Somewhere in eastern Ukraine right now, a drone you can carry in a backpack is hunting a Russian tank.

The drone cost a few thousand dollars. The tank cost millions.

That’s the war now.

In July last year, US Defence Secretary Pete Hegseth signed a memo moving small drones from one accounting category to another. They used to be classified the same way as fighter jets. Now they’re classified as ammunition.

Ordered by the case, and expended by the thousand.

That single memo changed the maths. Annual US military drone purchases ran at around 50,000 last year. They’re forecast to hit 300,000 this year, and over a million within a few years.

The FY27 US Defence budget earmarks US$75 billion for drones and counter-drone systems. NATO is targeting 5% of GDP by 2035. Europe has pooled US$870 billion for defence rearmament. Australia is in for A$22 billion over the decade.

This is the largest defence procurement cycle since the Cold War.

In 2019, an Israeli engineer named Dekel Keisar started a company. He’d spent his career at Israel Aerospace Industries, running the structural engineering on military drones at Israel Aerospace Industries, the country’s largest defence company.

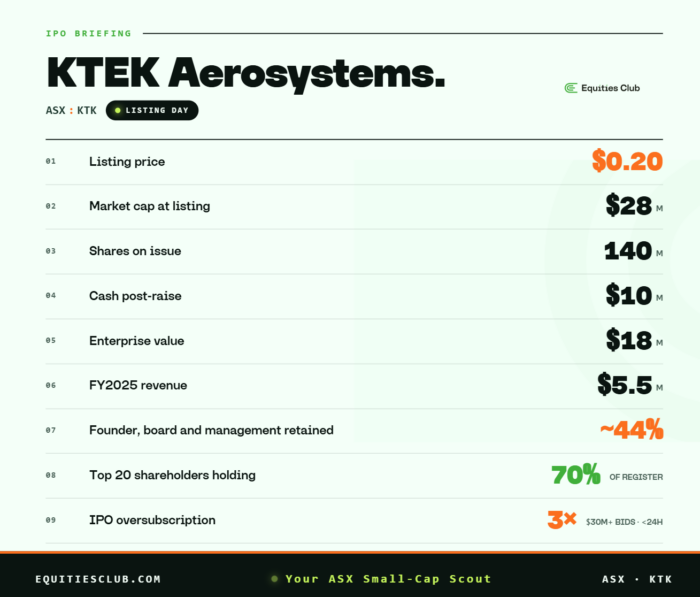

Seven years on, that company is called KTEK Aerosystems (ASX: KTK). It lists on the ASX today, and we’re adding it to the Equities Club portfolio.

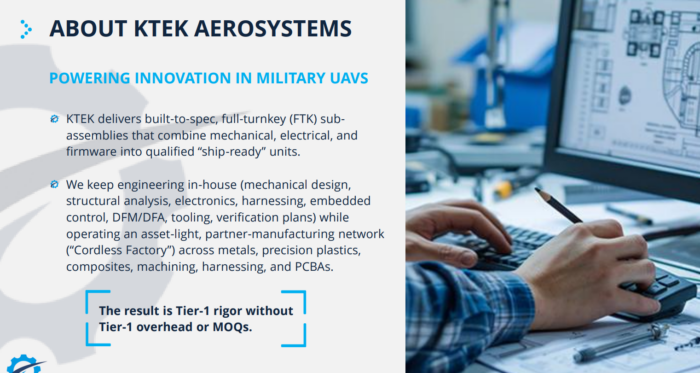

KTEK Aerosystems builds the parts that go inside drones made by other companies. That’s wings, frames, landing gear, electromechanical assemblies and structural sub-assemblies.

The names on the finished drones, Elbit, UVision and the rest, buy those parts from KTK and bolt them in.

Every drone they ship with KTK components inside is revenue back to KTK, without KTK needing to win a single government contract.

It’s the picks-and-shovels play of the drone boom.

