigs roll in next month to test depth for the first time. Graphite results land soon after. The maiden inferred resource is on track for the second half of the year.

The next six months decide whether FUN stays a $25 million explorer or starts closing the gap on a $460 million neighbour.

General advice warning, disclosure and confidentiality notice

General advice warning

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consulting your own investment advisor to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (“Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 1,554,000 FUN shares at the time of publishing this article. Equities Club has been engaged by FUN at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.