We parked outside the Perth Mint just before open on Thursday. There was already a crowd waiting at the gates, and by the time they opened the line snaked out the door. The staff barely looked up.

At these gold prices, that’s just what a Thursday morning looks like.

Gold is above US$5,200/oz. J.P. Morgan just put US$6,300 on it by year end. Central banks are hoarding bullion at record pace. And everyday punters are queuing at the Mint on a rainy weekday to get their hands on it.

You can read all the forecasts you like, but a line out the door at 9am tells you something a price chart can’t.

All of that was before bombs started falling on Tehran on Saturday afternoon, likely killing the Supreme Leader, grinding the Strait of Hormuz to a halt and dragging half the Gulf into the firing line.

We covered what escalation could mean for oil and gold in last week’s wrap. Expect both to move sharply when markets open Monday.

The ASX 200 pushed to fresh all-time highs during the week in the middle of earnings season, and the smaller end of town was just as busy.

What caught our eye this week:

- Bombs fall on Iran, Gulf shipping thrown into chaos

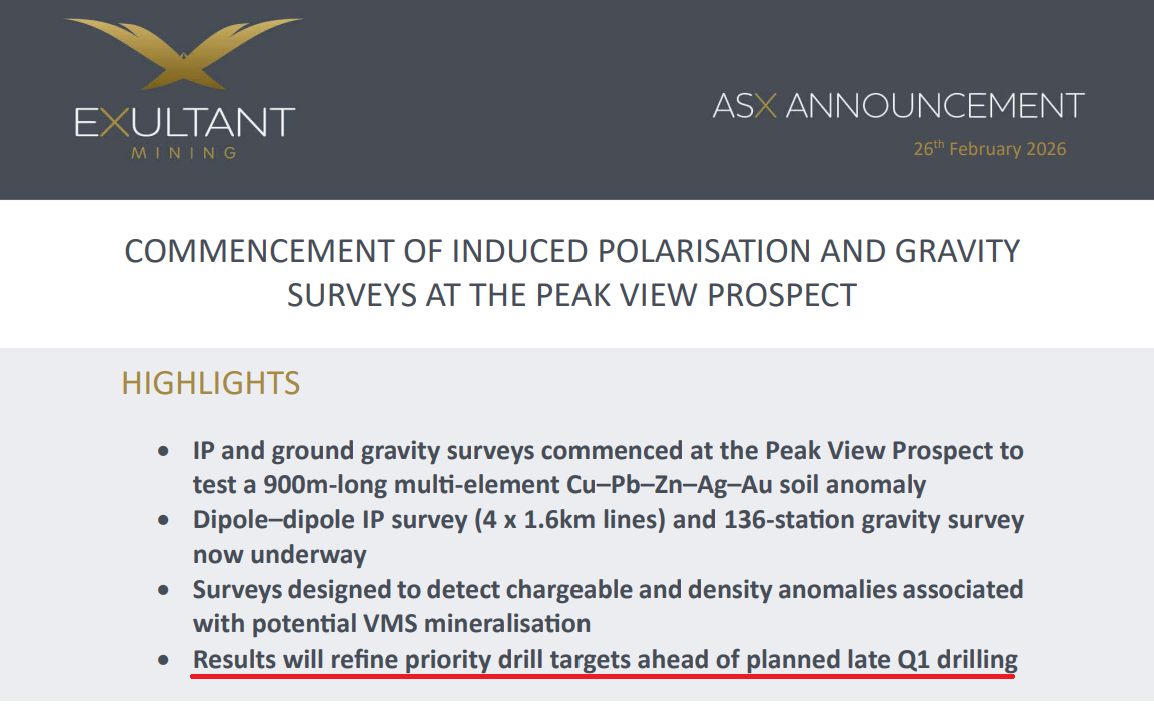

- 10X gets geophysics underway at Peak View ahead of late Q1 drilling

- FUN sends off a bulk met program, marking a shift toward development

- The Broker Black Book dropped with thirteen high-conviction broker picks

- Zimbabwe’s lithium export ban sparked a sharp price rebound on the ASX

- J.P. Morgan lifts its 2026 gold price target to US$6,300/oz

- Only one Australian company sits in the global top 10 gold producers

- BHP reclaimed the top spot on the ASX as CBA comes under scrutiny

- Could glaciers stop US$40 billion of copper investment in Argentina?

