Scandium is one of those metals the West is quietly worried about running short of. A pinch of it makes aluminium light and strong enough for fighter jets and missiles, and most of what little gets made comes out of China.

Which brings us to Mount Ridley Mines (ASX: MRD), a Western Australian minnow sitting on one of the biggest scandium resources on the planet.

The JORC number only went on that scandium in January, and at 2.2 cents and a market cap under $30 million, the story is still in its opening pages. Today’s news is the first move to do something with all that metal.

MRD has brought in the CSIRO to work out how you turn scandium in the ground into something an aerospace or defence buyer would pay for.

The program starts small and cheap, the right way for a tiny explorer to test a big idea without betting the balance sheet.

Mount Ridley (ASX: MRD) CSIRO Scandium Deal

The whole program costs $104,000, less than plenty of companies spend on a single drill hole, and MRD only covers part of it.

The CSIRO chips in up to $50,000 through its Kick-Start program, which co-funds projects with small Australian companies, and Mount Ridley pays the balance.

What the money buys is the CSIRO’s researchers working on Mount Ridley’s scandium, and a report the company owns outright at the end.

CSIRO’s team will map who holds the patents in scandium alloys, work out who supplies the metal and powder around the world, flag a couple of applications worth chasing, and take stock of the extraction and processing tech that’s starting to emerge.

If it turns up a market worth the trouble, stage two is where the alloy building would start.

The project runs out of Lab22, the CSIRO’s metal additive manufacturing facility. Additive manufacturing is the industrial name for 3D printing with metal, building a part up layer by layer instead of cutting it from a solid block.

It’s how aerospace and defence groups make parts lighter and stronger than anything you can machine.

Those same groups qualify an alloy first, then buy the metal behind it for years, sometimes decades. Get across the patents and applications before anyone else bothers, and your metal can end up being the one in the alloy.

And the report belongs to Mount Ridley, in a corner of the market almost nobody has staked out.

The CSIRO’s Commercial Track Record

Most retail investors don’t think much about the CSIRO when they weigh up a small-cap.

It’s Australia’s national science agency, and it has a long habit of turning lab work into money. The famous one is WiFi. CSIRO scientists cracked fast indoor wireless networking in the 1990s, patented it, and went on to collect around $430 million licensing it to more than 20 of the world’s largest tech companies.

The example miners will know is Titomic (ASX: TTT), which built its aerospace and defence printing business on cold-spray titanium technology licensed from the CSIRO, and still runs Kick-Start projects with them today.

A slice of that outfit is now on Mount Ridley’s payroll, for about the price of a Hilux.

“Our scandium resource is one of the largest in the world and we intend to do more with it than put it in a resource estimate.”

Allister Caird, Managing Director, Mount Ridley Mines

Mount Ridley’s Scandium Resource

The Grass Patch Complex, around 25 kilometres north of Esperance in Western Australia, hosts a JORC inferred resource of 367.98 million tonnes at 57.2ppm scandium, for roughly 18,555 tonnes of contained scandium metal.

The entire world produces somewhere between 15 and 25 tonnes of scandium a year. Take the top of that range and MRD is sitting on more than 700 years of global production, in farming country a half-hour drive from a deep-water port.

The scandium sits in the same weathered profile as the company’s heavy rare earth and gallium resources, so the same dig and the same plant could one day pull three critical minerals out together.

The current resource only counts the old drill samples that were assayed for scandium, and that’s a fraction of what Mount Ridley has in storage. The company kept a stack of historical sample pulps, the pulverised leftovers from years of drilling, that were never tested for scandium at all.

Those are now going back through the lab. Re-assaying pulps is about the cheapest way there is to grow a resource.

If the scandium shows up the way management expects, the resource can step up without a rig leaving the yard.

Why MRD is Taking it in Stages

We’ve watched plenty of small explorers announce grand downstream ambitions and burn half their cash on consultants before finding out whether anyone wanted the product. MRD is running this the other way around.

Spending capital on a scandium product before anyone knows the market or the patent gaps would be reckless, so Mount Ridley is paying a small bill to draw the map first.

The company can’t fund a full alloy development program yet, and doesn’t need to. It needs proof there’s a business at the end of this before committing to anything larger, and it’ll cost $104,000 to find out.

Aerospace, defence and robotics are the sectors in the frame, with the long-term aim being owned alloys, then partnerships and licensing income off the back of them.

That sort of thing takes years, and plenty has to go right along the way.

The Scandium Supply Squeeze

The 25-odd tonnes the world produces each year comes almost entirely as a by-product of nickel, titanium or rare earth mining.

A small amount of scandium turns ordinary aluminium into a lightweight alloy that holds its strength under heat and welds cleanly, which is why aerospace and defence buyers keep asking for more of it.

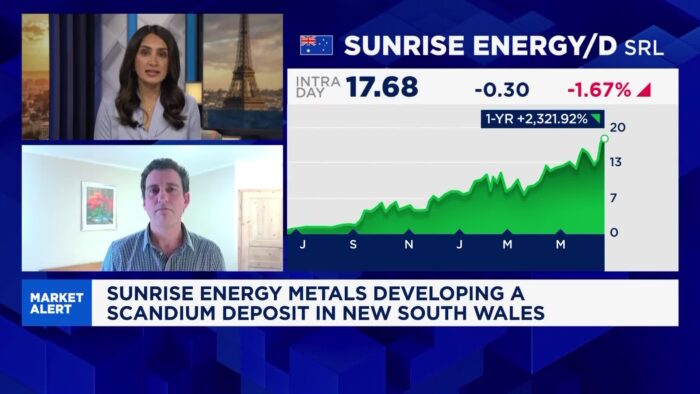

China controls something like 80 to 85% of global scandium supply, and it has been tightening export controls since early 2025.

Western governments and defence contractors have spent the time since scrambling for supply they can rely on, and no company has ridden that scramble harder than Sunrise Energy Metals (ASX: SRL).

Sunrise is turning its Syerston project in New South Wales into what would be the largest primary scandium mine outside China, and has already signed a multi-year supply option with Lockheed Martin.

SRL now carries a market cap north of $2 billion, after a rise of more than 2,000% over the past year.

Sunrise sits well ahead of Mount Ridley, with a finished feasibility study and a defence customer signed up, so the comparison only stretches so far. What it shows is the price the market puts on a Western scandium story once it starts to work.

Sunrise trades above $2 billion. Mount Ridley, with 18,555 tonnes of it in the ground, trades under $30 million.

Where This Leaves MRD

For $104,000, Mount Ridley has put its scandium in front of the country’s best materials scientists and keeps every page of what comes back.

There’s no revenue in it, and on its own it won’t grow the resource, though the pulp re-assays could do that separately. What it buys is a first look at where MRD’s scandium could actually end up, and who’d be paying for it.

The market has just handed Sunrise billions on that promise. At 2.2 cents, Mount Ridley isn’t priced for any of it yet.

General advice warning, disclosure and confidentiality notice

General advice warning

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consulting your own investment advisor to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (“Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 2,083,333 MRD performance rights at the time of publishing this article. Equities Club has been engaged by MRD at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.