A big week for the portfolio.

Evion Group (ASX: EVG) joined on Tuesday and ripped more than 60% the same day, on the second-busiest trading day in the company’s history.

It’s a sector we’ve never covered before, the company is already generating millions in revenue, and the global market it sits inside runs into the billions.

The rest of the portfolio kept moving . Drills mobilising in NSW, a managing director in London, and a serious manufacturing deal signed in Israel.

Meanwhile, copper is back near record highs. TSMC reckons the global chip market hits US$1.5 trillion by 2030. And Tuesday’s Federal Budget had something real for critical minerals, plus a few CGT proposals worth paying attention to.

Here’s what caught our eye:

- Why EVG ripped after we added it on Tuesday

- AI1’s quiet move toward an actual manufacturing partner

- TSMC’s US$1.5 trillion call and what it means for AI1’s graphene work

- Drills about to turn at Exultant Mining’s Balerion project

- Fortuna takes the rutile story to London

- Copper roars back and the juniors riding it

- What the Federal Budget actually means for small-caps

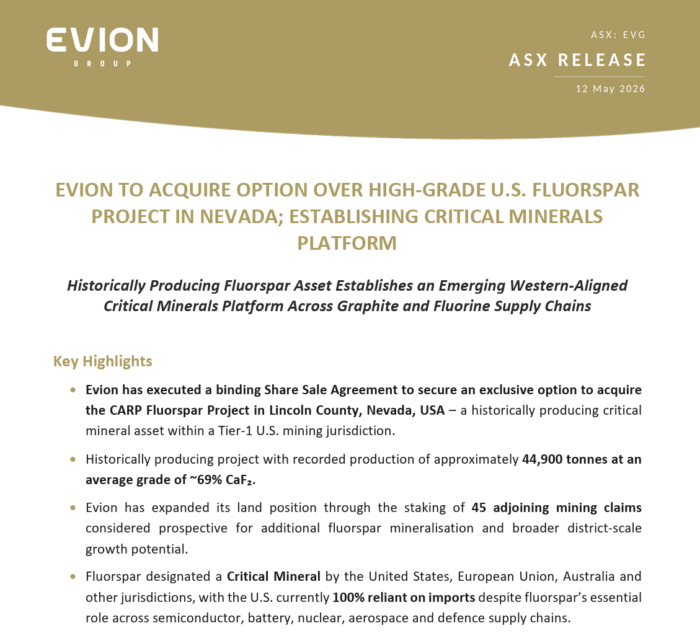

EVG Explodes Higher After Portfolio Addition

Evion Group (ASX: EVG) joined the portfolio Tuesday morning and was up more than 60% by the close, on the second-biggest trading day in the company’s history. It cooled later in the week but still finished up 30%.

The fluorspar story is what pulled us in.

EVG owns the Carp project in Nevada, a historic US producer that delivered around 44,900 tonnes at 69% CaF₂ before it shut. Modern sampling is coming back above that historic average, and the company has expanded its claims around the original workings.