- FMR surged after pulling mineralised core, with assays pending

What Iran Strikes Mean for Gold, Oil and Monday’s ASX Open

Things are moving fast in Iran. Talks in Geneva fell apart on Thursday, Trump said on Friday he was ‘not happy’ and that ‘sometimes you have to’ use force. By Saturday, bombs were falling across Iran.

Last June’s strikes on Iran were limited to nuclear sites, and markets shrugged them off within days. This is nothing like last June.

This time, Trump says they killed the Ayatollah, and told the Iranian people to overthrow their government once the bombing stops. We expect a very different reaction when markets open on Monday.

Iran has responded with missiles fired at Israel and US bases in Qatar, Kuwait, Bahrain and the UAE. The Gulf states that house those bases sit on top of the world’s oil shipping lanes. Shipping through the Strait of Hormuz has all but stopped. Oil closed Friday near US$73. It won’t open there on Monday.

Iran produces around 3 million barrels of oil a day, most of it moved through a shadow fleet of tankers doing ship-to-ship transfers to dodge sanctions. Iranian crude was already selling at a discount just to keep buyers. If that supply is now offline, buyers (mostly China) will have to scramble for replacement barrels at full price.

In the early fog of war, we’re not going to pretend we know how this plays out. What we do know is that conflict in the Middle East has historically been very good for gold and oil, and very bad for certainty.

If you hold commodity exposure heading into Monday, prepare for a bumpy ride.

Exultant Mining (10X): Geophysics Underway at Peak View Ahead of Drilling

Our portfolio company Exultant Mining (ASX: 10X) hasn’t slowed down since we added them to the portfolio a few weeks ago. For anyone who missed it, the full write-up is here (and one of our most read).

10X is a gold, silver and copper explorer with projects across NSW and Western Australia, sitting on high-grade historical hits that nobody has gone back to test with modern gear. At a $7 million market cap, we think that’s too cheap.

Their lead project Peak View, in the East Lachlan Fold Belt in NSW, now has IP and gravity surveys underway targeting the 900-metre copper-lead-zinc-silver-gold soil anomaly with drilling in the coming weeks.

Four 1.6km IP lines and 136 gravity stations are covering the full anomaly footprint, looking for targets that could point to VMS-style massive sulphide mineralisation.

Most of this volcanic horizon has never had modern geophysics run across it. The data coming back will be a genuine first look at what’s sitting underneath.

10X put out a video interview with their senior geologist Sebastian Hind recently that’s worth a watch.

The bit that caught our ear was the comparison to Captain’s Flat, a historically high-grade VMS deposit in the same district. The ore bodies there had a combined strike length of around 500 metres, with mineralisation running 800 to 1,000 metres at depth.

The soil anomaly at Peak View already stretches 900 metres at surface, with a second silver-gold anomaly over a kilometre to the south that may be connected.

Whether what they’re seeing at surface reflects something that thickens at depth is exactly what the geophysics and drilling are designed to answer.

No results yet, but soil results came out on 11 February, geophysical crews are on the ground, and rock chip assays are expected in the next week or two. Newsflow is stacking up heading into the late Q1 drill program.

At a $7 million market cap with gold above US$5,200/oz (and possibly going higher come Monday), the setup remains cheap for what they’re chasing.

