There was a bit of envy this week watching Karl declare himself free of the small screen and click his heels together like he was off to star in a musical.

I guess ending 26 years of 4am alarms will do that to a man.

No such luck for us. Our screen, the one that trades, had us hooked all week as usual, and it served up a gold price getting pushed around. Bullion tested US$4,000, dipped under for a moment, then clawed back above it to close out a fourth week in the red.

But no need to panic. Gold’s still up better than 23% on a year ago and the banks haven’t backed off their higher targets (more on that later).

Plenty was still happening down the cheap end. Here’s what caught our eye this week:

- Mount Ridley grows its scandium resource off old samples

- Azzuro wraps its first drilling phase at Red Hill, assays due in July

- Gold wobbles toward US$4,000 but the bull case holds

- Pathkey bolts on an AI chip-design play after buying Chipforge

- Orcoda jumps 179% on a contract win against a falling market

- China hands out a lithium permit and the sector drops

Mount Ridley (MRD) Grows Its Scandium Resource Again

Mount Ridley (ASX: MRD) keeps turning up scandium every time it digs back through its old drill samples.

MRD owns one of the biggest scandium deposits reported anywhere, around 367 million tonnes of it, on its Grass Patch ground near Esperance, with rare earth and gallium in the same ground.

This week it re-assayed another 481 old samples, and the deposit grew in all directions. The standout ran 22 metres at 134 ppm from 33 metres deep, about 46% above the existing resource average of 92 ppm. Other hits came in at 119 ppm and 104 ppm, and a number of holes still had scandium in them where the old drilling stopped.

MRD is doing this off pulps that have sat in the shed for years, with roughly 14,000 still to get through. It’s about the cheapest way to add tonnes there is.

Scandium is a critical mineral almost no one produces outside China and Russia. China put it under export licensing last year and choked the trickle reaching the West, which is why Australia, the US and Europe all want their own supply. It goes into aerospace alloys, fuel cells and 3D printing.

Demand for the metal is tipped to grow around 14.5% a year out to 2031 as those uses scale up. A deposit this size on Australian ground is what will turn the heads of Western buyers.

From here the new numbers feed into an updated resource estimate that could lift the JORC number. A second batch of re-assays is already back and under review, and the company is scoping a follow-up program to test a 13km stretch of untested ground to the south-west.

All of it funded off material MRD already owns.

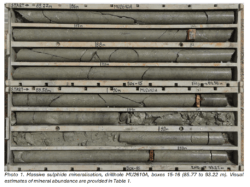

Azzuro (AZ9) Keeps Hitting Sulphide at Red Hill

Azzuro Resources (ASX: AZ9), or Asian Battery Metals as most of you know it, has spent the past two months putting holes into Red Hill, its copper-gold project in Mongolia, and pulling up sulphide most of the way down.

Phase one wrapped this week, 15 holes for close to 1,900 metres.

The best hole cut nearly 37 metres of massive sulphide, then deeper down clipped a two-metre vein logged at a visual 33% chalcopyrite.

Five of the six holes chasing the sulphide found it, and the system now runs about 272 metres along strike, still opening up at both ends and at depth. They’ve been chipping at this thing since last year and every phase makes it look bigger.

Quick caveat on those grades. They’re the geologists’ eyeball read off the core, and the lab can tell a different story once it weighs in. Visual chalcopyrite has flattered to deceive before, so treat the percentages as a strong hint rather than a banked result until the assays land.

Azzuro’s still a minnow, trading at 1.7c for a market cap near $14 million. It went into the program with $5.2 million in the bank and we’d put it near $4 million now, so there’s cash to keep the rig turning. Which it will, having already moved across to the nearby Copper Ridge target.

A company this size landing thick sulphide while the world can’t get its hands on enough copper can re-rate in a hurry, if the assays back the visuals.

Most of those assays are due in July, with downhole electromagnetic surveys (which pick up conductive sulphide still sitting in the ground) starting shortly.

Gold Price Holds Above US$4,000 as Banks Stay Bullish

Six months ago you couldn’t get through a barbecue without someone telling you gold was headed for US$10,000. It’s come off the boil a bit lately, back to around US$4,071, and funnily enough that same crowd has gone quiet.

Gold is still up more than 23% on this time last year. Most people fondly remember the record it set in January, so a few months underneath it feels like a collapse when the price has really just had a rest.

We like gold more now that some people have lost interest.

The banks have all trimmed their forecasts since the slide, and every trimmed forecast still sits above where gold trades today.

- Goldman Sachs: US$4,900/oz by year end

- BMO Capital Markets: an average around US$4,625/oz across the second half

- Deutsche Bank: US$4,300/oz in the September quarter, lifting to US$4,800/oz by December

Goldman just cut its forecast and still landed about 20% above where gold sits now.

Central banks have been buying hand over fist for months (China’s been adding to its pile 18 months straight), and they don’t lose sleep over what the price does in any given week. That’s the floor under all of this.

Sentiment in gold can flip in a hurry though, and the last few months are proof of that.