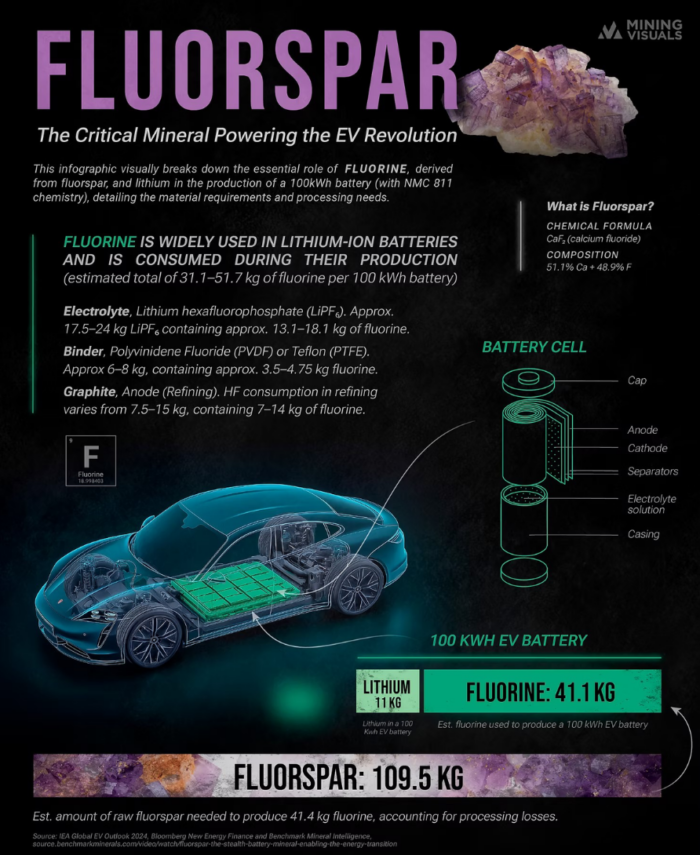

Fluorspar is one of those minerals most investors have never thought about, which is fair enough. It quietly underpins a big chunk of modern industry: hydrofluoric acid, lithium-ion battery electrolytes, semiconductor manufacturing, refrigerants and uranium enrichment all rely on it. China controls global supply. The US imports effectively all of it.

A historic US fluorspar project lands directly in the middle of that scramble for non-China supply.

Then there’s the graphite side.

EVG’s Maniry graphite project in Madagascar is working through permitting, with the technical assessment signed off and the mining permit in the final stretch. Maniry sits under the EU Critical Raw Materials framework, which puts a European customer base genuinely on the table.

The company is also generating cash from its Indian graphite processing operation, with shipments into international markets running right now.

So that’s what we bought. Two critical minerals stories across projects in the US, Madagascar and India, with revenue already on the books.

The share price sits at a mere 4.8c, and the company is valued just over $30 million with about $8 million in cash.

We expect EVG to continue to build momentum in the coming weeks and will be reporting on everything to our subscribers.

Find our full breakdown of why we added EVG to our portfolio here.

AI1 Keeps Building With A Serious Partner

Adisyn (ASX: AI1) signed an MOU on Monday that changes the shape of its drone stealth program.

The partner is Raval A.C.S., one of Israel’s biggest plastics groups. Last year Raval did €201 million in revenue, with an order backlog of €1.243 billion.

Their customer list reads Volkswagen, BMW, Mercedes, GM, Porsche. Five of the toughest customers in manufacturing to win, and harder again to keep, and Raval has all of them.

AI1’s subsidiary 2D Radar Absorbers will co-develop graphene-enhanced injection-moulded parts for radar absorption in drones and UAVs.

Development happens on Raval’s serial production machines from day one. The parts coming out of R&D are already manufacturable, and the path from prototype to qualified volume production running in months rather than years.

The structure points toward a 50:50 joint venture for manufacturing in Israel, with 2D Radar earning a royalty on gross JV revenues for licensing its radar absorption technology. Definitive agreements are targeted within 180 days.

Every new materials story on the ASX runs into the same brick wall when defence customers turn up to look at it. Can you actually make this at scale, in a real factory, to the tolerances we need?

Many of them never answer that question. AI1 just did, by signing up a manufacturer who already builds parts for five of the biggest car companies in the world.

Israel and the US are scaling drone manufacturing capacity aggressively right now, and defence buyers are turning to automotive-grade plastics manufacturers because the volumes and accreditation already match.

And one detail in the fine print matters more than people might catch. The Tel Aviv University licence underpinning 2D Radar is worldwide. Raval’s exclusivity covers Israel and nothing else. The same technology can sit inside a different partnership in Europe, the US, anywhere else AI1 wants to take it. They’ve signed the manufacturer, but not given away the asset.

And two carmakers on Raval’s customer list have also been in the news this week.

Mercedes-Benz’s CEO told the Wall Street Journal on Friday the carmaker is “willing” to move into defence production, saying it could be a “growing niche”.

Volkswagen is in talks to convert one of its German plants from car production to missile-defence manufacturing for an Israeli defence group.

The line between making cars and making defence equipment is thinner than it was a year ago.

AI1 just signed the manufacturer sitting right where that line runs.

Find our full breakdown on their recent announcement here.

What TSMC’s US$1.5 Trillion Call Means for AI1

TSMC believes the global semiconductor market clears US$1.5 trillion by 2030.

When the company manufacturing roughly 90% of the world’s most advanced chips, TSMC, starts talking about where the semiconductor market is heading, investors should probably pay attention.

AI and high-performance computing alone are expected to make up 55% of that.

And the chokepoint inside every next-generation AI chip is the interconnects.

The copper wiring that ties billions of transistors together on a chip is breaking down at modern speeds. It overheats and slows signals as chips shrink and clock speeds climb. The next generation of AI chips can’t get past this on copper alone.

AI1’s atomic-layer-deposition work targets exactly that. They’re growing graphene directly on the wafer to either improve or replace the copper, in a process that fits with how chips are already manufactured.

