Three portfolio additions on the trot, three flyers.

AI1 is up around 270% since we added it. EVG is up more than 80% in a fortnight, after ripping 60% on its opening day. And this week KTEK Aerosystems (ASX: KTK) joined the portfolio, listed at 20c on Monday morning, and closed the week at 38c.

Ninety percent up in five sessions. The kind of start most listed companies don’t see in their first year of trading, let alone their first week.

The thread tying all three together is the same one running through the whole small-cap end of the market right now. Money is moving fast into defence and critical minerals, and the smaller end of the ASX is where that money keeps finding its biggest leverage.

The rest of the portfolio moved with it. Mount Ridley kicked off the metallurgical work that decides whether its heavy rare earths actually come out of the ground, and Evion brought in a 45-year mining veteran as chair.

Outside the portfolio, the man who built Northern Star from a $363 million WA junior into Australia’s largest gold producer stepped down. We’ll get to him further down.

Let’s get to it.

- KTK closes its first week on the ASX up 90%

- Defence and drones move into the hottest pocket of the small-cap market

- Mount Ridley shifts from rare earths discovery toward processing

- Evion brings in a 45-year mining veteran as chair

- Patrys lines up the clinical trial site for the delirium program

- The MD who built Northern Star from $363m into a $27 billion giant steps down

- Guzman y Gomez rallies after walking away from the US

KTK Closes Its First Week Up 90%

Somewhere on the Tel Aviv outskirts in 2019, an Israeli structural engineer named Dekel Keisar was working on a counter-theory.

Everyone else in the defence industry was building bigger, more expensive flying platforms. Dekel had spent his career inside that industry.

He thought it had the future backwards.

The drones that would matter, he’d decided, were the cheap ones. The ones you could build by the 1000s and lose without having to write a memo to a general.

Seven years later, the Pentagon agrees with him. KTEK Aerosystems, the company Dekel started with that hunch, listed on the ASX this Monday at 20 cents. It closed the week at 38, up 90%.

For new readers, KTK builds the components that go inside military drones. Wings, frames, landing gear, electromechanical assemblies. The names on the finished platforms, Elbit, UVision and the rest, buy those parts and bolt them in.

It’s the picks-and-shovels play of the drone boom.

We went long on the full breakdown on Monday. The IPO closed three times oversubscribed, with $30 million in bids for a $10 million raise that filled in under 24 hours.

Regal Funds Management, Thorney Investment Group and US-Israeli defence fund Scopus Ventures are on the register. Board and management hold 44%, while the top 20 holders sit at 70%.

Speaking with Dekel last week, one line stuck with us. He’d been attracted to small drones twenty years ago, when nobody in the industry took them seriously.

“Back then, most of the industry was focused on big, expensive flying platforms. I thought it makes sense to have small platforms, cheaper platforms, that you can manufacture in huge capacities … now that is what actually happens.”

– Dekel Keisar, Founder, KTEK Aerosystems

The man bet his career on what the Pentagon now openly embraces. And the numbers behind that shift are extraordinary.

For KTK specifically, the move from here is operational. First purchase orders from the two newly approved Tier-1 contractors. A US manufacturing partner online. New customer wins beyond the existing book.

Each one is a chance for the market to re-rate.

Mount Ridley Moves From Discovery Into Processing

There’s a moment in the life of a junior critical minerals story where the question shifts.

It stops being “Have you found something” and starts being “Can you actually get it out of the ground?”. Most companies never make the shift. The graveyard of ASX rare earth juniors is full of names that had a resource, couldn’t crack the chemistry, and quietly disappeared.

Mount Ridley Mines (ASX: MRD) started making the shift this week.

The company kicked off Phase 1 metallurgical testwork at Perth lab Nagrom, running the heavy rare earth, scandium and gallium mineralisation from its Grass Patch project through the chemistry that decides whether the rocks become a mine or a footnote.

You can find our full note on this weeks news here.

Running the program is Chris Larder, who joined MRD three weeks ago after spending 30 years building flowsheets in WA, including time at Alcoa’s Wagerup gallium plant and Lynas’ Mt Weld rare earth separation facility. The two WA operations MRD’s basket could realistically feed into.

