We added KTEK Aerosystems (ASX: KTK) to the portfolio last week. The Israeli drone-parts supplier rang the bell 11 days ago at a $28 million valuation.

The first units since listing are already leaving the warehouse.

Inside the container: 1,100 advanced composite airframe components, packed into 100 finished drone sub-assemblies, heading to one of KTK’s existing Tier-1 customers.

The invoice on this one shipment runs to roughly A$500,000. And there’s plenty more to come. The company is targeting 150 units a month inside five months.

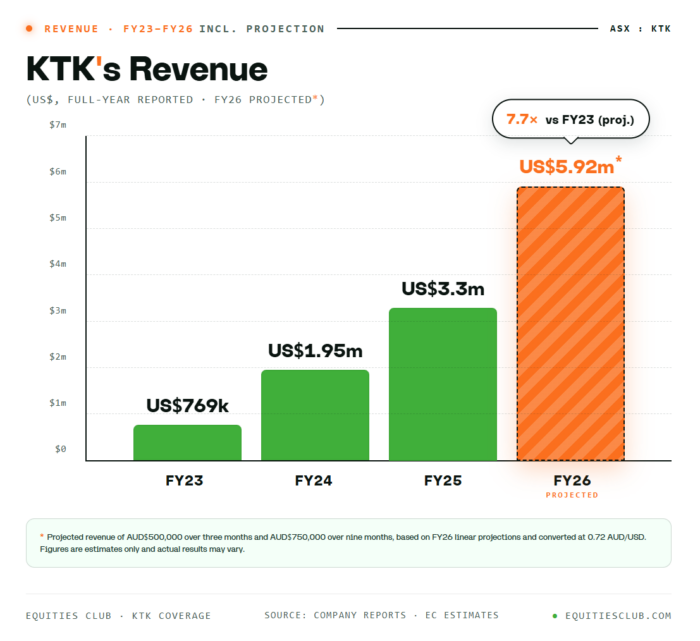

At roughly A$5,000 a unit, that works out to about A$9 million in annual revenue off existing customer contracts, before any of the IPO money goes to work pushing deliveries further across the back half of 2026.

Dekel Keisar, KTK’s founder and managing director, put it plainly:

“Our focus now is simple: ramp as fast as we can and convert our order book into delivered units and recognised revenue.”

At 31.5 cents, KTK is valued at roughly 5 times that $9 million revenue run-rate.

For context, Electro Optic Systems (ASX: EOS) trades closer to 14 times revenue and Elsight (ASX: ELS) sits north of 35 times.

KTK is the cheapest of the three.

Supply Lines Reopen

When we wrote up KTK last week, the conflict in the Middle East was still hot and the region’s supply chains were running on rations.

Components dribbled through when they could and production sat at a fraction of capacity.

The order book for KTK kept piling up while the parts to fulfil it sat on the wrong side of a border.

The picture has shifted in the past few days. The US is leaning hard on every party in the room to get a peace deal across the line, and the freight lanes have responded faster than the diplomats trying to negotiate peace.

Trucks are moving. Ports are clearing. The European facility has now cleared the first shipment out the door.

It’s still a fragile setup. A peace deal that’s being negotiated by the hour can come apart by the hour. But for the first time since KTK rang the bell, the parts are flowing where the orders are.

What the Shipment Feeds Into

The shipment announced today was half a million dollars. The cycle it feeds into runs to hundreds of billions.

The US has earmarked US$75 billion for drones and counter-drones in its FY27 defence budget. NATO is targeting 5% of GDP on defence by 2035. Europe has pooled US$870 billion for rearmament. Australia is in for A$22 billion over the decade.

It’s a procurement cycle so large it has its own acronyms (DAWG, DDP, JADC2, pick your alphabet), its own committees, and its own line in the budgets of dozens of governments.

The big drone-makers are the ones running the procurement gauntlet and winning the government contracts. KTK isn’t in that fight.

KTK supplies the parts that go inside the drones those contracts pay for, which means whichever drone-maker wins the tender, KTK’s parts are still in the aircraft and KTK still gets paid.

The drone-makers buying from KTK today include Elbit Systems and UVision, two of the most established names in the Israeli defence drone industry. The drones they sell, with KTK components inside, are flying in active conflict zones and sitting in the stockpiles of Western defence forces.

Two more Tier-1 names with combined revenues above US$10 billion have already cleared KTK as an approved supplier.

Getting to that stage takes between one and three years of facility audits, aerospace certifications, prototype runs and small initial orders.

The grind that buries most early-stage defence manufacturers before they ever ship at scale has already been ticked off by KTK.

One shipment is small in the scheme of what’s to come. The supply chain underneath it is built to ship years of them.

KTEK founder and managing director, Dekel Keisar on business operations:

“Supply chain conditions have normalised and we are back to business as usual, shipping product, generating revenue and building toward our full production run-rate. This first delivery on its way to our customer marks the beginning of what we expect to be a regular and growing cadence of shipments.”

How KTK Ramps Without Needing a Factory

Most small defence companies, sitting where KTK is sitting today, would announce a factory.

A press release would go out. The capital raise would follow. Shareholders would get diluted to fund the concrete, the machines and the floor staff. By the time the doors opened, the order book would have moved on.

KTK has spent the past seven years building a way to not do that.

The model is called the Cordless Factory. KTK keeps the engineering work, the structural design and the quality assurance in-house, sitting with the team that has the certifications and the customer relationships.

The actual making of things, the cutting and laying and curing and assembling, sits with a network of aerospace partners across Israel, Europe, Thailand and the US.

When demand grows, KTK allocates more work into the network.

The proof is in the numbers from before the IPO. KTK quadrupled revenue between FY23 and FY25 without going back to shareholders for cash. Same share register, four times the revenue.

That’s the engine that gets KTK from the 100 units shipped this week to the 150 a month target.

The IPO money sitting on the balance sheet will push it even further than that.

What Lands Next

The shipment that left this week is the start of a list. There are four things to watch for between now and the next time we write about KTK.

- The next Elbit and UVision invoices. This week was 100 units. The 150-a-month target covers contracted demand from those two customers, and every monthly shipment between now and then is a revenue line the market can see.

- The first purchase order from a new Tier-1. Two more Tier-1 names have already cleared KTK as an approved supplier. That’s the hard yards done. The next step is converting that paperwork into an actual purchase order, then into a supply agreement that locks KTK in across a multi-year platform.

- The US partner. American drone procurement is the biggest single piece of the global cycle, and a lot of that money requires US-located manufacturing to qualify. KTK has flagged the US as the next geography to add to the Cordless Factory network. The sooner that partner is online and certified, the sooner KTK is eligible to ship into American programs.

- Growth outside defence. KTK also supplies agricultural and delivery drone operators, which sit completely outside the defence budget cycle. Any traction in that part of the book is upside on top of the defence story.

Our View

Last week, KTK rang the bell at 20 cents with a story about ramping into the biggest defence buildup since the Cold War and converting an existing order book into recognised revenue.

This week, the first container since listing is on its way to a customer, the invoice is sitting at half a million dollars, and the company is targeting 150 units a month inside five months.

The world has decided it needs more drones. The companies KTK supplies are the ones building them. KTK has spent seven years getting to the point where it can ship parts into that demand at scale.

This week was the start of it showing up.

General advice, disclosure and confidentiality

<p data-pm-slice=”1 1 []”>General advice warning</p>

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consulting your own investment advisor to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (”Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 500,000 KTK shares. Equities Club has been engaged by KTK at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.