If even a piece of that lands, AI1 sits inside a market the world’s biggest chip company has just put a US$1.5 trillion price tag on.

There’s a long way from a guaranteed outcome, but the short list of ASX small-caps with that kind of optionality is why it sits in our portfolio.

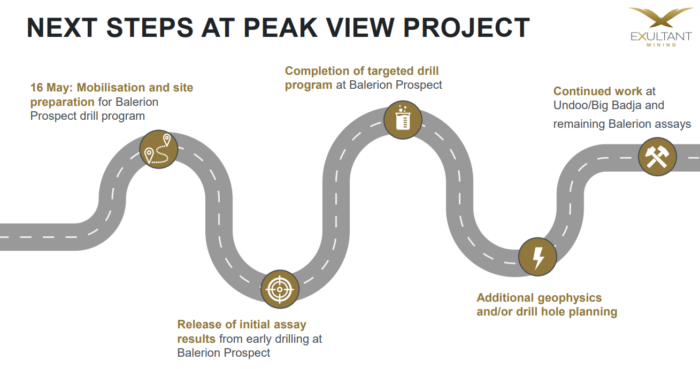

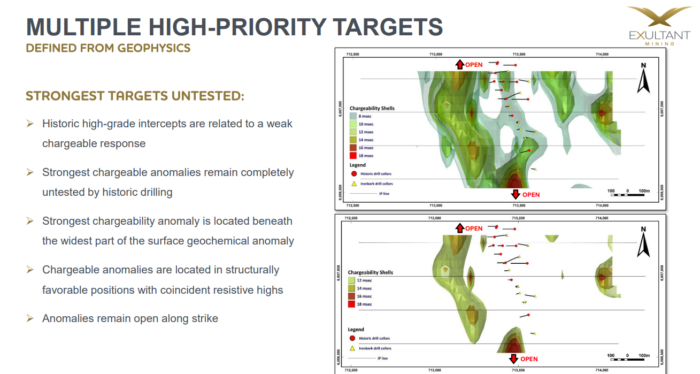

Drills About to Turn at Exultant Mining

The rigs should be spinning this weekend. Always a sentence we love to write.

Exultant Mining (ASX: 10X) put out a fresh corporate presentation this week, with mobilisation and site prep at Balerion already underway. The first hole turns over the weekend.

A formal market announcement is the usual next step, and we’d expect that to land in the coming week once the first hole is underway.

The drill program has been months in the making and these are the moments that make us love the small-cap game.

Chairman Brett Grosvenor spent last week adding to his position through on-market purchases. Directors buying ahead of drilling reads as confidence in what they may find.

10X has around $3.8 million in cash from the March quarter, with an enterprise value sitting closer to $3.5 million. For a company starting a drill program across multiple high-priority targets inside the renowned Lachlan Fold Belt, that’s tiny.

Old workings at Balerion produced intercepts of 4.25% copper, 1270g/t silver, 22% zinc, 11.6% lead and 2.29g/t gold.

Recent geophysics has flagged multiple low-resistivity and chargeability targets sitting next to, and in some cases directly underneath, those historic high-grade intercepts.

The strongest targets were never drilled by previous campaigns.

Whether the rigs find what the geophysics suggests is the open question we’ll soon have an answer to.

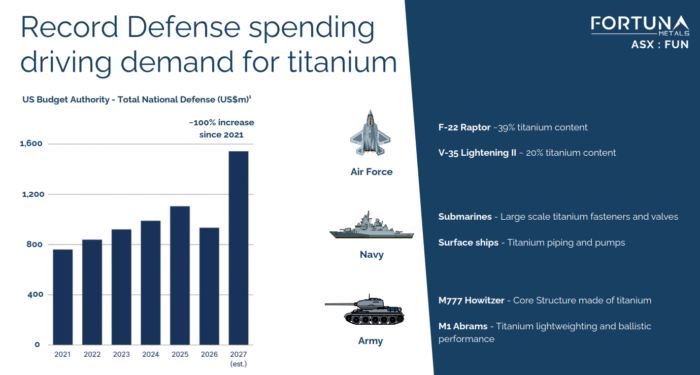

Fortuna Takes the Rutile Story to London

Fortuna Metals (ASX: FUN) flew its rutile story into London this week, with CEO Tom Langley at the 121 Mining Investment Conference with a fresh corporate presentation in hand.

London 121 is one of the bigger meeting points on the mining calendar. Around 75 companies, hundreds of qualified investors, and a format that produces thousands of one-on-one meetings across two days. It’s basically project teams sitting across from the people who allocate capital.

