Most juniors grow a resource the expensive way. Raise money, turn a drill, pray the assays cover the spend.

Mount Ridley Mines (ASX: MRD) just grew its scandium hand out of a storage shed.

MRD’s Grass Patch Project sits about 25km north of the deepwater port at Esperance in WA, and already holds a sizeable scandium resource.

The company dug a batch of old drill samples out of storage and sent them back to the lab to be re-assayed for scandium. Those holes were drilled years ago, back when the ground was being chased for nickel and copper. The scandium in them was never measured at the time.

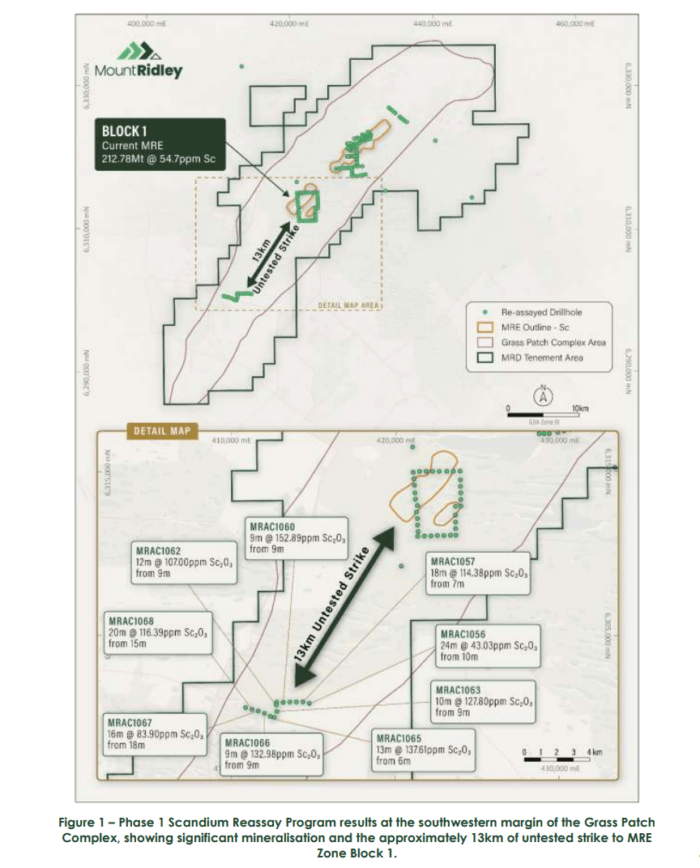

The numbers came back well above what is already defined. Block 1, the company’s central scandium zone, holds 155.2Mt at 91.8ppm Sc₂O₃.

The reassay beat that comfortably, with hits like 9m at 152.89ppm and 20m at 116.39ppm, both near surface.

The hits landed about 13km southwest of the current resource, on ground the resource doesn’t cover yet.

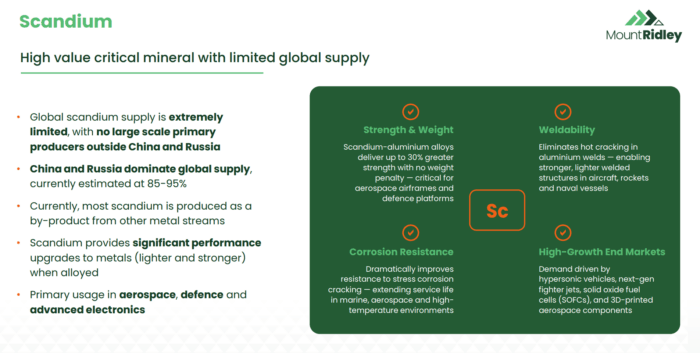

For those new to scandium, it goes into aluminium alloys for aircraft, defence platforms, fuel cells and 3D-printed parts, and for years it sat as a niche metal almost nobody chased.

That changed in April 2025, when China put it under export licensing and Western buyers in aerospace and semiconductors had to start finding supply somewhere else.

MRD is a portfolio company of ours and sits at 2.5c with a market cap around $35 million, a small company sitting on a large mineralised system it’s only now starting to map properly.

MRD Scandium Reassay Results

Phase 1 of the reassay covered 3,271 old air core pulps from across the Grass Patch Complex.

The scandium was in the samples the whole time. Nobody had thought to look.

When they finally did, the best holes came back well above the Block 1 resource average, and the strongest grades turned up right at the edge of the old drilling, where the resource runs out.

Some of the standout hits:

- 9m at 152.89ppm Sc₂O₃ from 9m

- 13m at 137.61ppm Sc₂O₃ from 6m

- 9m at 132.98ppm Sc₂O₃ from 9m

- 10m at 127.80ppm Sc₂O₃ from 9m

- 20m at 116.39ppm Sc₂O₃ from 15m

Grades are meant to fade as you walk away from a defined resource. You’ve drilled the good bit, the edges thin out, that’s how it usually goes.

