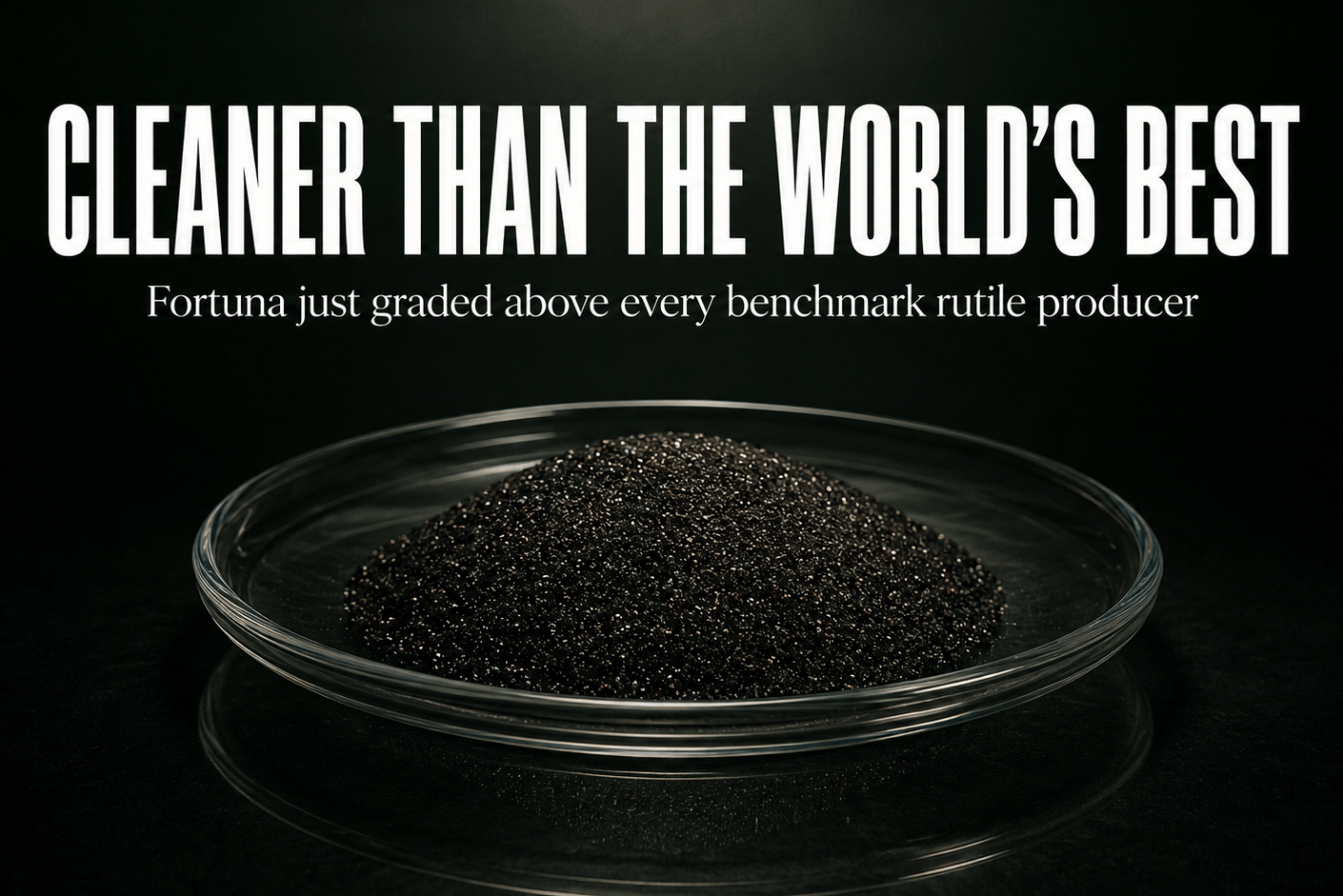

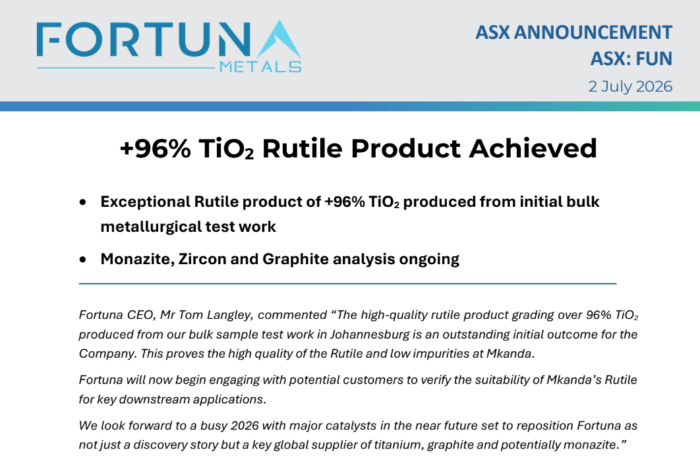

Fortuna Metals (ASX: FUN) has pulled one of the cleanest rutile concentrates in the sector out of a five-and-a-half tonne sample of Malawian dirt, grading 96.66% titanium dioxide.

That is cleaner than the rutile the world’s established producers have been selling for years.

