Two of the biggest spending cycles in a decade are running side by side. Tomorrow morning, we’re adding a company to our portfolio that’s landed in the middle of both.

More on that in the morning.

As for the rest of the week, if you’d only glanced at the ASX 200 you’d have shrugged, put your phone down, and gone about your day. The index barely moved.

Meanwhile a refinery fire knocked out 10% of Australia’s fuel, oil crashed 11% as the Hormuz story flipped twice in 48 hours, gold sat near US$4,800/oz, Eden put on 91% in a fortnight, and Yugo flew 54% on its first drill result.

The index seemed to sleep through the lot.

What caught our eye this week:

- Director buying ahead of drilling at Exultant Mining

- Defence spending piling into drones

- Scandium demand lifting on the back of AI infrastructure rollout

- Gold IPOs keep ripping out of the gate

- A DFS next door to Fortuna Metals reprices the corridor

- Over $5 billion in coordinated Australia-US critical minerals support

- Yugo Metals flies on first drilling hits

- Eden Innovations adds another 31% for a huge two-week run

A New Name Joins the Portfolio Tomorrow

Tomorrow morning we’re introducing a new portfolio addition in a thematic that’s running hot. Without giving the game away, here’s what you’re getting:

- Management team with decades at the top of the industry

- A multibillion-dollar market that’s compounding faster than most people realise

- Commercial revenue within sight

- A valuation with plenty of room to run from here

Full breakdown lands in your inbox before market open tomorrow. If you’re subscribed, keep an eye out. If you’re not, enter your email button below.

Chairman Buying Ahead of Drilling at Peak View

This week, Exultant Mining (ASX: 10X) chairman Brett Grosvenor bought another 100,000 shares on market, adding to an already sizeable holding in 10X.

The rigs are weeks from turning at their Peak View project, targeting a copper-lead-zinc-silver-gold sulphide in New South Wales.

10X has mapped a target corridor using IP and gravity work across multiple 1.6km lines, alongside surface rock chips running up to 50.9 g/t gold over a 360 metre quartz vein trend. (Rock chips are hand-picked surface samples, so they tell you where to look, not what the bulk grade looks like.)

The upcoming program targets the biggest geophysical anomaly on the project, an area earlier drilling campaigns missed.

Directors see the targeting work before anyone else. Grosvenor’s buying right before the first hole goes in tells you he likes what he’s seen.

Peak View is about to get its first proper test.

Drone Funding Catches up to the Talk

Last week we said we liked the drone space. The funding numbers this week did the rest of the talking.

Australia this week flagged up to $5 billion of new spending on uncrewed systems, funnelled into programs with names that sound like rejected Tom Clancy titles.

Ghost Bat is a combat drone that flies alongside crewed fighters. Ghost Shark is an autonomous submarine that just entered service with the Navy this month.

The Integrated Investment Program is now spending $12 to $15 billion on kit like this through to 2036.

Three years of Ukraine has taught every defence ministry the same lesson. A $500 drone can take out a $10 million tank, and the budgets are starting to reflect it.

The US, as it tends to, is going magnitudes larger on defence spend, with policy proposals pointing towards a US$1.5 trillion defence budget in 2027 and loitering and kamikaze drones near the top of the shopping list.

China’s also spending hard on the same tech.

The contracts are starting to flow, and there are two ways small-caps get their cut. The ones making the parts that go inside these things, and the ones digging up the metals that go inside the parts.

The Scandium Sweet Spot

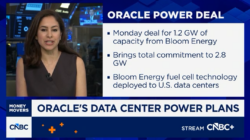

Scandium used to be a specialist alloy story. This week it walked straight into the AI data centre trade.

Oracle just signed a master services agreement with Bloom Energy covering up to 2.8GW of solid oxide fuel cell (SOFC) systems. It’s the biggest single SOFC deal ever done.

SOFCs make electricity through an electrochemical reaction instead of burning fuel, and they rely on scandium-stabilised zirconia to work efficiently and last longer.