There are plenty of gold names that ran hard on the way up and now trade at valuations that leave no room for a wobble. The ones worth owning are quality operators still trading at a fair price, and they’re out there if you put in the work.

We’ve got our eye on a couple. More in the coming weeks.

Pathkey (PKY) Buys Chipforge in an AI Chip-Design Bet

We flagged Pathkey (ASX: PKY) on 3 May as one to keep an eye on, back when it was sitting at 5c. It closed this week at 7.1c, up more than 40%, and we think it’s only just booting up.

This week PKY completed its buyout of Chipforge, a Singapore outfit building an AI platform that designs custom computer chips.

Designing custom silicon today takes 12 to 24 months and at least US$5 million a design, and most attempts fail on the first try, with an 86% first-silicon fail rate.

Chipforge’s pitch is that its agentic AI does the heavy lifting between design and verification, cutting that timeline by up to 70%.

Cadence and Synopsys, the two US giants that own chip-design software, are worth around US$190 billion between them and still run on tooling built in the 1980s.

Governments have committed more than US$115 billion to building out their own chip capacity since 2022, and the world is tipped to be short a million chip engineers by 2030. (Finally, a job the robots are creating instead of stealing.)

Chipforge holds an exclusive worldwide licence to chip-design IP from Nanyang Technological University, ranked the number one AI research institution globally.

PKY’s pre-revenue and tiny, so plenty can still go wrong. But it’s pointed straight at the silicon shortage the whole world is throwing money at, and it’s already handed readers 40% since we first flagged it.

Orcoda (ODA) Jumps 179% on a Wagner Contract Win

The biggest small-cap move of the week came from an unlikely spot, a Brisbane logistics and software business. Orcoda (ASX: ODA) jumped 179% on a new contract.

The deal is with the Wagner Corporation, the Toowoomba clan who built an entire airport on farmland outside town. Orcoda’s now running the workforce logistics and facilities management at Wellcamp Business Park, the industrial estate that’s grown up next to that airport.

It kicks off in July, worth about $8 million a year, billed monthly on the number of workers housed on site.

Orcoda turned over about $17 million last financial year, so a single deal adding half that again is a proper step up, and it lands just as the company was nursing a hole left by a major customer who deferred work back in FY25.

The contract runs on Contractor360, Orcoda’s workforce platform, lately rebuilt as an AI-led system that handles onboarding, rostering, accommodation and site access. Plenty of mining and construction outfits run big crews on remote sites and need similar, so Wellcamp doubles as a shop window for potential customers.

More often than not, the week’s small-cap winners are explorers riding a fresh drill hit. Orcoda got there on a signed contract and recurring revenue, which is a sturdier reason to be up 179%.

China’s Lithium Permit Knocks the Sector Again

A single permit notice out of China knocked the lithium market this week, and the ASX lithium names wore it with everyone else.

The trigger was CATL’s Jianxiawo mine in Jiangxi, one of the biggest hard-rock lithium deposits going. Around 65,000 tonnes of lithium carbonate a year comes out of it, roughly 3% of global supply, and it’s sat idle since August last year when its permit lapsed.

That shutdown alone was enough to more than double Chinese lithium futures at one point.

Then this week Jiangxi authorities handed a CATL subsidiary a fresh land-use approval. That’s an early tick in a long process, but traders jumped on it as the clearest sign yet the mine is coming back, and Chinese lithium carbonate futures fell about 10% over two sessions to a 10-week low.

Pilbara Minerals (ASX: PLS), Liontown (ASX: LTR) and Mineral Resources (ASX: MIN) all price off that Chinese carbonate number, so the drop washed straight onto our market within the day.

Small explorers feel it more than anyone, because they fund their drilling by raising money, and the price they can raise at tracks the lithium price. Knock 10% off in Jiangxi and a junior in Perth has to hand over more shares to bring in the same cash.

The small caps swing harder than the producers both ways, so weeks like this sting the rebounds fly.

There’s still no telling when the mine actually fires back up, and most analysts see lithium supply staying tight as battery demand climbs.

What it lays bare is how much of lithium’s recovery leans on this one mine staying dark, and how completely Beijing still works the switch, the same lever we’ve watched it pull on gallium, scandium and rare earths.

The Week Ahead for ASX Small-Caps

We’re glad to see the back of June. It’s been a rough month for small-caps, caught between the usual end-of-financial-year selling and the lingering hangover from the May budget and all the noise around tax.

The good news is news flow tends to pick up from mid-to-late July, so our portfolio companies should start dropping announcements, and the ASX should find a pulse again.

Gold looked to settle by Friday, copper held firm, and lithium wore the brunt of a mine that might be coming back to life.

And keep half an eye on the defence names, because the US and Iran are circling each other again, which has a way of putting a bid under that corner of the market.

Till next week.

General advice, disclosure and confidentiality

General advice warning

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consult your own investment adviser to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (“Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 2,083,333 EVG shares, and 1,150,000 AZ9 shares at the time of publishing this article. Equities Club has been engaged by MRD and AZ9 at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.