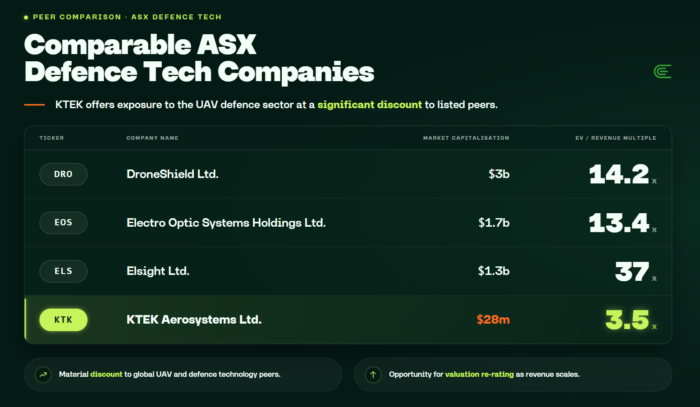

Today’s IPO values KTK at $28 million. The drone programs KTK supplies parts into have won more than $2.5 billion in contracts since 2023.

KTK is already pulling in more than $5 million a year in revenue, more than quadrupled in two years. Dekel still owns 36% of the company going in.

The $10 million raise for the IPO filled in under 24 hours. It was three times oversubscribed, with over $30 million in bids. Regal Funds Management, Thorney Investment Group and US-Israeli defence fund Scopus Ventures are all on the register.

The top 20 shareholders hold 70% of the company between them, so there won’t be much paper left this morning.

KTK lists today at 20 cents. We think the rest of the story is bigger than the share price.

What KTEK Aerosystems (ASX: KTK) Does

KTK builds the bits that go inside military drones.

That sounds simple. The engineering and supply chain behind it are not.

At the top of the chain sit the Tier-1 defence contractors. These are the companies that hold the government contracts, design the drone platforms, and ship the finished product to the military.

Think Elbit Systems, UVision, Textron and L3Harris. Their names are on the contracts and their logos are on the drones.

But they don’t build everything from scratch. No defence contractor does.

One layer down sit the Tier-2 suppliers. They build the components and sub-systems that go inside the drone. Airframes, wings, avionics mounts, electromechanical assemblies, power systems and landing gears.

The Tier-1 contractor takes those pieces, integrates them with software, sensors and weapons systems, and delivers the finished drone to the customer.

KTK is the Tier-2.

What KTK ships into a Tier-1 factory is what the company calls a “full-turnkey sub-assembly”. A ready-to-install drone section that arrives with all the mechanical, electrical and firmware components already integrated and tested. The Tier-1 bolts it in and moves on.

For the Tier-1, that saves months of engineering and production headache.

For KTK, it means they’re not competing with low-cost commodity suppliers on bolts and brackets. They’re delivering engineered systems that took years to design and qualify.

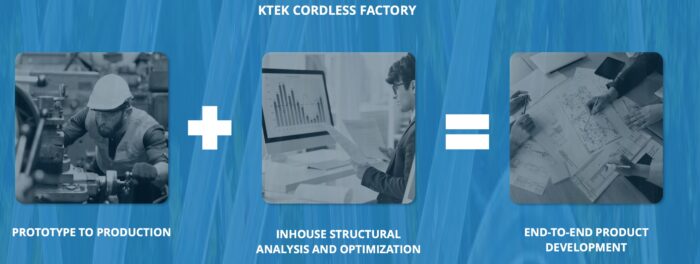

KTK’s Cordless Factory Model

Most defence manufacturers scale by building bigger factories. That eats capital and locks the company to one country.

KTK runs a different model. The company calls it the “Cordless Factory”.

The engineering, the design work, the quality control and the systems integration all stay in-house.

The physical manufacturing gets contracted out to a global network of certified aerospace partners across Israel, Portugal, the Netherlands and Australia, with US partners next on the list.

The model lets KTK scale production without building new plants. It can move work between facilities depending on customer location, capacity and geopolitics, while avoiding the capital intensity that crushes most early-stage defence manufacturers.

It’s how a company doing more than $5 million a year in revenue can already be supplying Tier-1 defence programs at scale.

The model works because Dekel and the team that built KTK came from the other side of the deal.

They spent years at Israel Aerospace Industries and consulting to the major drone manufacturers, working out from the inside what the Tier-1s actually want from a supplier.

The Cordless Factory lets them punch above their weight.

