Is the demand for lithium still increasing?

Lithium stocks have been belted over the past year. The sector’s gone from hero to heavily discounted, and people are wondering whether the demand story’s finished or just taking a breather.

The lithium oversupply narrative has taken hold lately, but is it justified? Understanding what’s really happening requires looking beyond the price action at the demand and supply dynamics.

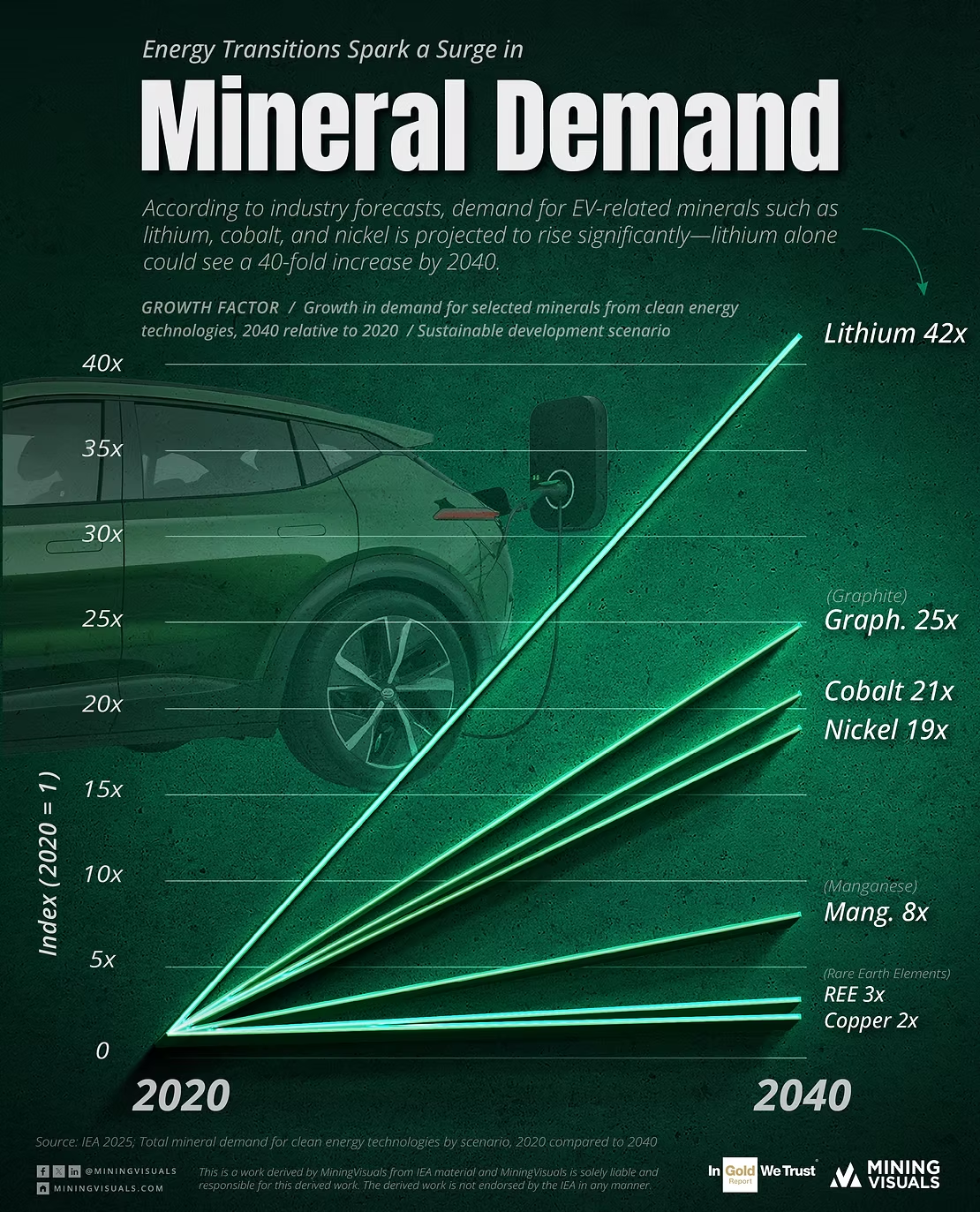

Yes, lithium powers electric vehicles (EVs). But it’s not just about cars anymore. Battery tech is broadening. Grid-scale storage, renewables and other industries are picking up the slack just as car sales slow.

Twenty years ago, lithium was little more than a pharmaceutical niche – doctors prescribed it for bipolar disorder and depression. It was a tiny market with steady demand. AKA, nothing that got commodity traders excited.

Then, Elon arrived.

What’s driving this demand?

