The Easter wind-down might’ve slowed trading, but plenty of stories kept bubbling away underneath. The holiday lull gave us a chance to step back and spot the patterns forming for the months ahead.

Gold’s relentless record climb continued, Pilbara Minerals dropped its quarterly, showing where lithium stands now and hinting at what could be around the corner.

And over in America’s heartland, natural hydrogen drilling kicked off in Kansas, a development worth watching for resource investors with an eye on emerging energy plays.

Plenty to keep an eye on, even with half the market already thinking about hot cross buns.

Here’s what we’re unpacking this week:

- Gold breaks $3,350 – and why the majors might soon go shopping

- Lithium’s reality check – Pilbara’s numbers reveal the true state of play

- Natural hydrogen comes alive – Kansas drilling could shift the landscape for ASX players

Let’s get to it.

Gold price surges past US$3,350 as M&A chatter builds

Gold powered to fresh all-time highs this week, touching an eye-watering US$3,357.40 per ounce as investors continued piling into the yellow metal.

The drivers remain familiar – escalating trade tensions (most notably, the US and China), recession whispers growing louder in financial circles, and investors seeking shelter from market volatility.

Goldman Sachs has already torn up its previous forecasts, now tipping gold to hit $3,700 per ounce by year-end. Their analysts even float the possibility of $4,500 should those recession fears materialise into reality.

Despite gold’s stellar run, junior gold exploration companies are still not being rewarded. While the metal itself breaks records, companies searching for it can barely attract a second glance from investors.

The disparity between soaring gold prices and the stagnation of junior explorers’ valuations suggests a potential opportunity for investors.

Major mining companies aren’t blind to this opportunity. With their own reserves depleting and replacement costs rising, they’re increasingly eyeing junior projects as acquisition targets. The ingredients for an increase in M&A activity are mixing nicely.

For junior explorers with their wits about them, this is actually a decent time to be getting their ducks in a row. Keep drilling, keep hitting milestones, keep chatting up potential partners. When the tide turns (and it always does), they’ll be the ones getting the calls.

Investors should closely monitor developments in the sector. Once the penny drops and this pricing gap closes, you might see a proper rush back into quality gold projects. And we all know how that movie ends. Latecomers always pay top dollar.