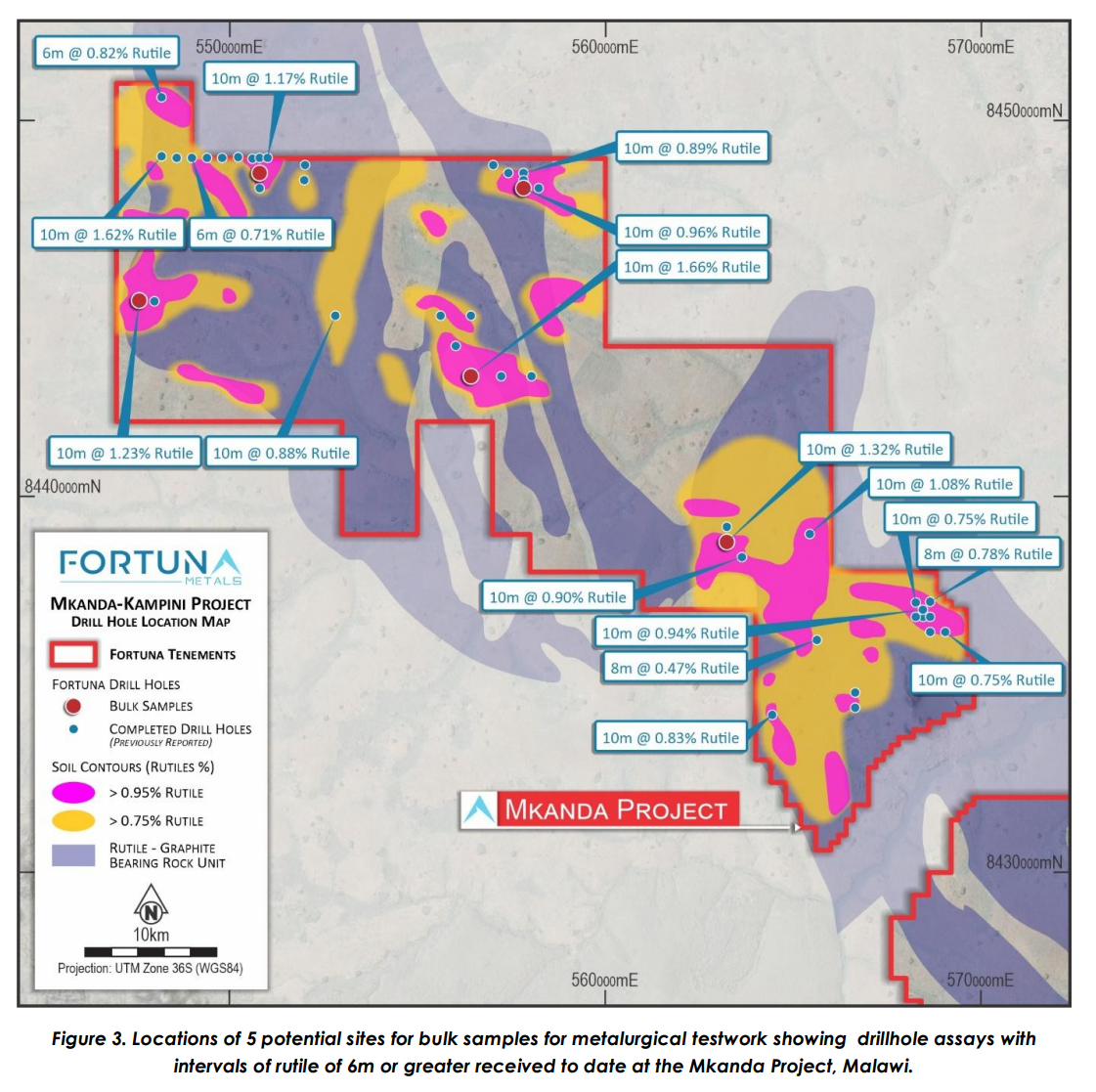

Fortuna Metals Kicks Off Bulk Met Testing at Mkanda

Another of our portfolio companies, Fortuna Metals (ASX: FUN), kicked off a 5-tonne bulk metallurgical program targeting a >95% rutile concentrate at their rutile project in Malawi.

FUN is exploring what could be a large-scale rutile system along the same geological corridor as Sovereign Metals’ Kasiya deposit, the biggest rutile find globally.

Mineral Technologies in Johannesburg is running the test work, with results expected by June 2026. This is the first real sign FUN is thinking beyond exploration and toward what a mine might actually look like.

The concentrates will be sent to companies in the titanium sponge market, the high-value end of the rutile chain that feeds into aerospace and advanced manufacturing. That’s where the serious money sits, and potential funding.

On the ground, 675 shallow drill holes are done, with 534 assays still pending. Those results will help map the scale of the ~25km² high-grade anomalies and guide priority resource drilling.

Bulk sample results, Q1-Q2 assays and Aircore drilling from May all feed into a potential maiden inferred resource in H2 2026. The team is building toward a Kasiya-style development pathway, and so far the work is backing it up.