Tesla changed everything. Suddenly, everyone needed lithium, and car makers found themselves competing with battery manufacturers for long-term supply deals they’d never had to think about before.

Governments also piled in on EVs, announcing deadlines for phasing out petrol and diesel cars over the coming decades.

That shift is still happening, just more slowly than many expected.

Consumers are hesitating. Cost of living’s up, interest rates are high and charging infrastructure is patchy at best (try finding many working chargers in regional Australia). Some governments have pulled back on subsidies too, which isn’t helping.

These headwinds have slowed the pace of EV adoption but haven’t stopped it entirely.

China still drives most lithium demand – they’re the world’s largest car market by a mile. But even the Chinese are experimenting with alternatives like lepidolite in battery production, once again slowing the demand for lithium.

Meanwhile, new demand sources are emerging.

Grid-scale battery energy storage systems (BESS) are becoming another major lithium consumer. These batteries store power from the grid and disperse it in peak periods, taking pressure off existing grids. This is particularly important in developed countries where ageing power grids are now faced with increasing demand.

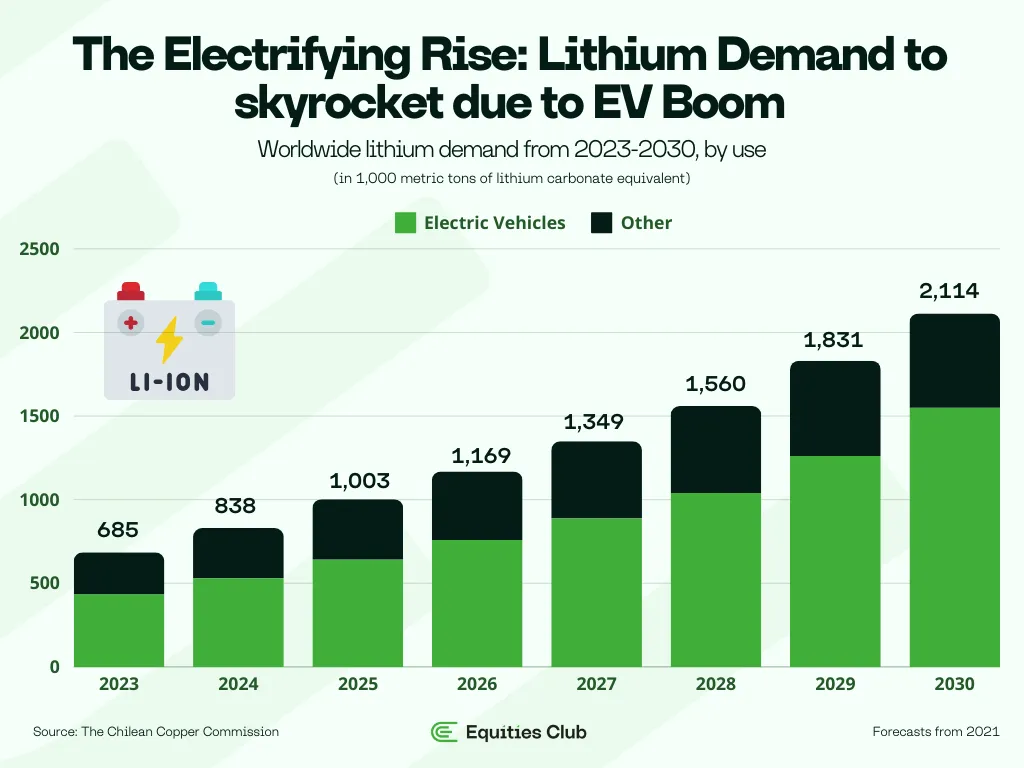

Most lithium demand forecasts still point to strong growth through the 2030s, driven by both transport and storage sectors.