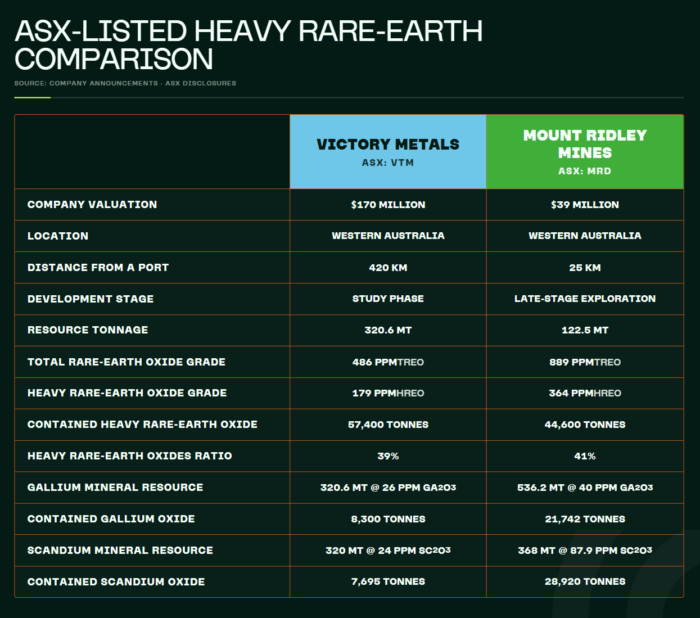

The piece of this story we keep coming back to is the comparison with Victory Metals (ASX: VTM). Same clay-hosted, heavy-loaded deposit style. Same WA jurisdiction. VTM is well into pre-feasibility on its North Stanmore project with strategic partners on the books, and the market values that work at around $170 million. MRD sits at around $39 million.

That’s just under five times the gap on the same style of deposit, with one detail in MRD’s favour. VTM’s resource holds heavy rare earths and scandium. MRD’s holds all of that, plus gallium. The full set. And Grass Patch sits 25 kilometres from port in WA, which is a head start most of its peers don’t have.

Phase 1 doesn’t close that valuation gap on its own. The work in front of Larder’s team is the work VTM was doing two years ago. What it does is start the technical case the rest of the development pathway gets built on.

The Defence Pivot on the ASX

Three years ago, a Russian tank cost millions of dollars and a Ukrainian drone cost a few thousand. The tank won that fight every time.

Now, the tables have turned.

The footage coming out of eastern Ukraine over the past 18 months has done more to shift Western defence procurement than any think tank report ever could.

There’s numerous clips around the internet of a backpack drone taking out a piece of armour that took a year to build and a decade to design.

The maths of war has been rewritten in front of a live audience.

The Pentagon, NATO and the Australian Defence Force have all seen the same footage and arrived at the same conclusion. The next war is going to be fought with things that cost less than a used car, built at mass scale.

Behind it sits Australia’s $15 billion commitment to autonomous systems, NATO targeting 5% of GDP by 2035, and Europe’s US$870 billion rearmament pool. The money has to find somewhere to go.

Some of it is finding the ASX.

Adisyn (ASX: AI1) has been on a run as the market has worked out what graphene stealth coating means for a drone the size of a quadcopter, and KTK turned a lot of heads in its first week on the ASX.

The trade has now spread well past what we own.

1414 Degrees (ASX: 14D) ripped another 60% this week on its aerospace and defence battery materials pivot.

AnteoTech (ASX: ADO) jumped 40% after validating drone applications for its Ultranode battery technology.

Both were industrial materials stories 12 months ago, and are now defence stories, because the money inside the sector has decided that’s what they are.

The thing to remember about defence trades is they don’t usually run on quarters. They run on procurement cycles, and the cycle that just opened is the biggest one since the Cold War.

The companies sitting inside it now are the ones that get to compound and the market is finally waking up to where the next generation of defence spending is heading.

Big Changes at Board Level as EVG Ramps Up

Evion Group (ASX: EVG) spent the week reshaping its leadership team, and the stock finished about 10% higher at 5.5c.

The headline appointment was Mal Randall stepping in as non-executive chair.

Randall brings more than 45 years across the resources sector. Senior Rio Tinto roles. Lithium, rare earths, graphite and broader critical minerals development. A career that’s run through every cycle the Australian resources sector has produced since the 1980s.

He doesn’t take chair roles on a whim at this point.

EVG has a few moving parts inside the business now, and they’re all maturing at the same time.