Sovereign Metals (ASX: SVM), which sits on the same geological corridor in Malawi, rose over 14% this week. SVM trades at 86.5c with a market cap above $600 million. FUN trades at 8.4c and is worth $24 million. Same corridor, same mineralisation style, very different price tags.

We believe FUN gives you exposure to proven ground at a fraction of the cost, and the market seems to be slowly catching on.

The Broker Black Book: Top ASX Stock Picks for 2026

We released The Broker Black Book earlier this week. Instead of writing about our own picks, we picked up the phone and asked the people who structure deals, allocate capital and see placements before they go public one question: what’s your highest-conviction pick for the year ahead?

What came back was an interesting mix of where professional money is leaning.

Copper names with scale in good jurisdictions. Gold stories with real production pathways forming. Explorers going after large systems. And a handful of left-field ideas that you won’t find in the usual small-cap echo chamber.

Thirteen picks in total, spanning resources, biotech and emerging tech, each laid out with valuation context, key assets and the broker’s reasoning in their own words.

If you want to know where experienced operators are putting money as we move through 2026, it’s a good place to start.

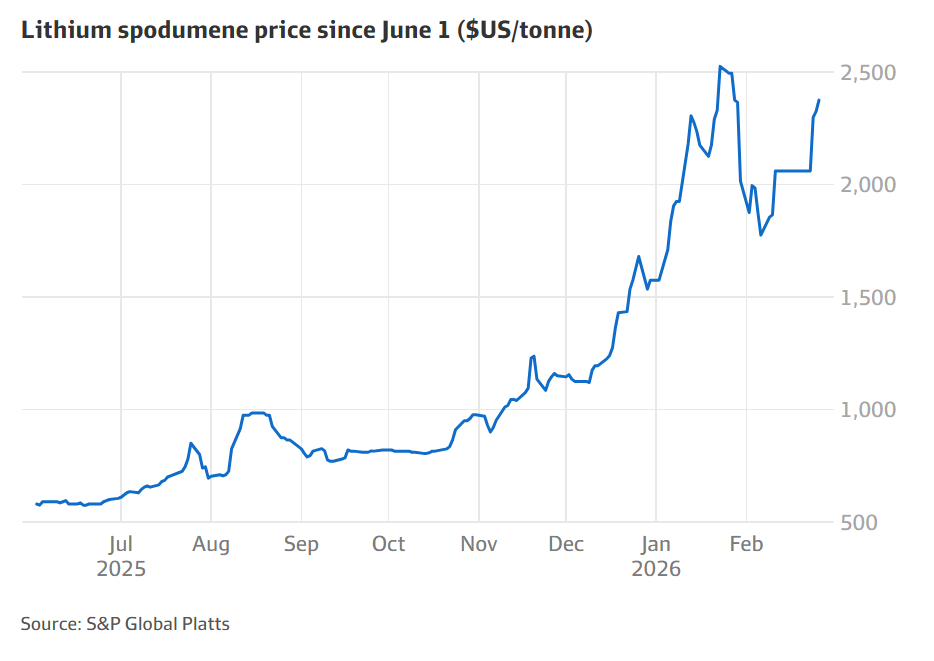

Zimbabwe Bans Lithium Exports and ASX Lithium Stocks Rally

Lithium was back in the headlines this week, and for once it was good news.

Zimbabwe, which accounted for roughly 10% of global lithium output last year, suspended exports of lithium concentrate to force more domestic processing. The reaction on the ASX was immediate and aggressive.

Spot spodumene prices jumped more than 2% in a single session and finished the week up over 15%. PLS (ASX: PLS) led the charge, surging 26% as shorts got squeezed and investors recalibrated near-term supply risk.

China’s refiners are reportedly stocked only through mid-April, and with shipments taking months to arrive, any delay in Zimbabwean tonnes tightens the window further.

We’d been waiting for something to jolt this market. Higher prices could accelerate restarts across Australia and put a floor under beaten-down developers.

This comes with caution though as these things have a habit of being walked back, and the next few months hinge entirely on whether the ban holds and supply can respond fast enough to cap the rally.