SOFCs already soak up around 47% of global scandium demand. A 2.8GW contract puts real numbers behind a market that had mostly lived in forecasts.

Bloom has deployed 1.2GW to 1.4GW globally to date, and entire national SOFC fleets usually sit in the hundreds of megawatts to low single-digit gigawatts. A 2.8GW order from a single customer is a big step up from anything the market has seen.

Sunrise Energy Metals (ASX: SRL), the most advanced large-scale scandium exposure outside China and Russia, has already run roughly 50% over the past month as the story flows into the share price. It’s now valued at roughly A$1.85 billion.

Which brings us to our portfolio company Mount Ridley Mines (ASX: MRD).

MRD has scandium sitting alongside rare earth mineralisation across 367.98Mt at Grass Patch, and there are no large-scale primary Western scandium producers.

A big volume of pulps is still to be re-assayed for scandium, with clear scope to expand the resource footprint. At a $45 million market cap, we still think the scandium exposure inside MRD is getting overlooked.

Gold IPOs Running Hot

Gold juniors are having a moment on the ASX. Three new listings in a few months have all rewarded the people who got in early, and the latest one ran harder than anything before it.

With the war in Iran cooling, the market is pivoting back towards gold, and the price closed the week stronger.

Here’s who’s been running, and who we think lists next.

Bison Resources (ASX: BSR) listed this week at 20c, ran as high as 95c, and closed the week at 57c. A 185% premium to issue price after five trading days.

The move followed a heavily oversubscribed $5.5m raise to fund its Nevada projects along the Carlin Trend, one of the world’s most prolific gold belts.

Black Horse Mining (ASX: BHL) listed in December and peaked at 220% above its 20c IPO price. They’re drilling a historic Victorian gold mine that produced more than a million ounces before water forced it shut.

Valiant Gold (ASX: VAL) is the other one, holding well above listing after peaking at a 70% premium.

When gold is this strong for this long, investors are paying up for any IPO with clear geology and a credible path to proving it out.

Which naturally leads to the next question: who’s next?

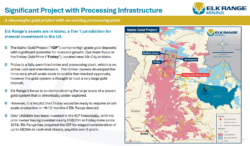

Elk Range Mining earned a mention in our top stockbroker picks for 2026, and we think for good reason.

Elk comes to market with a permitted underground mine sitting on defined historical ounces, with processing infrastructure already in place. That’s a meaningful headstart over your average early-stage listing.

With gold holding near US$4,800/oz, Elk shapes up as the next gold float to keep an eye on.

The DFS Next Door to Fortuna Metals

Sovereign Metals (ASX: SVM) dropped its Definitive Feasibility Study (DFS) for Kasiya this week. The numbers make it pretty clear how valuable the rutile and graphite corridor in Malawi really is.

The headline figure was a pre-tax Net Present Value (NPV) of US$2.2 billion. SVM’s current market cap is around A$470 million.

A DFS is the study that tells you whether a project actually makes money, and NPV is the headline figure, the present-day value of all future cash flows once time and risk are accounted for.

It’s one of the cleanest ways to size up a project’s economic strength.

SVM closed the week up just under 6%. That one week’s gain in market cap is worth more than the entire market cap of Fortuna Metals (ASX: FUN), which sits around A$25 million.

FUN sits along the same geological trend as SVM, just south of Kasiya. SVM is now putting study-backed numbers against a multi-billion-dollar project, which validates the corridor itself at a valuation level.

We’ve been backing FUN as leverage into this region since we added it to the portfolio. Proven geology, now proven economics, and still trading at a fraction of what’s sitting further down the belt.

Policy Support Keeps Building

More than $5 billion in coordinated export credit support is now being pointed at new critical minerals projects across Australia and the US.

Export Finance Australia and the US Export-Import Bank issued aligned letters of support across nickel, cobalt, rare earths and gallium supply chains.

For anyone not across it, letters of support are the step before financing, signalling to developers and investors that the money will be there once projects clear their milestones.

That’s governments moving from strategy documents to project financing. It’s the step that usually moves a project from study to build.