At Grass Patch the opposite happened.

The numbers climbed the further out the holes sat, and the best of them landed right at the boundary of where anyone had bothered to drill.

That tells you the resource on the books could be the small end of what’s in the ground, and the company hasn’t found the edge of the system yet.

So for the cost of lab work, MRD has a fistful of near-surface scandium hits and a 13km corridor of untested ground pointing away from the resource. That corridor is where the drill goes next.

Why Scandium Supply Is Tight

Scandium is one of those metals almost nobody talks about until they can’t get it.

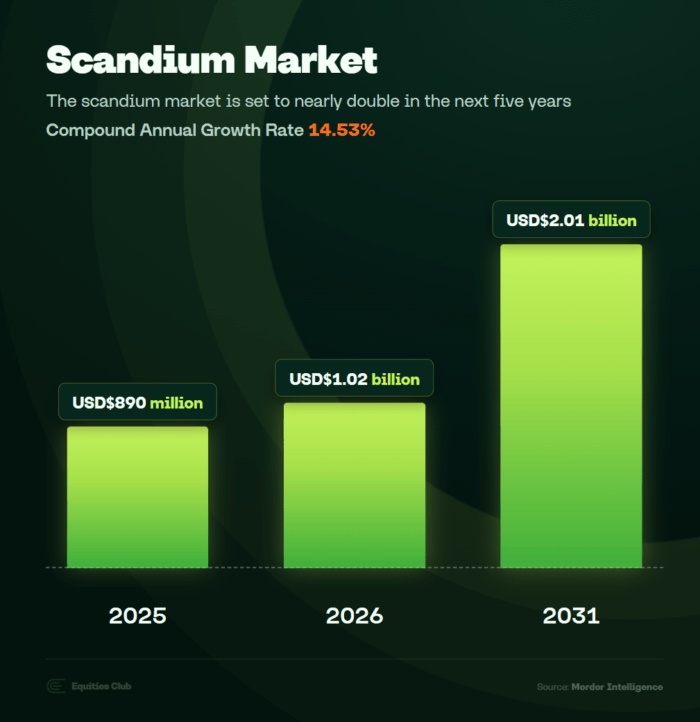

The entire world produces around only 25 tonnes a year (demand’s already more than four times that). Barely any of it comes from outside China and Russia, and most of what does get made is a by-product of mining something else, so nobody can just turn up supply when it’s needed.

And since that clampdown, the buyers who lean on it, aerospace and the chip makers, can’t count on the supply that used to run through Beijing.

Scandium sits around US$3,350 a kilogram, a different universe to the metals most ASX juniors dig for.

Demand is tipped to grow about 14.5% a year out to 2031, off the back of those same end uses, and there’s next to nothing new being built to supply it.

Mount Ridley says it holds one of the largest scandium resources going, 25km from a deepwater port in WA. That’s a lot of a scarce metal, in a country the West actually wants to buy from, right when that’s the one thing everyone’s chasing.

How Mount Ridley Mines (ASX: MRD) is Growing its Scandium Resource

Mount Ridley skipped most of the bill.

For most explorers this size, the cash goes out the door faster than the results come back, and plenty of good ground never gets tested because the money runs dry first.

Here the drilling was already done years ago, and someone else paid for it, the nickel and copper explorers who worked this ground long before MRD arrived.

The holes are in, the samples are on the shelf, and the only real cost left is the lab invoice.

There are roughly 14,000 more pulps still waiting, on top of the 3,271 already run. Each one is a cheap shot at a bigger resource, off holes already drilled and paid for.

And the results come back in weeks, not the months a new drill program usually eats.

For a junior trying to make a dollar stretch, you couldn’t script it much better.

The first batch goes straight into the resource model, with a real shot at lifting parts of the existing resource from Inferred to Indicated.

Phase 2 is being scoped now, pointed squarely at that 13km corridor where the best grades turned up.

What’s Next for Mount Ridley Mines

MRD calls itself an explorer, but it’s trying to become a developer, and this nudges it further down that road.

The honest read is that there is still a fair way to go. These are aircore hits inside an Inferred resource, and they need real drilling before anyone banks them. The strike is open and the 13km corridor hasn’t seen a rig yet.

A resource growing off 14,000 pulps already in storage, with no rig and no raise, is about as efficient as a junior gets.

The market still prices MRD like a plain-vanilla explorer, a shallow scandium system 25km from a port, in the one country every Western buyer wants to source from as they back out of China.

The next assays aren’t far off. Keep pulling numbers like these out of storage, with the drill still to come, and a $35 million valuation likely won’t hold.

General advice warning, disclosure and confidentiality notice

General advice warning

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consulting your own investment advisor to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (“Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 2,083,333 MRD performance rights at the time of publishing this article. Equities Club has been engaged by MRD at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.