Evion Group (ASX: EVG) has a field crew in the Nevada desert right now, sampling ground it reckons could hold a bigger fluorspar system than the one mined out of here in the 1960s.

The project is Carp, in Lincoln County about 140km northeast of Las Vegas. It was a working high-grade fluorspar mine half a century ago, before it went quiet for decades.

EVG picked it up on option in May, stapled on a stack of adjacent ground, and had the old surface sampling independently checked.

That was the groundwork. Today it laid out what happens next.

It’s a staged run of work, built to take Carp from a historic mine with strong surface hits to a set of drill-ready targets with a rig turning.

Each step firms up what’s actually in the ground, which is the part the market can’t price until someone goes and proves it.

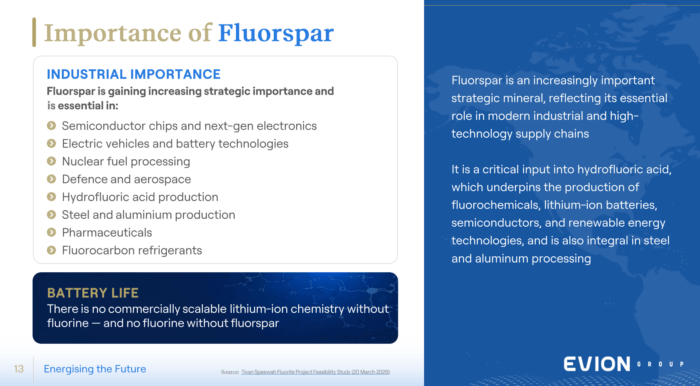

Fluorspar feeds batteries, chips, refrigerants and nuclear fuel, and the US military rates it among its highest supply risks in a conflict.

The price has moved to match (more on that later), and America imports every tonne it uses.

EVG is sitting on a high-grade slab of it in the jurisdiction Washington most wants to buy from. Almost none of that is in the share price yet.

EVG Share Price and the June Selloff

EVG is trading at 3 cents, the same price the raise that funded the Carp deal was done at.

Right now the market is putting next to nothing on the project itself, the historic mine and every claim staked around it.

Most of that is the time of year. June is a notorious month for selling. Thinly traded small-caps often get sold as 30 June approaches, and stocks that have drifted tend to cop it regardless of what’s happening underneath.

Nothing about Carp has changed in the last month, and now there’s a plan to put value on it over the coming months.

Nevada sits at the top of the Fraser Institute’s mining jurisdiction rankings.

EVG’s Carp Exploration Plan

Carp produced fluorspar once, back in the 1960s, but only from what the old miners could see at surface.

The grades EVG has since pulled from the ground sit higher than anything that mine ever sold, and the best of those came from the pits the old crews never finished.

Something’s down there, and the program now running is the hunt for it.

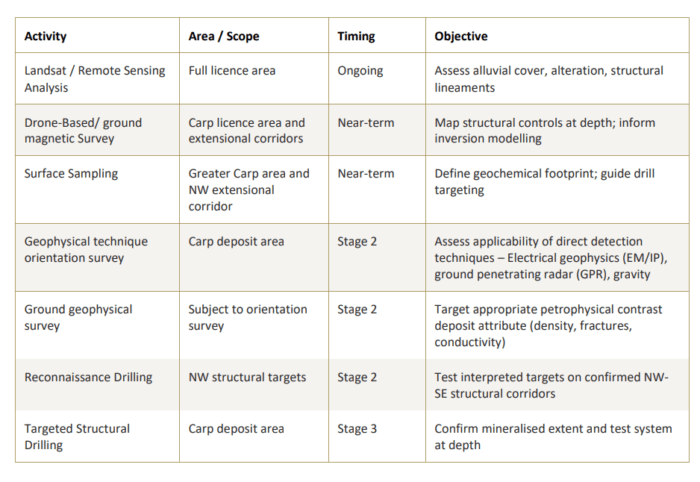

A crew is already on site, collecting rock samples along a corridor on the north-west side of the main claim block. EVG only picked that ground out as a target recently, and it’s the cheapest place to start.

Sampling only reads what’s lying on the surface, and the deeper question of what sits metres below is the one drilling answers, but drilling is where the money goes, so you want the holes pointed at the right ground before the rig ever turns.

The work program, stepped from low-cost sampling through to drilling

That pointing is the job of a magnetic survey, flown by drone or walked across the ground, reading the structures and how they run at depth.