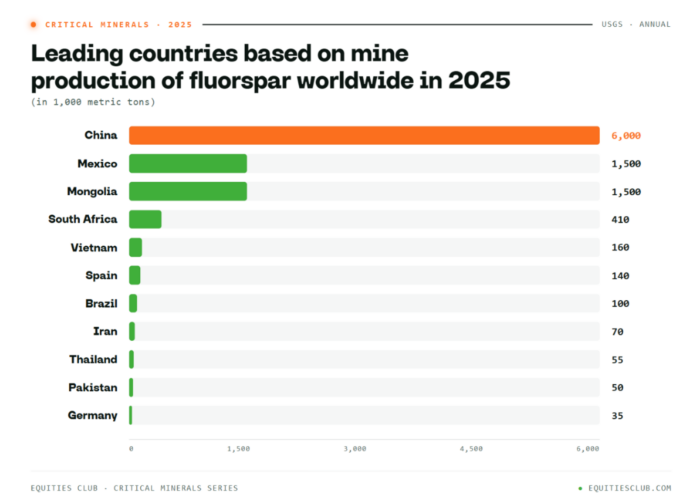

The newly acquired Carp fluorspar project in Nevada gives the company exposure to a mineral that quietly underpins lithium-ion battery electrolytes, semiconductor manufacturing, uranium enrichment and refrigerants.

China controls global supply. The US imports effectively all of it.

That’s the kind of imbalance Western governments have spent the past two years actively trying to fix.

Alongside fluorspar sits the Maniry graphite project in Madagascar, advancing toward Final Investment Decision under the EU Critical Raw Materials framework.

Graphite remains one of the core inputs for lithium-ion battery production, and Maniry is well advanced compared to most ASX peers in the space.

Underneath those two sits the Indian graphite JV, which already generates revenue and ships into international markets today.

The company also strengthened the technical bench this week with geologist Mark Fletcher, whose background spans nickel sulphides, gold and IOCG systems.

A year ago EVG was a graphite story.

Today it sits across fluorspar in Nevada, graphite permits in Madagascar, revenue in India, and a Rio Tinto-pedigree chair at the top.

This increasingly feels like a company trying to build a diversified critical minerals platform across multiple commodities, jurisdictions and revenue pathways rather than relying on one standalone project outcome.

PAB Lines Up Its First Human Trial

Patrys (ASX: PAB) climbed nearly 20% this week after the company lined up the two pieces it needed to put RLS-2202 into actual humans.

The Phase 1A trial site is now CMAX, one of Australia’s most established clinical research facilities. Alithia Life Sciences will run the day-to-day management of the study.

A biotech can talk about a drug for years before anyone actually receives it. Naming the trial site and the operator is the step that moves the conversation out of the lab.

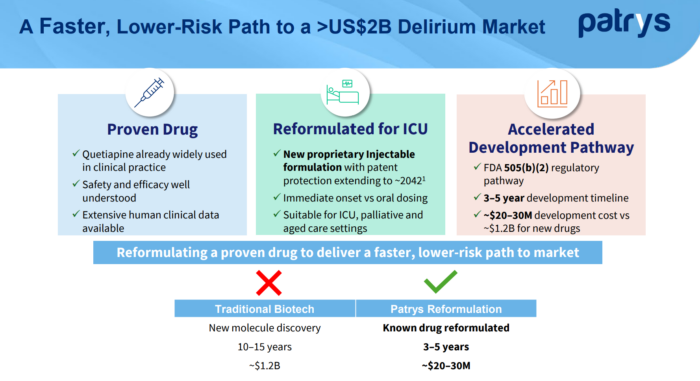

RLS-2202 is an injectable designed for acute care, where the target is delirium.

Picture a nurse on a hospital ward at 3am, sitting with an 82-year-old who came in for a hip replacement and woke up confused, agitated, pulling at his IV lines.

That’s delirium. It strikes elderly patients hardest, particularly after surgery or in intensive care. It lengthens hospital stays, slows recovery, and raises mortality.

The patient pool is substantial. Ageing populations across the developed world keep elderly hospital admissions climbing every year, and delirium turns up in a meaningful share of them.

Acute care is a setting where speed matters more than almost anywhere else in medicine, and the treatment options on the ward for delirium haven’t meaningfully moved in decades. PAB’s pitch is that an injectable formulation can deliver faster and more reliably than what’s currently in use.