For years, Western critical minerals projects have been stuck waiting for someone to underwrite the risk. China already underwrites its own.

Having two allied governments do the same in parallel is a different setup than the one small-cap developers have been working inside.

For small-caps like MRD with heavy rare earths and scandium exposure, the policy direction keeps getting clearer. Allied governments are backing domestic and partner supply chains directly, and that’s a better macro setup for emerging projects than anything we’ve had before.

Yugo Flies on First Drilling Update

Yugo Metals (ASX: YUG) ripped 54% this week to a roughly $34 million market cap after its first drilling update from the Erak Prospect at the Sinjakovo Project in Bosnia.

Early scout drilling hit shallow breccia-hosted mineralisation across gold, silver, copper and antimony, with a 7.1 metre zone from just 26.2 metres depth. The structure remains open along strike and at depth, and assays are due shortly.

Surface support was already there before the rigs turned. Historical trenching returned 61 metres at 1.5 g/t gold, and rock chips went as high as 7.9 g/t gold and 2,070 g/t silver.

Adriatic Metals is the reference point in this part of the world. They scaled a breccia-hosted system in Bosnia into a takeover at around US$1.25 billion.

Yugo is a long way behind that, but first-pass drilling confirming a live polymetallic system in the same belt is how those stories usually start.

The Strait of Hormuz: 48 Hours of Whiplash

Every paragraph of this section has a shelf life of about six hours right now, but we’ll do our best to wade briefly into the fog of war.

Overnight Friday was the wild one. Iran’s foreign minister declared the Strait of Hormuz “completely open” for the first time since the war started, oil crashed more than 11% in its biggest single-day move of the conflict, and the S&P 500 and Nasdaq both closed at record highs. For a few hours, it looked like the war premium was gone.

That already appears to be falling apart. Iran’s military said the strait had “returned to its previous state,” the IRGC opened fire on commercial tankers, and warned that approaching the strait would be treated as “cooperation with the enemy.”

A second round of US-Iran talks is now scheduled for tomorrow in Pakistan. The ceasefire itself runs out mid-week.

Friday was the market pricing peace. Saturday was the reminder that war is messy.

Gold gave back some ground on Friday, while oil juniors went the other way. Both those trades could flip in a heartbeat if the peace talks go sideways.

Eden Keeps Running

Last week we flagged Eden Innovations (ASX: EDE) after a 45% move. This week the stock added another 31%, taking the two-week gain to roughly 91%.

The latest announcement gives you the why. Eden launched its new EdenShield division targeting defence and national security applications, with products including hardened concrete and electromagnetic shielding materials.

Hardened concrete does what it sounds like. Stronger, more blast-resistant building material, useful for anything important from embassies to data centres.

Electromagnetic shielding protects sensitive electronics from interference, whether that’s electronic warfare or the guy next door running a big magnet.

Governments are writing bigger cheques for the infrastructure that houses all of this, and retrofits tend to land faster than full rebuilds.

This is why selective exposure to emerging small caps still matters. When a company sits in a sector with structural demand and starts moving from trials into commercial rollout, the market responds fast.

Eden’s two-week run is a reminder that the biggest percentage moves often come from smaller names sitting in the right theme at the right time.

What’s Next

The themes are all pointing the same way right now.

Defence budgets are turning into contracts, AI infrastructure is showing up in metals demand, critical minerals policy is moving from press release to cheque book, and gold sitting at records is keeping the exploration and IPO pipeline wide open.

With Iran (possibly) winding down it’s as good a backdrop for small-caps as we’ve had in a while, and several names we covered this week have drills turning or results pending over the coming weeks.

Tomorrow morning, we’re adding one more to the portfolio.

If you want to be first in line, hit the subscribe button below.

Till next week.

General advice warning, disclosure and confidentiality notice

General advice warning

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consulting your own investment advisor to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (“Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 1,554,000 FUN shares, 2,083,333 MRD performance rights, and 200,000 10x shares, and 187,500 BHL shares at the time of publishing this article. Equities Club has been engaged by FUN, 10X and MRD at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.