Lithium market outlook: Pilbara Minerals reveals state of play

Spodumene prices, demand forecasts and funding implications

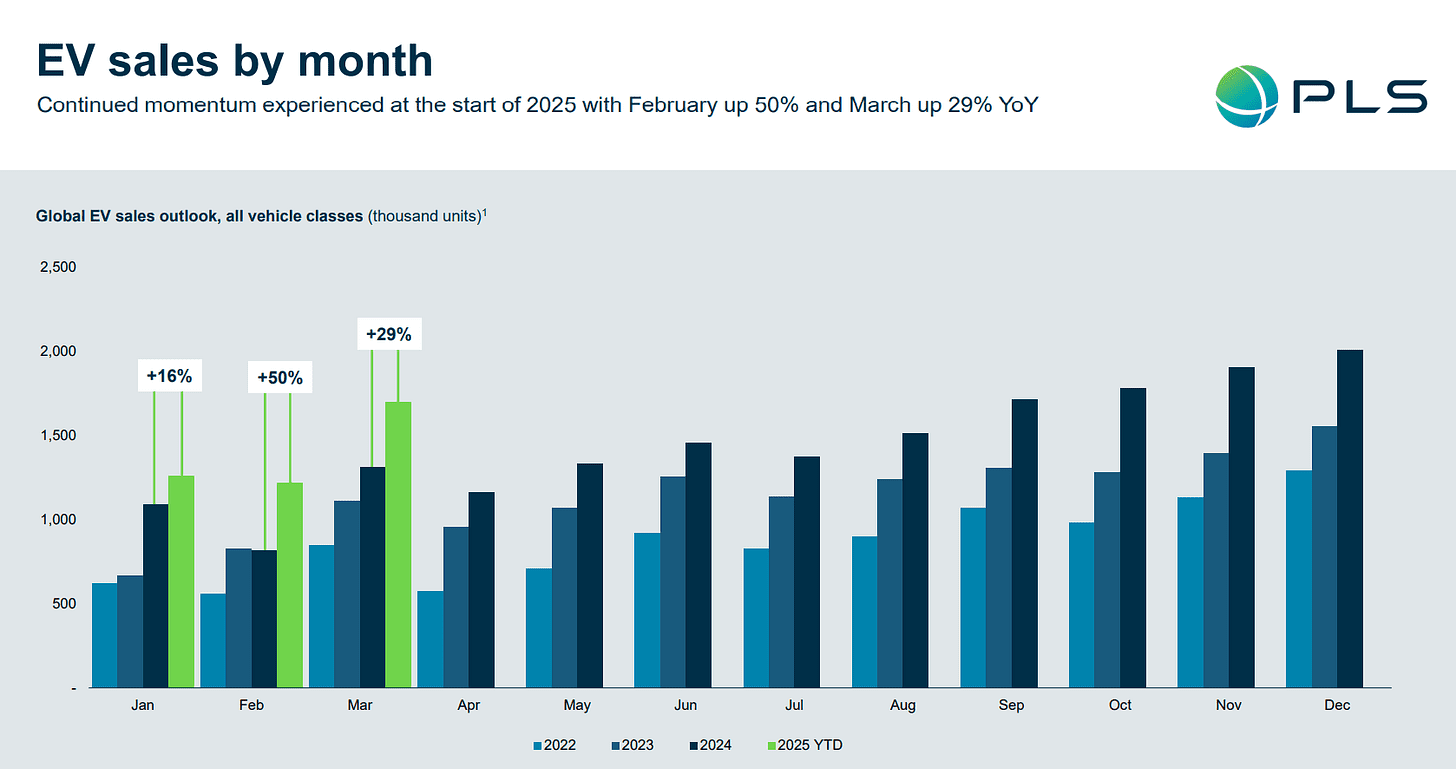

This week, Pilbara Minerals (ASX: PLS) released its March quarterly report, giving us a look under the hood at Australia’s largest lithium producer and how it’s adjusting to the current choppy waters.

Spodumene prices ticked up 7% to US$747/t during the quarter – a small step in the right direction, but let’s not pop the champagne just yet. That’s still less than half what producers were getting this time last year.

Production and sales volumes were down due to operational adjustments, but the company still expects to hit its yearly production targets. While this resilience is encouraging, it’s not reflective of the broader market, which remains under pressure from an oversupply dynamic and weaker near-term demand growth.

Looking more broadly, lithium prices have stabilised from their late 2023 collapse but remain subdued. According to Benchmark Minerals, spot spodumene prices remain too low to make new projects worthwhile for most operators.

Expansions in Australia and Africa have added to the glut, while many new projects funded during the past boom are slowly coming online. This has created a near-term mismatch: Demand is growing, just not quickly enough to mop up all this new supply washing into the market.

For junior lithium explorers, this pricing environment presents real challenges. Equity markets have become more selective, with capital tougher to secure and institutional investors sitting tight until prices show clear signs of recovery.

Several pre-development projects are on hold, and drill programs are being deferred or scaled back. Without offtake agreements or strategic partners, juniors risk becoming stranded.

The AFR covered this rather well recently. Even with government interest in downstream processing, developers still need tax breaks or subsidies to keep their heads above water.