FUN walks in with the Mkanda rutile project in Malawi, sitting roughly 20km south of Sovereign Metals’ Kasiya discovery on the same geology. The updated presentation put an exploration target on Mkanda of 180 to 240 million tonnes at 0.86 to 1.0% rutile from shallow depths.

Rutile is the premium feedstock for titanium production, and titanium demand is firming across aerospace and defence. Humanoid robotics is adding a fresh angle, with Tesla and others now talking about production at scale.

A meaningful chunk of global rutile supply runs through a small number of producers in a small number of countries. Western buyers chasing allied supply have been working through their options for a while now.

A small-cap with a credible rutile story, on the same belt as a Rio-backed discovery, walking into a room full of institutions hunting for exactly that kind of name.

Pitt Street Research dropped a note on Fortuna this week. They’re calling the maiden JORC resource the milestone that converts FUN from explorer to resource-backed junior, with H2 2026 the target.

At A$0.11, they reckon the risk-reward is worth owning into that catalyst.

Pitt Street is reading FUN the same way we have been.

The weeks ahead are worth following.

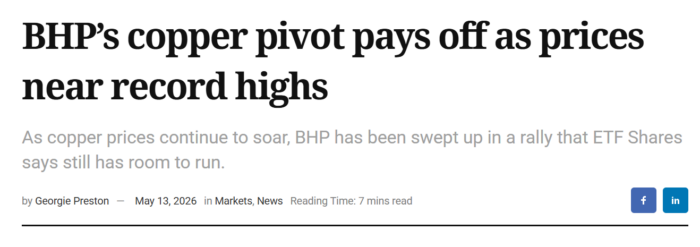

Copper Roars Back as Junior Explorers Circle

Is copper back?

The price climbed roughly 7% this week before closing flat, but now sits up around 11% year-to-date, pushing back toward record territory.

Supply tightness, Chinese demand and the global electrification build are all pulling in the same direction at the same time.

BHP’s copper pivot is starting to look like the right call as the major leans further into copper exposure. The metal also brushed past Middle East volatility this month without flinching, which tells you something about how tight the market reads underlying supply.

The supply story is the engine here. The world needs vast amounts of copper to electrify everything, build out AI data centres, ramp up defence manufacturing and keep grids upright. Meaningful new discoveries keep getting rarer and harder to develop.

When copper moves like this, the market eventually hunts further down the curve. Juniors with real ground and drills already turning sit at the front of that queue, especially the ones already throwing up early results.

What the Federal Budget Actually Means for Small-Caps

Tuesday’s Federal Budget got a fortnight’s worth of takes in 48 hours.

Most of them landed on the proposed CGT change. The 50% discount goes, replaced by cost-base indexation plus a 30% minimum tax on net capital gains, from 1 July 2027 if it passes.

Our take is that capital follows good companies. A multi-bagger is still a multi-bagger, even after the tax bill. The bar to be in one just goes up.

Then there’s the critical minerals piece that caught our eye.

The new Critical Minerals Reserve pulls $1 billion from the existing $5 billion Critical Minerals Facility, with another $150 million set aside for selective stockpiling.

Canberra keeps signalling it wants Australia to do more than dig and ship, and the funding to back it is still flowing.

The companies with real projects and a sensible development pathway will feel it. The ones slapping “critical minerals” onto the PowerPoint will keep getting ignored.

At Equities Club, our approach stays the same. We are active investors, always looking for the best opportunity. We back companies where the project and the people both stack up, after they’ve been through our own filter. Most don’t make it.

Good projects keep finding capital, especially where the world is actively short of new supply. Weak stories get ignored faster than before.

The Week Ahead

The catalysts keep coming this week. The first Balerion results for 10X land in the weeks ahead. AI1 has a six-month clock to firm definitive agreements with Raval. The London 121 meetings tend to surface follow-throughs a couple of weeks later.

A lot of small-cap work is invisible. The site visits, the management calls, the months between deciding a name is worth covering and adding it to the portfolio. The next few weeks are where the visible part lives.

Till next week.

General advice, disclosure and confidentiality

General advice warning

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consult your own investment adviser to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (“Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 1,554,000 FUN shares, 2,083,333 MRD performance rights, 900,000 AI1 performance rights, 200,000 10X shares, 4,500,000 EVG shares at the time of publishing this article. Equities Club has been engaged by FUN, AI1, MRD, 10X and EVG at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.