The company is targeting first participant dosing in Q3 2026, subject to approvals.

Biotech investing changes when a program crosses into humans.

Before that point, the market is pricing a thesis. After it, the market is pricing data. The two are different exercises with different multiples attached, which is why biotech share prices tend to move sharply around the moment of the crossing.

PAB isn’t there yet. But this week the company put the infrastructure in place to get there.

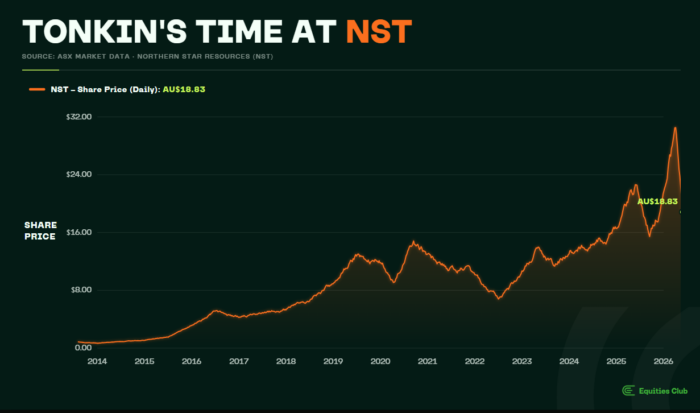

The 30-Bagger Walks Off the Job

In 2013, Northern Star Resources was a 85.5c stock with a $363 million market cap and a few WA gold mines on the books. The kind of name that scrolled past most retail investors without registering.

That year, a mining engineer named Stuart Tonkin joined as chief operating officer.

This week, Northern Star (ASX: NST) announced Tonkin will step down during Q1 next year.

The stock sits at $18.83 and the company is worth almost $27 billion. It runs three major production hubs across Western Australia and Alaska, employs more than 10,000 staff and contractors, and is now Australia’s largest gold producer.

Every reader of this wrap is quietly hunting for a company that goes from speculative to serious while the rest of the market is still looking the other way. Northern Star is the closest the Australian gold sector has come to that template in the last decade.

Tonkin built it through the deals he did along the way.

The Saracen merger reunited ownership of Kalgoorlie’s Super Pit for the first time in generations. The acquisition of De Grey brought Hemi, one of the most significant undeveloped gold discoveries in the country, onto the balance sheet.

Those weren’t the only deals across the decade, but they were the ones that defined what Northern Star was going to be.

The past 18 months have been harder, with production downgrades and operational frustrations.

These are the kinds of pressures that catch up to companies once they get big enough, but the decade that came before is a story to be proud of.

Northern Star sat at the speculative end of the ASX in 2013. The same end where EC readers spend their mornings. The chance to compound a small company into a serious one is still on the table for someone today.

Tonkin’s decade is proof of what it takes to grab it.

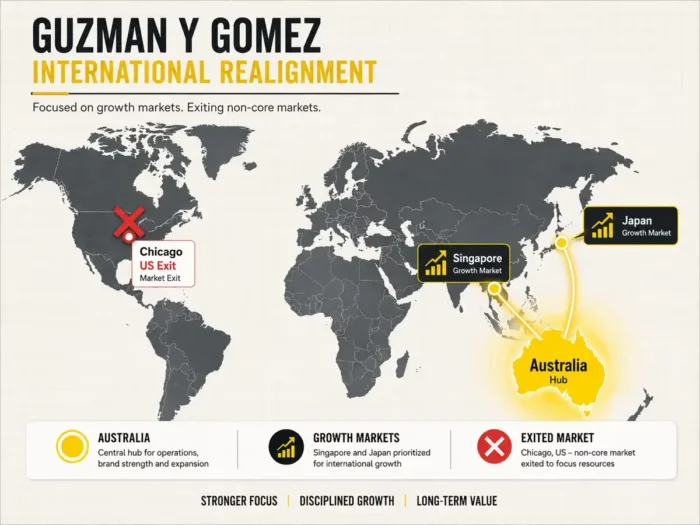

Burrito or Bust: GYG Calls Time on America

Guzman y Gomez (ASX: GYG) walked into America in 2020 with its flagship store in suburban Chicago and a plan to take the country.

This week the company walked out with a writedown and an apology.

In response, the stock ripped.