Why KTK’s Approved Supplier Status Matters

There’s a piece of the KTK story most retail investors will gloss over. It’s the words “approved supplier”.

Getting on a Tier-1 defence contractor’s approved supplier list takes between one and three years. You go through facility audits, AS9100 aerospace certification, prototype runs and small initial orders, with performance monitoring throughout, before the Tier-1 trusts you with any real volume.

Once you’re in, you’re hard to displace. Swapping out an approved supplier means putting a competitor through the same multi-year qualification process while disrupting an active production line.

The Tier-1 won’t do it lightly.

That’s why a $28 million company can credibly claim a place inside drone programs running $2.5 billion in contracts.

KTK is already inside the supply chains of the companies winning them, and getting another supplier in its place means rebuilding a multi-year process from scratch.

It’s the kind of edge that only gets built over years of work. KTK has already done it.

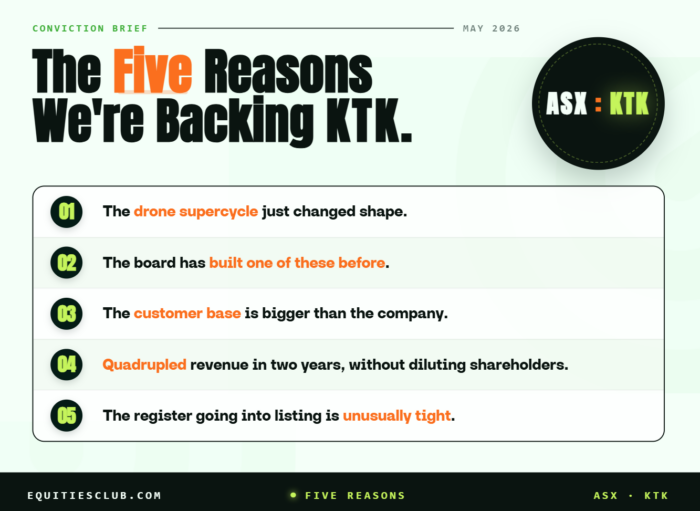

Five Reasons We’re Backing KTEK Aerosystems (ASX:KTK)

1. The Global Drone Procurement Supercycle

In July last year, the US Defence Secretary picked up a pen and changed how America buys drones.

Small drones used to be procured like fighter jets. Long contracts, big budgets, slow approvals, signed off by senior officers. Pete Hegseth’s memo moved them into the same accounting bucket as bullets. Cheap. Expendable. Bought by the case. Ordered by the unit commander rather than the Pentagon.

The numbers moved overnight from the memo.

The Defence Autonomous Working Group inside US Special Operations Command had a US$225.9 million annual budget last year. The FY27 budget request hands it US$54.6 billion. A 240-fold jump to a single line item, in 12 months.

The US Army wants a million small drones. The Pentagon’s separate Drone Dominance Program wants another 200,000 by 2027. Total US military drone purchases ran at 50,000 last year. They’re forecast to hit 300,000 this year, then over a million within a few years.

The companies whose names are on the finished drones get the headlines. The Tier-2 suppliers underneath them ship the volume.

Volume procurement rewards suppliers who are already qualified, already integrated into production lines, already shipping into platforms the US military has approved.

KTK is already inside.

2. A KTK Board With an ASX Drone Track Record

In 2017, an Australian-listed company called Elsight (ASX: ELS) came to market with a $18 million valuation. It built radio communications for drones.

The chairman who’d helped bring it there was a former semiconductor executive named Howard Digby.

Elsight today is worth about $1.5 billion.

Roughly 80 times the IPO valuation over eight years, in the same broad sector KTK is listing into today. Howard’s been on plenty of boards that didn’t 80x. He’s a Non-Executive Director ofr one drone-adjacent ASX small-cap.

For KTK he is the Chairman.

Director Chris Baxter sits on the operational side of the table. He’s advised Skyeton, a Ukrainian drone manufacturer shipping platforms straight into the war.

Ukraine is the most heavily combat-tested UAV environment on the planet right now, and the lessons coming out of it are reshaping how every Western military thinks about drones.