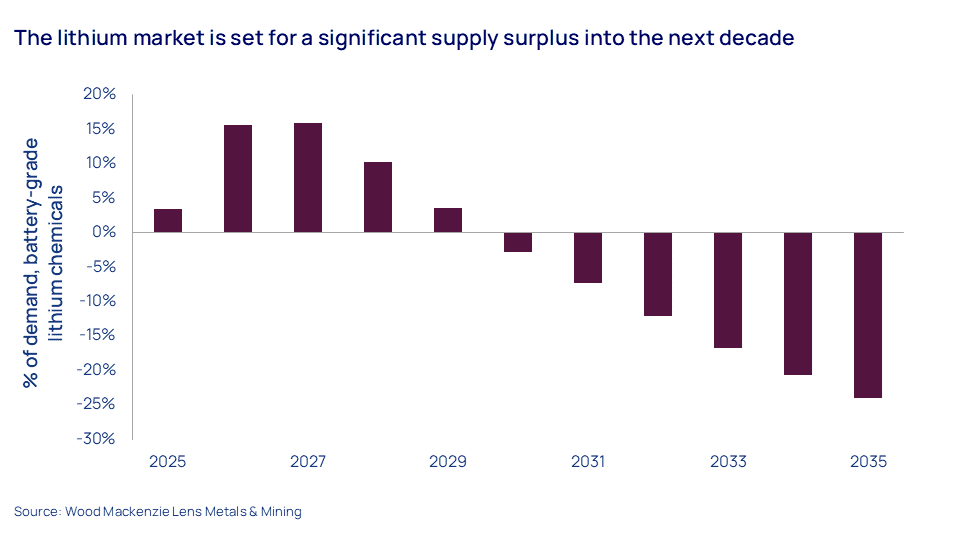

Demand’s still growing. Supply just beat it to the punch. As lithium prices fall, many investors believe demand has stopped; this is categorically wrong.

The lithium market remains small and immature compared to other commodities. When new supply floods the market faster than demand can absorb it, prices fall even though total consumption continues rising. It’s basic economics, but it confuses investors watching lithium company share prices crater while lithium usage hits new records.

Where is the lithium supply coming from?

The days of a few lithium producers controlling the market are done. Supply is pouring in from every corner. Australia, South America, West Africa, Canada, the US, Spain and more. If there’s lithium in the ground, someone’s drilling it.

Historically, lithium supply came primarily from two types of deposits: hard rock spodumene, found mainly in Australia, and lithium-rich brines, mostly in South America’s ‘Lithium Triangle’ of Chile, Argentina, and Bolivia. For years, these two regions controlled global lithium production and supply.

Australia remains a major player, with world-class deposits still being discovered. Supply has increased substantially from Australia, with many mines coming online during the price peaks, only to be put into care and maintenance as prices fell.

Argentina is seeing a flood of investment in brine projects, with companies like Rio Tinto now investing heavily thanks to government reforms and rising foreign capital. The large brine operations in South America are low-cost and can be scaled quickly, keeping a lid on pricing.

Mali, West Africa, has also become a major supplier of lithium, with one of the world’s top five hard rock lithium deposits discovered and now in production.

With deposits being found in Canada, the USA, Spain, and the Democratic Republic of Congo, it is clear that the pipeline to develop projects for years to come will remain strong.

China, the dominant force in turning lithium into batteries, is also looking to expand its domestic supply with aggressive exploration.

Lithium goes through a complex conversion process before it ends up in batteries. Raw lithium gets transformed into battery-grade chemicals like lithium hydroxide and lithium carbonate.

Not all lithium can convert into battery-grade, with discovered deposits having to undergo extensive metallurgical testing to ensure the quality of the product.

China dominates the processing market, which gives them enormous buying power. They can basically dictate terms, cherry-pick the best projects and even muscle their way into mine development deals.

Many question the role recycling of lithium batteries will play in years to come. When lithium was trading at high prices, everyone was talking about recycling batteries. Now that prices have collapsed, suddenly nobody’s interested in spending money on recycling technology. Funny how that works.

Supply has become the main culprit behind falling lithium prices. This oversupply of lithium has overwhelmed even bullish demand projections and pushed weaker producers to the brink.

Mining operations are being mothballed left and right (care and maintenance is the polite industry term) to let demand catch up.

For investors, both sides of the equation matter. Demand growth is nice, but supply dynamics can determine whether you make money. Low-cost producers in stable countries are the ones most likely to be able to ride out the ups and downs of future lithium price fluctuations.

Is there a possibility that we’ll be facing an oversupply?

Supply has grown much faster than demand, and when that happens, prices fall. It’s Economics 101.

The lithium market is absolutely exhausted. A few years back when prices were screaming higher and supply was tight, everyone was making money. Discoverers, producers, and most importantly – investors.

Mining companies have since thrown billions at new projects around the world. The result was a massive wave of new supply that hit markets faster than anyone expected, completely swamping demand.

Demand has been growing steadily, sure, but the rush to build new projects meant supply outstripped it easily. Even the conversion facilities in China (where most mined lithium gets processed) are nearing capacity. Their appetite for more lithium has almost vanished.

With Chinese facilities maxed out, the first Australian operations to shut were the high-cost producers. Those large margins that were made during boom times are now gone, with many unable to turn a profit.

The South American brine operations, which take longer to come online but are able to produce cheaper than hard rock deposits in Australia, are maintaining operations with reduced profit margins.

The outlook for lithium prices remains pretty grim. Any bump in demand gets filled immediately by existing mines or mothballed operations that can restart pretty quickly when needed.