J.P. Morgan Gold Price Forecast: US$6,300/oz by End of 2026

J.P. Morgan forecast this week that gold could rise 22% from current levels to reach US$6,300 by the end of 2026. With the gold price at US$5,200/oz now, a target from the world’s biggest investment bank 20% higher certainly helps gold sentiment.

They’re pointing to strong investor demand and central bank buying that’s been running well above recent averages through 2025. J.P. Morgan reckons that momentum carries into next year, and with mine supply as slow to respond as ever, it doesn’t take much extra demand to move the gold price when there’s nothing on the supply side to absorb it.

For ASX gold miners, developers and juniors, US$6,300/oz changes project economics by a fair whack. Projects that looked marginal twelve months ago suddenly have real wiggle room, and those already producing just got a bigger margin on every ounce they pour.

Exploration gets funded as projects look more attractive, and when capital starts looking for leverage to the gold price, small caps are where it ends up. We’ve seen that playbook run before.

We’re backing our small-cap gold plays in Black Horse Mining (ASX: BHL) who are expecting gold drill results shortly, along with 10X, who will be drilling in the coming weeks.

Druckenmiller Goes Long Copper and Gold

Stanley Druckenmiller sat down with Morgan Stanley this week for an interview that’s well worth a watch. For anyone who doesn’t know the name, Druckenmiller is regarded as one of the best macro investors alive, with roughly 30% annualised returns over nearly 30 years and never a losing year.

His portfolio has been heavy in AI for the past three years, but that’s not the case anymore. He’s now long copper, long gold, short bonds, and bearish on the US dollar.

On copper, he says there’s no meaningful new supply coming online for roughly eight years, and demand from AI and data centres is only adding to the squeeze. He called it a consensus trade, but that doesn’t bother him. As he put it, “I don’t care if a trade is crowded, if I think the thesis is right and the trend is with me.”

On gold, he described it as ‘mainly a geopolitical trade.’ Given what’s unfolding in Iran, that reads pretty well.

Copper and gold are two commodities we’ve been banging on about for quite some time, and one of the best track records in history is sitting on the same side of the trade.