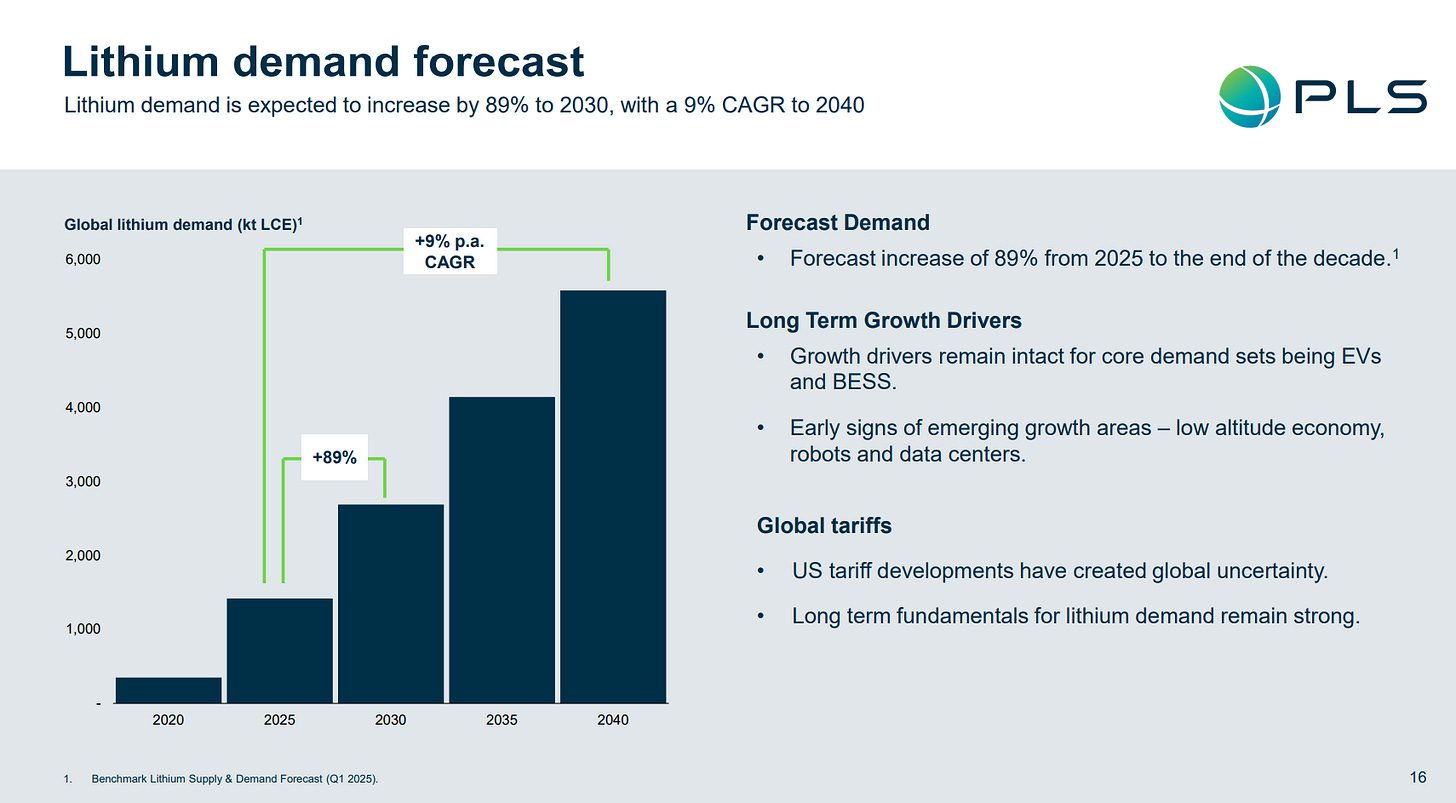

Despite the headwinds in the short term, the long-range forecast remains positive.

Lithium demand is still expected to grow by nearly 90% by 2030, driven by EVs, grid storage, and industrial applications. Battery storage systems are emerging as a significant second growth driver alongside EVs, with installations ramping up worldwide.

The question now is whether we see another lithium boom or a more mature, cyclical upswing.

Investment banks expect prices to climb gradually rather than rocket back to the extreme highs of 2022. Goldman Sachs forecasts spodumene prices to trend towards US$1,200–1,300/t over the medium term, reflecting a more balanced market.

Macquarie takes a slightly more bullish view, citing long-term supply-side challenges, particularly in bringing new Tier 1 resources online.

The consensus is that current prices are unsustainable for most new projects and that without a decent recovery, future supply will fall well short of needs. This would set things up nicely for stronger pricing as we push through the back half of this decade.

For junior explorers, it’s time to bin the old “we’ll be in production by Christmas” pitch. Smart players are now focusing on resource quality, strategic partnerships, and flexibility over the long haul.

The sector’s having a bit of a clearout, not a collapse. For savvy investors, this is prime hunting season – look for companies with staying power, tier-1 geology, and management teams who’ve seen cycles before and know how to navigate them (and manage capital).

The boom may not be back yet, but the groundwork for the next one is quietly being laid.