There’s still a massive pipeline of new lithium projects being planned across multiple countries. Getting them built is another story. Banks don’t want to touch new lithium projects while prices are on the floor.

If you’re still keen on lithium stocks, stick to the low-cost producers with decent balance sheets and world-class deposits. Cheap explorers might look tempting after getting absolutely smashed, but buying speculative miners during commodity crashes can end badly.

Even the biggest lithium bulls admit there’s way too much supply around right now. The smart money is focusing on the survivors – companies that can weather this downturn and be positioned for when the cycle eventually turns.

What does a lithium oversupply mean for lithium prices?

People love overcomplicating the lithium market, but it’s actually pretty straightforward. Supply and demand drive prices, just like any other commodity. When supply grows faster than demand, prices collapse.

Battery-grade lithium dropped from US$80,000/t to under US$8,000, which is a crash by any definition.

This is a direct result of new supply flooding the market trying to take advantage of those high prices.

There’s an old investing saying: “The cure for high prices is high prices.” Basically, when something gets expensive enough, everyone rushes in to produce more of it, which kills the price. Lithium just lived through a textbook example.

The market’s already flooded and Chinese converters are full. There’s no appetite for new supply.

It also makes it a buyer’s market with Chinese facilities now able to name their price when negotiating with mining companies because they know producers need to sell.

The days of the US$80,000/t lithium are firmly gone; the $8,000/t raw mined lithium are also long gone. Australian producers are now selling at around US$650 per tonne, which has completely wiped out profit margins. Survival now means running the most efficient operation possible.

The next few years look pretty tough for lithium pricing. Existing mines can ramp up production easily if demand picks up, making any price recovery unlikely this decade.

If you’re still determined to own lithium stocks, focus on the absolute lowest-cost producers. High-cost operations are already toast, and marginal producers are barely hanging on. The companies that survive this downturn will be the ones positioned to benefit when the cycle eventually turns.

Financial discipline, research and tracking pricing are imperative for a high-risk investment such as lithium in the current market.

What does this mean for lithium investors?

Being a lithium investor right now is pretty miserable. Prices are low, supply is everywhere, and even the best-run companies are struggling to deliver decent returns to shareholders.

And even then, wider sentiment can still punish the strongest names. Fundamentals are hard to ignore, and right now they’re grim.

If you’re hunting for quick gains, lithium stocks are absolutely the wrong place to be looking right now.

Explorers can’t raise a dollar to save themselves, and producers are watching their revenues get decimated. Lower margins mean many operations are scaling back production or going into care and maintenance (industry speak for temporarily shutting down).

Lithium company share prices have been absolutely demolished. Pilbara Minerals, considered the benchmark of Australian lithium, has fallen 75% from its highs.

Tough markets separate the survivors from the casualties, and we’re seeing that play out in real time. Some producers are even begging governments for help to stay operational. They want reduced royalties (the fees companies pay governments for mining rights), but that’s just a band-aid solution.

If you came here looking for tips on the next lithium boom stock, this probably isn’t what you wanted to hear. But you might have just saved yourself some serious money by understanding the reality of this market.

Of the few remaining lithium companies on the ASX, look for the lowest-cost producer with the highest margin and with minimal debt.

Avoid high-cost operations entirely. And don’t get pulled in by companies promising breakthrough tech or processes. In commodity markets like this, boring efficiency beats innovation every time.

Do your homework thoroughly – read company presentations with a critical eye, check what both bulls and bears are saying and understand that this downturn could drag on for years. The companies that survive will eventually benefit when the cycle turns, but picking the survivors requires careful analysis.

In Summary

Lithium demand keeps growing, but supply is growing much faster, and that’s going to keep prices suppressed for years. EV adoption and grid-scale battery storage are both expanding, but not nearly fast enough to soak up all the new lithium hitting the market.

This oversupply has caused the collapse of lithium prices, raw materials, and lithium chemicals. Conversion facilities in China currently have no appetite for lithium, while the cheapest producers, South American brines, are operating at very tight margins.

The glut is unlikely to ease this decade, and share prices of ASX lithium stocks have plummeted, with even market leaders down 75%.

This is a lithium market where only the leanest survive. Focus on low-cost, tier-one producers – or get ready to bleed.

Even then, our strong belief is that lithium prices will remain low for some time, putting pressure on even the most efficient companies. Any mistake in this market and your investment is likely to get punished dearly.

Want to stay ahead of the next turn in the cycle? Join the Equities Club newsletter – we track small caps, supply shocks, and everything in between. No fluff. Just what matters.

General advice warning

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consulting your own investment advisor to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (“Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products.