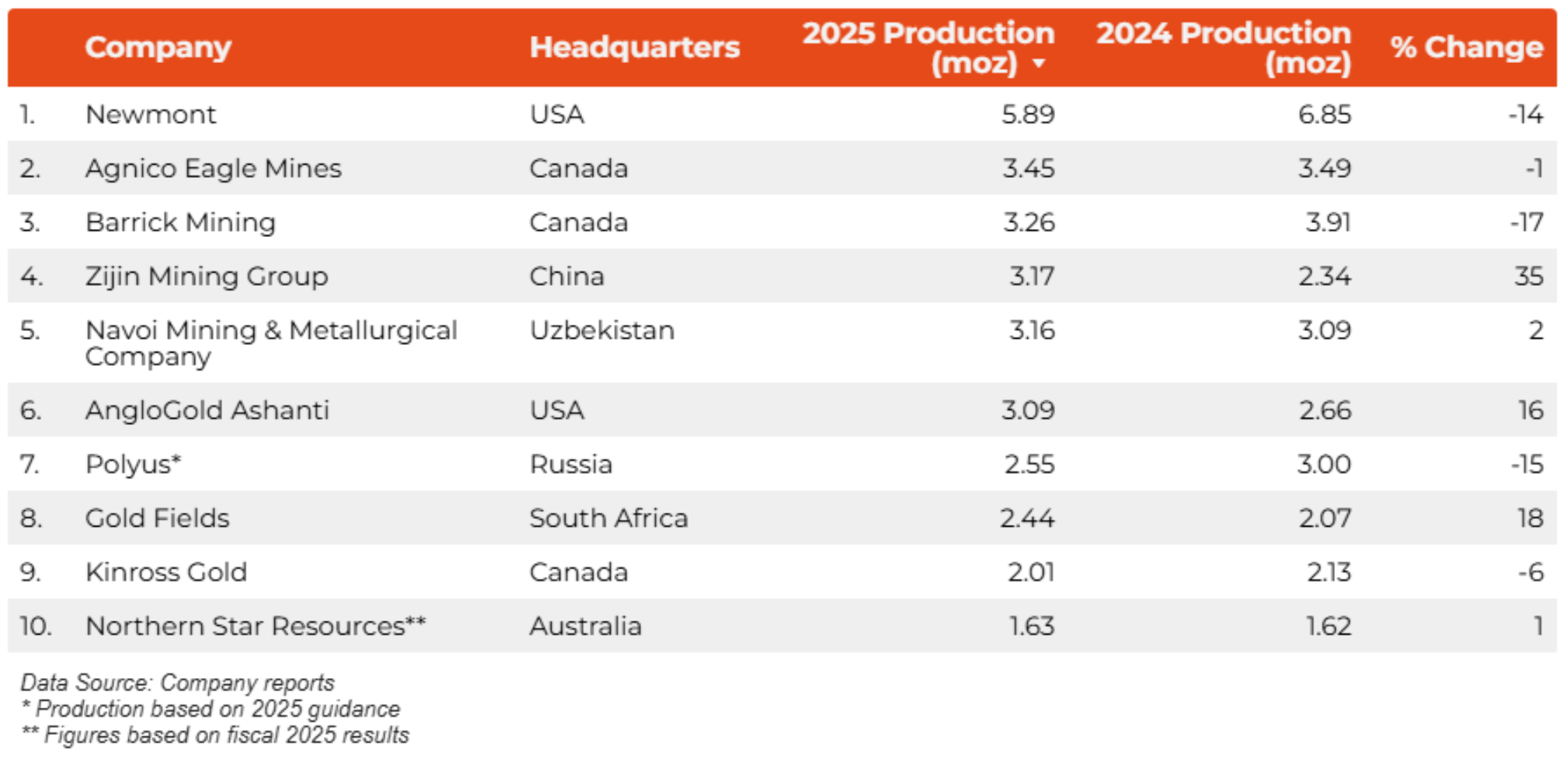

Australia’s Top 10 Gold Producers: Only One ASX Name Makes the List

From the gold price to the big gold miners. With gold near record levels, you’d expect Australia to be all over the global production tables. We’re one of the biggest gold-producing countries on earth, after all.

The thing is when you line up the world’s top 10 gold producers by ounces, there’s only one Australian name on the list, Northern Star Resources (ASX: NST).

Newmont sits at the top with 5.49 million ounces produced in 2025, Agnico Eagle and Barrick are both above 3 million. The rest of the top tier is spread across Canada, Africa, Central Asia and Russia.

Australia’s largest gold producer NST comes in at number 10, producing around 1.63 million ounces. NST is targeting around 3 million ounces down the track after last year’s purchase of De Grey Mining.

At a corporate level, the international majors still control the bulk of large-scale output.

If gold stays strong (which we think it will), consolidation will matter more and more. There’s room for an Australian company to move up that list, and we wouldn’t be surprised to see someone have a crack at it.

BHP Takes Back Australia’s Biggest Listed Company

BHP edged past Commonwealth Bank on Friday to reclaim the title of Australia’s biggest listed company. In afternoon trade, BHP was sitting at roughly $292 billion, just ahead of CBA at about $290.4 billion after the bank’s shares slid 2.2%.

This top spot has been changing hands for months. CBA grabbed it back in early February, BHP had it briefly in January. Over the past twelve months, BHP shares are up more than 40% while CBA’s up closer to 11%.

What moved things on Friday was reporting that CBA has referred itself to police and regulators over up to $1 billion in suspected fraudulent home loans. The issue centres on loans allegedly obtained using fabricated documents, including income statements and AI-generated paperwork, with parts of the activity linked to broker and referral channels.

The loans are reportedly secured with no arrears yet, but the scale raises obvious questions about how those loans got through in the first place. Banks trade on trust, and if the governance questions keep piling up, the premium CBA trades at can shrink quickly.

BHP, on the other hand, is still riding strong copper and iron ore prices. If CBA’s regulatory headaches deepen, BHP could hold this spot for a while.

Argentina’s Copper Boom Hinges on Glacier Law Reform

According to Bloomberg, Argentine President Javier Milei is pushing to amend the country’s 2010 Glacier Law to unlock what could be US$40 billion of copper investment in the Andes.

Real money, real projects. BHP and Lundin jointly own and are advancing the massive Vicuña district, home to the Josemaría and Filo del Sol deposits, which rank among the largest undeveloped copper systems on the planet.