Natural hydrogen drilling begins in Kansas, with ASX eyes on HyTerra and TEE

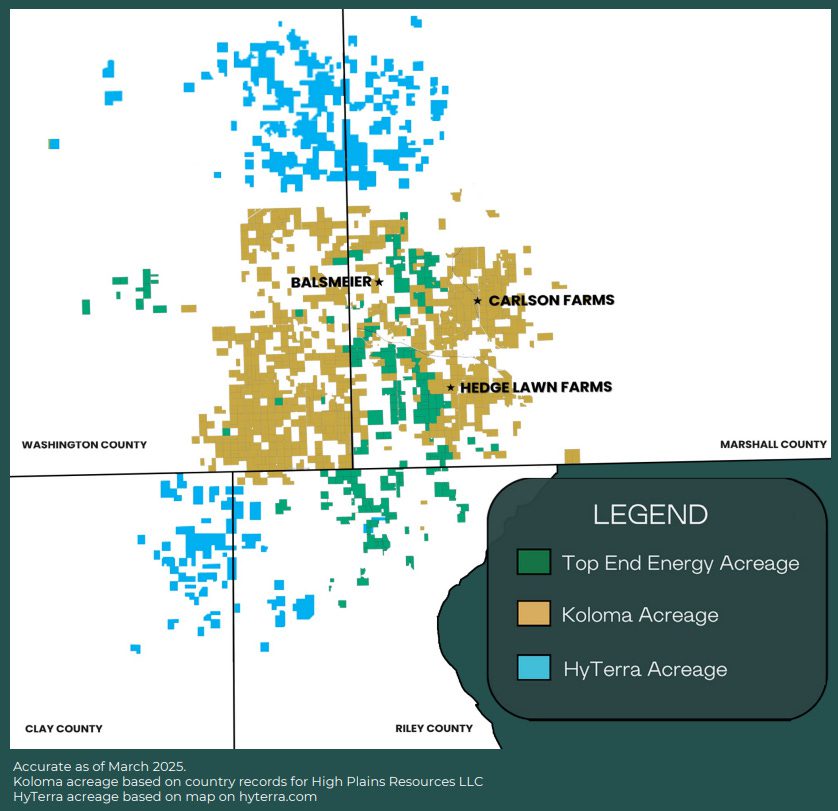

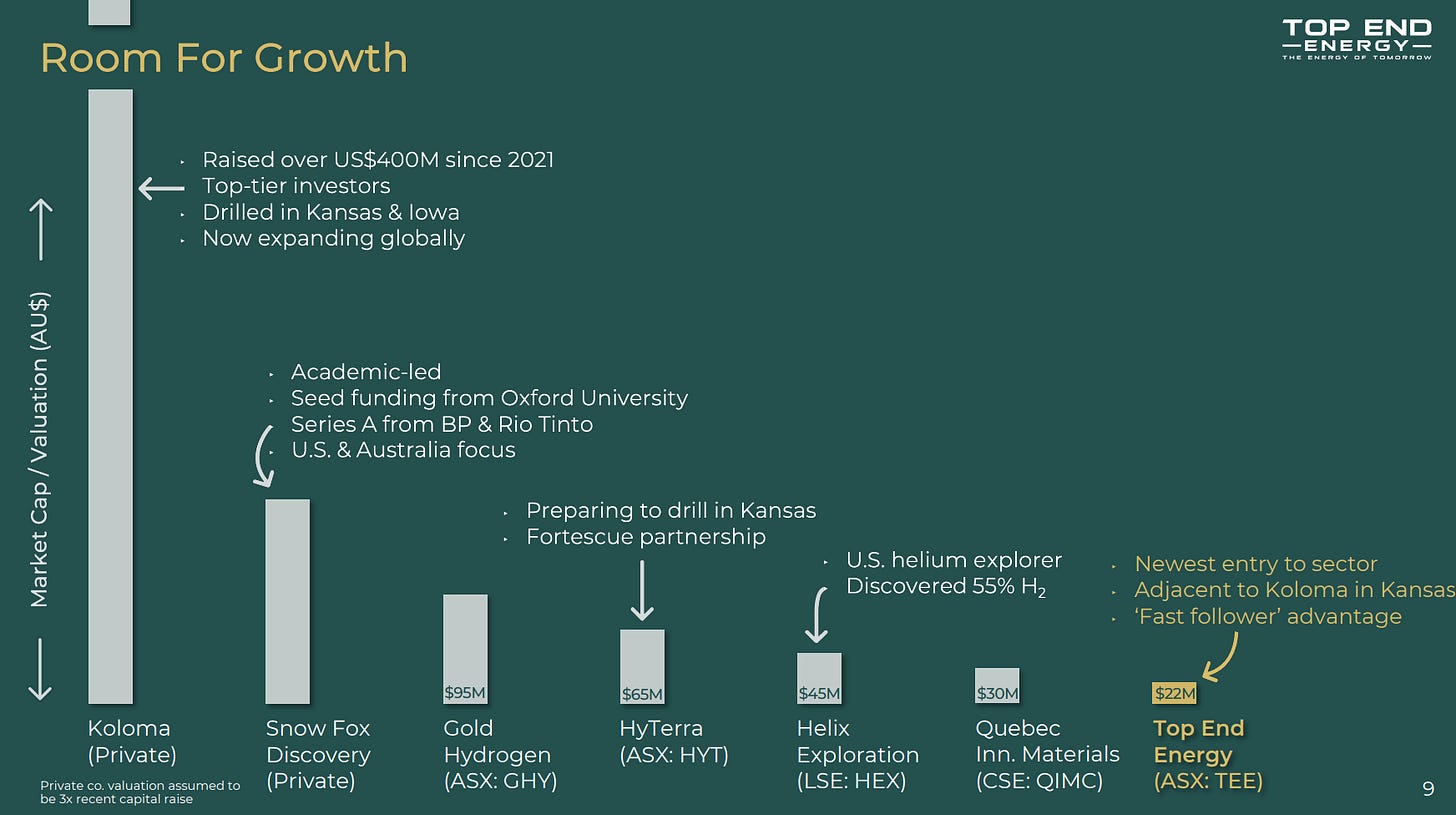

While our investment in Top End Energy (ASX: TEE) gears up for drilling in the coming months, we will be watching very closely the nearby results of Hyterra, which began drilling this week.

The natural hydrogen-focused Hyterra sports a market cap north of $65 million, while TEE sits at roughly $20 million. That valuation gap looks interesting when you consider they’re chasing the same prize in the same Kansas postcode.

HyTerra has kicked off drilling the first of two wells at their Nemaha Project, backed by Fortescue Future Industries as part of a 12-month program.

The program aims to validate historical reports of elevated hydrogen and helium concentrations in Kansas.

This campaign matters for everyone with skin in the Kansas hydrogen game. Natural hydrogen could potentially undercut manufactured hydrogen on cost by a significant amount.

While both the technology and market are still emerging, drilling in an area with known gas shows and right next door to existing ammonia and petrochemical facilities gives it a strategic edge.

The fact that the drilling program is fully funded by a tier-one backer is also a vote of confidence in the project’s underlying geology and commercial promise.

For those of us watching this emerging space, Hyterra’s wells should provide some valuable first data points on what might be possible – and a useful preview of what TEE will be targeting when their rigs start turning, all while carrying a fraction of Hyterra’s price tag.

Equities Club Weekly ASX Wrap: Market Insights and Outlook

The ASX might’ve clocked off early this week, but the market narratives never stop.

Gold keeps pushing higher. Lithium’s working through a reset. And natural hydrogen’s moving from idea to drillbit.

While we keep our ear to the ground, we encourage all our readers to continue with financial discipline and keep backing teams with a plan and near-term news. Stay patient, stay selective.

Tough markets don’t reward the lazy. But they do leave the door open for anyone paying attention. You only need one good hit to turn things around.

This website offers general information intended to guide you, and does not constitute personal advice. We recommend considering how this information aligns with your personal goals and financial circumstances. All information and advice is provided without any responsibility of liability on any account whatsoever on the part of this firm or any member or employee thereof.

Equities Club Ltd (CAR No. 001308139) is a corporate authorised representative of ShareX Pty Ltd, Australian Financial Services License (AFSL) No. 519872.

Disclosure: Equities Club owns 600,000 shares of TEE at the time of publishing this article. Equities Club has been engaged by TEE at the time of writing.