Non-executive director Winton Willesee sat on the board of DroneShield (ASX: DRO) through its early scaling years.

Three directors. Three ASX drone stories that became serious ones. That isn’t common at the $28 million end of the market.

3. KTK Customers Hold $2.5 Billion in Drone Contracts

A $28 million company sits inside customer contracts worth more than $2.5 billion.

That single ratio is the most striking thing on the KTK page.

KTK’s two existing public customer relationships are UVision and Elbit Systems, two of the most established names in the Israeli defence drone industry.

Both names mean a lot in the global drone space, but neither is a household name in Australia, so it’s worth a quick translation.

UVision is planning a Nasdaq IPO at a multi-billion dollar valuation. Its closest US-listed comparable, AeroVironment (NASDAQ: AVAV), is valued at around US$12 billion. Then there’s Shield AI, raising fresh capital at the same US$12 billion mark. Leonardo DRS (NASDAQ: DRS) sits at roughly US$10 billion.

Elbit Systems is one of Israel’s largest defence contractors, listed on both the Tel Aviv and NASDAQ exchanges with a market cap around US$25 billion.

That’s the calibre of company KTK is supplying parts to.

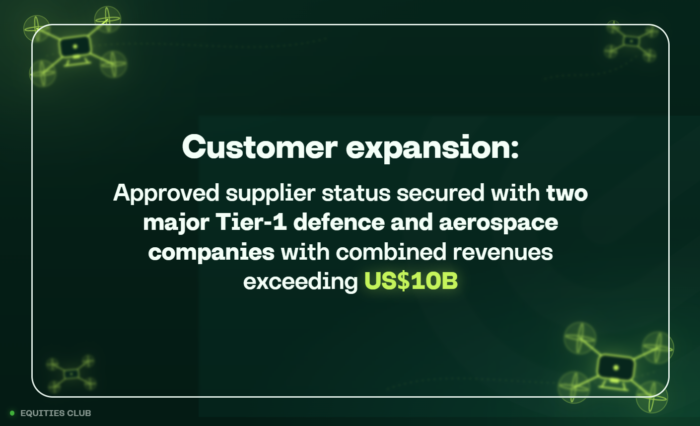

On top of the existing book, KTK has approved supplier status with two more Tier-1 defence and aerospace groups, with combined revenues over US$10 billion between them. Initial purchase orders are expected.

The $2.5 billion customer order book matters more than the headline number suggests. KTK is already inside the supply chains of the contractors winning the contracts, and that’s the part you can’t replicate at IPO from outside the industry.

4. KTK Revenue Quadrupled in Two Years

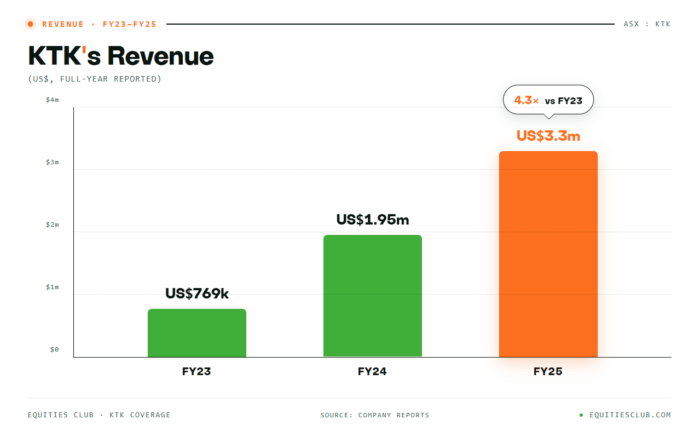

KTK’s revenue went from US$769k in FY23, to US$1.95m in FY24, to US$3.3m in FY25. In Australian dollars, that’s around A$5.5 million in FY25.

A 107% compound annual growth rate, and revenue has more than quadrupled in two years.

Most ASX companies celebrate 20% annual growth in a good year. KTK is growing five times faster than that, and onboarding Tier-1 defence contractors at the same time.

Usually that kind of growth at a small-cap manufacturer means going back to shareholders for cash, again and again, to fund the next stage of growth and the next customer ramp. Existing holders get diluted on every raise.