Fluorspar at Carp sits in faults and folds, so tracing those structures traces the mineral itself, and the data builds into a 3D model that turns open ground into a handful of marked targets.

The mineral is noticeably denser than the limestone around it, so the right survey can pick out buried bodies of it the way you’d feel a brick hidden in a bag of feathers.

Fluorspar pulled from Carp, the purple banding running through the rock.

The drilling follows in two passes, reconnaissance holes first across the north-west targets, then deeper structural holes back at the old pits to chase the system down.

The rig only turns once the cheaper work has earned it.

Carp’s Mining History and Grades

Carp has been a mine before. Between 1958 and 1971 it produced 44,900 tonnes of fluorspar from four shallow pits, crushed and sold straight to Kaiser Steel with no other processing.

Fluorspar is graded by how much calcium fluoride, written CaF₂, is packed into the rock. The higher that number, the purer the material and the more it’s worth.

Carp came out at around 69%, enough to sell as it was. At that purity it goes to steelmakers as a flux, the additive that pulls impurities out of molten metal. A mine ran here for 13 years on that grade.

Where fluorspar ends up: chips, batteries, nuclear fuel, defence and steel.

It closed in 1971 for a reason that had nothing to do with the geology. Cheap imported fluorspar flooded the US market and undercut small American producers, until an operation Carp’s size couldn’t make the sums work.

The mineral stayed in the ground, waiting for the economics to swing back. They have.

Verified results from 2024, signed off in May, came back as high as 88.15% CaF₂ across all four old pits, well north of the 69% the mine once sold at.

As purity climbs like that, the mineralisation stops being simple steel flux and starts heading toward acid-grade fluorspar, the premium tier behind batteries, chips, refrigerants and nuclear fuel.

Carp isn’t there yet, but that climb is the whole point. It’s also where the value sits.

Nevada ranks as the top mining jurisdiction in the world on the Fraser Institute’s survey, the gauge explorers use for where it’s safe to sink money into the ground.

EVG’s CARP fluorspar project in the tier-1 mining jurisdiction of Nevada, USA.

Why Fluorspar Is a Critical Mineral

For years almost nobody outside the steel industry could tell you what fluorspar did. That changed when the country that fed the world’s fluorspar started hoarding it.

China mines and uses more fluorspar than anyone, and for years it sold the surplus on. Then it stopped being a net seller and became a net buyer, and the rest of the world was left scrambling for supply.

(It’s worth knowing there are two grades that matter here, because they sell into different worlds).

The lower grade is called metspar, the stuff steelmakers melt into the furnace as a flux.

The higher grade is acidspar, the pure end that gets turned into the acid behind batteries, chips and refrigerants.

Same mineral, dug from the same ground, but the cleaner it comes out, the more it’s worth.

China runs the supply, the US imports the lot, and the deficit is widening

Both have been climbing. The average the US paid for metspar went from US$151 a tonne in 2021 to US$400 in 2025. Acidspar ran from US$322 to US$470 over the same stretch.

Buyers paying more than double in four years is what a supply squeeze looks like before anyone’s built the new mines to fix it.

The US imports 100% of its fluorspar and has for decades, even with old mines sitting idle across the country.

Fluorspar shows up twice on the US military’s list of nine minerals with the highest shortfall risk in a major conflict, once as metspar and once as acid-grade.

The Defense Logistics Agency, the arm of the Pentagon that stockpiles materials for wartime, recently put US$168.9 million into a fluorspar supply contract. On the military side the mineral runs through armour-grade aluminium and jet fuel catalysts as well.

Carp is one of the few high-grade options in America.

What’s Next for EVG at Carp

Right now Carp is a hunch with a strong history.

A mine that ran for 13 years, grades that have come back higher than it ever sold, and a read on a system that runs deeper than anyone has tested.

The sampling, the magnetics, the model and the drilling behind them are each there to turn that hunch into a defined deposit, one low-cost step at a time.

The market only ever pays for what it can measure, and every result that comes back gives it more to go on.

America imports every tonne of fluorspar it uses, the price has more than doubled in four years, and Carp is one of the few high-grade options on US soil in the jurisdiction Washington most wants to buy from.

Fluorspar has waited more than 50 years for the world to come back around. Now EVG finds out how much is down there.

General advice, disclosure and confidentiality

General advice warning

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consulting your own investment advisor to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (”Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 4,500,000 EVG shares. Equities Club has been engaged by EVG at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.