The cleaner it is, the less refining it needs downstream, and the more buyers pay for it.

The market values the whole company at around $27 million, with a maiden resource only weeks away.

Behind that sits roughly $15 million in the bank. A fair chunk of that came from WndrCo, the US tech fund behind SpaceX and Anduril, which is getting upstream of the humanoid wave before it breaks. They paid 11 cents a share to get in.

The stock trades at 9.2 cents today.

Twenty kilometres north, Sovereign Metals (ASX: SVM) sits on the same geology. The market values SVM north of $370 million, more than 13 times Fortuna.

Today’s grade is the first reason to think that gap should close. The resource weeks away is the next.

The Result: 96.66% TiO₂, and What That Buys Fortuna Metals

Rutile is the cleanest natural source of titanium. Buyers pay for the titanium dioxide locked inside it, so a higher TiO₂ reading and lower impurities mean a product that’s worth more and easier to sell.

Sovereign Metals put out a feasibility study on Kasiya, the world-class deposit just up the road, and buried in it is a table of the best rutile on earth. Fortuna’s beats the lot.

The table lines up the rutile the market already runs on. Kasiya specs out at 95.7%. Sierra Rutile, which has been shipping out of Sierra Leone since the sixties, sits at 96.3%. Base Resources’ Kwale mine in Kenya comes in at 96.2%.

Fortuna pulled 5.4 tonnes out of its Mkanda ground, ran it through magnetic and electrostatic separation to strip the heavy minerals from the waste, and the concentrate came back at 96.66%.

Which clears every one of them.

Two of the mentioned have fed the world’s pigment plants and titanium mills for decades, and Fortuna’s bulk sample graded cleaner than both of them the first time it put material through a plant.

Then there’s Toho Titanium, one of Japan’s big sponge producers, which ran the ruler over Kasiya’s rutile and cleared it for aerospace, about as high as the bar goes for titanium feedstock.

Fortuna sits on the same geology and graded above the product that passed.

The Demand Story: Titanium and the Humanoid Build-Out

Titanium is what ties a rutile grade in Malawi to the robots coming off production lines in California, and it explains why a fund that usually chases rockets and tech wrote an $8.6 million cheque for an African explorer.

Titanium is light and strong under load, which is where the humanoid build-out hits a wall, because you can’t build a machine that walks and lifts all day out of anything heavier. And the cleanest source of it is rutile.

The companies building humanoids are already worth billions.

Apptronik, valued at $5.5 billion, has just opened a 90,000 square foot “data factory” in Austin to train its Apollo robots, with Google DeepMind and Mercedes-Benz among the backers.

Figure AI, last marked at around $39 billion, has its Figure 03 robots sorting parts on BMW’s factory floor in the US.

China’s UBTech took $334 million of pre-orders for its U1 companion robot in about four weeks, and Norway’s 1X is getting ready to put humanoids into people’s homes.

Scale these to the numbers the makers keep quoting (Elon’s talking a million a year, and that’s just his first factory) and the world needs far more titanium than it pulls out of the ground today.

And the supply is heading the other way. Natural rutile output has fallen by about a third over five years as the old mines run down, and almost nothing new is due before Kasiya comes online. The US imports nearly all the titanium feedstock it runs on.

So demand is climbing while supply shrinks, and the biggest buyers are hunting for a friendly source outside China.

Which runs straight back to FUN’s concentrate in Malawi grading 96.66%.

What’s Next: Fortuna’s Maiden Resource and Drilling Ahead

The big one lands mid-July: Fortuna’s maiden resource estimate. It’s the first hard number on how much rutile sits in the ground at Mkanda and at what grade.

It’s the first proper measure of whether Mkanda has the scale to sit alongside the tier-one rutile ground up the road. Pulling one together inside 12 months of picking up the project is quick work by anyone’s measure.

A 5,000 metre aircore program then runs through the September quarter, chasing the mineralisation deeper and tightening the grid, with a 30-hole core drilling program behind it later in the year.

Graphite testwork is lined up for the same window, and rare earth and monazite analysis runs alongside it, after Sovereign turned up heavy rare earths at Kasiya in January.

Fortuna’s also got its own lab running in Malawi now, which cuts the cost of testing and gets results back faster. Expect a steady flow of announcements through the rest of 2026 and into 2027.

Fortuna Metals: The Bottom Line

Today’s result answers the quality question.

The rutile grades higher than products already selling into the market, and it’s low on the impurities buyers care about.

The resource estimate answers the size question, and that lands in a few weeks.

At $27 million against Sovereign’s $370 million, Fortuna is still priced as the early-stage punt it was 12 months ago, even with a US tech fund on the register at a premium and a benchmark-beating product in hand.

Exploration never comes with guarantees, and a maiden resource can land differently to what the early work suggests. But Fortuna heads into the back half of 2026 in a much stronger spot than it started the year.

The resource is weeks away, drilling results keep coming behind it, and every one of them feeds a titanium squeeze that gets tighter each time another humanoid maker scales up.

General advice warning, disclosure and confidentiality notice

General advice warning

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consult your own investment advisor to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (“Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 1,554,000 FUN shares at the time of publishing this article. Equities Club has been engaged by FUN at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.