KTK has grown without doing that once.

The model is built to produce a margin profile closer to an engineering business than a manufacturer, and growth that doesn’t depend on tapping shareholders every time a customer ramps an order.

5. KTK’s Share Register and Institutional Backers

Regal Funds Management anchored the KTK seed round in late 2025. They came back for the IPO in 2026.

Regal is the alternatives arm of Regal Partners (ASX: RPL), with $20.9 billion in funds under management, and backing the same company twice at two different price points is about as clear a signal as a fund manager gives.

Alex Waislitz founded Thorney Investment Group in 1991, sits on the AFR Rich List with an estimated net worth around $1.5 billion, and has one of the longest small-cap track records in the country. Thorney is in.

Anton Tagliaferro founded Investors Mutual in 1998 and built it into one of the most respected value houses on the ASX.

His family office TGI Holdings is on the KTK register, and he gave the AFR his read on the listing directly: a “picks-and-shovels play to help facilitate the rapid acceleration in drone production driven by strong demand from defence departments globally.”

Scopus Ventures is a US-Israeli defence and technology fund. Specialist money that looks at defence supply chains for a living. Scopus putting capital into a Tier-2 UAV supplier listing on the ASX is a direct vote on KTK’s engineering and customer relationships.

VP Capital and Cyan Investment Management rounded out the institutional book. Both have spent years picking small-cap names that worked.

Add it all up. KTK has 140 million shares on issue at listing. Board and management hold roughly 44%, locked up. The top 20 shareholders hold around 70% of the register between them. Institutions own about half of what’s left.

That leaves a tiny free float with the potential to move aggressively if the market starts understanding what may be building here.

There isn’t much paper for retail this morning, and the names already holding it aren’t the kind that sell early.

What we’re watching

A few specific things from listing day forward.

- The first purchase order from a new Tier-1. Approved supplier is the hard yards. The next step is converting that into a purchase order, then a second one, then a supply agreement that locks KTK in across a multi-year platform. Each step is a chance for the market to re-rate the stock.

- The US partner network. American drone procurement is the single biggest piece of the global cycle, and a lot of that money will require domestic manufacturing or US-located supply chains. KTK has flagged the US as its next manufacturing geography. The faster they get a certified US partner online, the more programs they’re eligible for.

- New customers beyond UVision and Elbit. The existing book is concentrated in two names. Every new Tier-1 relationship that turns into revenue opens up more of the market.

- Revenue scaling without major capital raises. The Cordless Factory model is built to allow this. If it works, KTK compounds revenue without going back to shareholders for cash. If they need to raise to fund the next ramp, that’s a different story.

Risks

- Customer concentration. UVision and Elbit dominate the current book. If either pulls back, or the geopolitics around their end-customers shift, KTK feels it directly.

- Geopolitical exposure. KTK was founded and operates substantially out of Israel. Engineering and a chunk of production stays where the talent is, and the region remains a high-risk operating environment.

- Tight float volatility. Limited paper amplifies upside when momentum is good. It can also amplify downside when sentiment turns.

Our view

Years ago, Dekel Keisar looked at the defence industry and bet against everything it stood for.

Every major player was building bigger, more expensive flying platforms. Multi-million dollar drones with multi-year delivery schedules. Dekel thought the future was the opposite. Drones you could build by the thousand.

In 2026, that’s the type of war being fought in Ukraine. That’s the procurement decision the Pentagon just made. That’s the volume problem every Western military is now staring at.

Dekel built KTK to supply the future he saw coming. The future has arrived.

KTK lists today at $28 million. Doing more than $5 million in revenue, growing at triple digits, customers running $2.5 billion in active drone contracts, and three directors who’ve each been inside an ASX drone story that became a serious one.

Most ASX listings ask the market to believe in something that might happen. KTK is asking the market to look at what’s already happening, and price it.

KTK rings the bell this morning at 20 cents. Wheels up.

General advice, disclosure and confidentiality

<p data-pm-slice=”1 1 []”>General advice warning</p>

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consulting your own investment advisor to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (”Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 500,000 KTK shares. Equities Club has been engaged by KTK at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.