The catch is that Argentina protects glaciers and the frozen ground around them as water reserves. If they’re formally listed, they’re off limits. Some of those ice formations sit directly above or next to major copper deposits, which is where the tension comes from.

Miners want flexibility. Environmental groups see it as gutting safeguards. Both sides have a case, and the political outcome is anyone’s guess.

If the reforms pass, Argentina re-rates as a serious copper jurisdiction overnight and development timelines accelerate across the Andes. If they stall, billions in planned spend stays parked and global copper supply gets even tighter down the track.

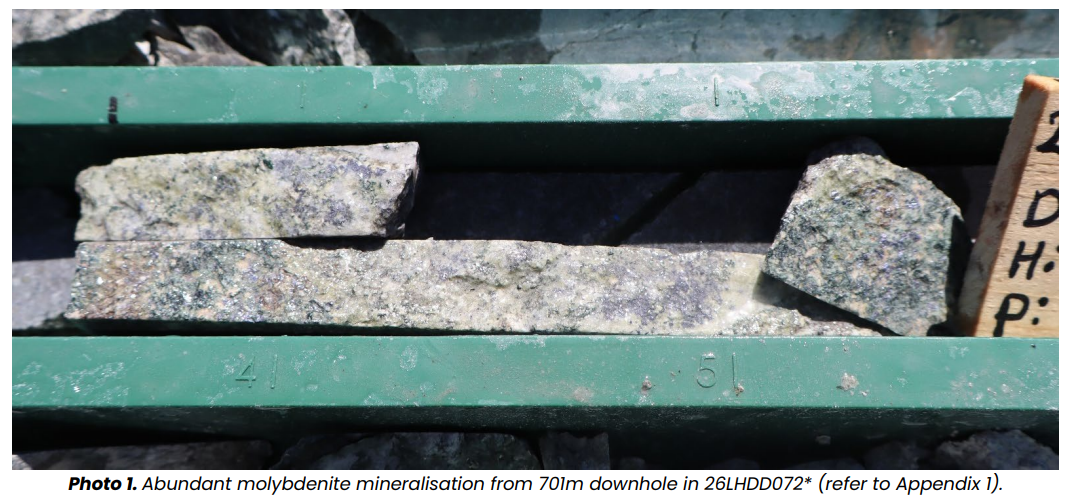

FMR Resources: Mineralised Copper Drill Core Sends Stock Surging

We’ve been following FMR Resources (ASX: FMR) closely since Mark Creasy cornerstoned their raise ahead of drilling last year. It’s a Chilean copper explorer, chasing a big porphyry system at Llahuin in Chile. The full history of our coverage is here.

This week the stock ran more than 20% after FMR confirmed visible copper and molybdenum sulphides within porphyry intrusions at their Southern Porphyry target.

We first called FMR Resources at 17.5c in our 2025 10 Stocks to Watch article early last year, backing the team behind it. The company is led by seasoned geologist Oliver Kiddie, who believes this latest hole is closer to the core of the system than anything they’ve drilled before.

The market read it as a sign FMR could be closing in on a genuine source intrusion, which is a very different proposition to hitting peripheral alteration on the fringes.

What we like about this story is that FMR is doing big porphyry exploration at virtual sea level, within a six-kilometre mineralised corridor at Llahuin in Chile.

Compare that to the Andean plays sitting at 4,000 metres altitude where logistics alone can blow out timelines and costs.

Next steps include downhole geophysics across Targets A, C and K, which will help refine the 3D model, then design a hole to test the interpreted source south-east of Target K.

Plenty of work ahead, but each hole has built on the last. Assays pending.

ASX Weekly Wrap: What to Watch on Monday

The world looks a lot different this morning than it did on Friday. We covered what we know in the Iran section above, but the honest answer is that nobody knows what comes next, including us.

We’ll be glued to the screens tomorrow.

Till next week.

General advice, disclosure and confidentiality

General advice warning

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consulting your own investment advisor to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (“Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 1,554,000 FUN shares, 200,000 10X shares, 187,500 BHL shares at the time of publishing this article. Equities Club has been engaged by FUN, 10X and BHL at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.