The maths of failure in the US fast-casual market is brutal. Chipotle has been refining its operation for 30 years and runs more than 3,500 stores.

The American consumer has a 1000 places to buy a burrito within a half-hour drive of any major city.

A handful of Australian-accented imports in Chicago weren’t going to change that, and the longer GYG kept trying, the more capital it was burning to find out.

Management drew the line this week. All eight Chicago restaurants shut and US expansion plans were abandoned. The company will wear a one-off financial hit exiting the market.

Investors rewarded the retreat, the opposite of what management teams usually get for waving the white flag on a growth story.

GYG upgraded guidance for Australian underlying pre-tax profit to roughly $85 million for FY26, representing growth of almost 30% year on year.

With the US write-off behind them, that growth now sits in front of the market with nothing in the way.

Expensive offshore growth stories that aren’t working have lost their patience this year on the ASX. Capital wants to see discipline before it sees ambition.

GYG had been carrying the US rollout as a question mark on the stock for years. The Australian business was doing the work, and the American one was the story management kept asking the market to believe in.

Even after falling from above $43 to below $20 over the past 18 months, GYG still carries a valuation around the $2 billion mark. That’s the price the market is now willing to pay for a focused Australian business with 30% pre-tax profit growth and no US story attached.

Sometimes the bravest decision a management team can make is the one that admits the last decision was wrong.

GYG made it this week.

The Week Ahead

May closes out next week.

The small-cap end of the market still feels in better shape than the big end. Defence and critical minerals have been catching bids all month, and neither trade looks done.

Mineral Resources restarted Bald Hill this week. For two years the lithium majors have been writing down assets and pulling production. This was an early move in the other direction.

Sentiment across the smaller end of the lithium space picked up off the back of it, and there are a lot of names down there with operational leverage they haven’t been able to use in quite some time.

Gold is up roughly 50% on this time last year. Half the small-cap gold sector is still priced as though that move hasn’t happened, which means a meaningful chunk of the ASX is sitting on potential margin expansion.

Exultant Mining (ASX: 10X) is the big one we’re sitting on. The maiden NSW drill program is underway and results could land any time. At a $7.5 million valuation, 10X is the smallest company in our portfolio, and positive assays could move the share price quickly.

From our side, the news flow into June is busy. Portfolio companies advancing, drill bits turning, and now a market rewarding the work.

Till next week.

General advice, disclosure and confidentiality

General advice warning

The contents of this document are intended to provide general securities advice only and have been prepared without taking account of your objectives, financial situation or needs. Because of that you should, before taking any action to acquire or deal in, or follow a recommendation (if any) in respect of any of the financial products or information mentioned in this document, consult your own investment adviser to consider whether that is appropriate having regard to your own objectives, financial situation and needs. If applicable, you should obtain the Product Disclosure Statement relating to the relevant financial product mentioned in this document (which contains full details of the terms and conditions of the relevant financial product) and consider it before making any decision about whether to acquire the financial product. Whilst the Equities Club Pty Ltd (“Equities Club”) believes information contained in this document is based on information which is believed to be reliable, its accuracy and completeness are not guaranteed and no warranty of accuracy or reliability is given or implied and no responsibility for any loss or damage arising in any way for any representation, act or omission is accepted by Equities Club or any officer, agent or employee of Equities Club or any related company.

Neither Equities Club, nor any of its directors, authorised representatives, employees, or agents, makes any representation or warranty as to the reliability, accuracy, or completeness, of this document or any advice. Nor do they accept any liability or responsibility arising in any way (including negligence) for errors in, or omissions from, this document or advice.

Disclosure

The directors, authorised representatives, employees and associated persons of Equities Club may have an interest in the financial products discussed in this document and they may earn brokerage, commissions, fees and advantages, pecuniary or otherwise, in connection with the making of a recommendation or dealing by a client in such financial products. Equities Club owns 500,000 KTK shares, 2,083,333 MRD performance rights, 900,000 AI1 performance rights, 200,000 10X shares, 4,500,000 EVG shares at the time of publishing this article. Equities Club has been engaged by KTK, AI1, MRD, 10X and EVG at the time of writing.

Confidentiality notice

The information contained in and accompanying this communication is strictly confidential and intended solely for the use of the intended recipient/s. The copyright in this communication belongs to Equities Club. If you are not the intended recipient of this communication please delete and destroy all copies immediately.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No 519872.